Trends & Determinants of Self- insuring Health Benefits 1997-2004 PRELIMINARY-PLEASE DO NOT

advertisement

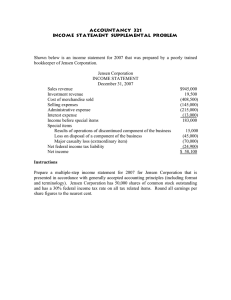

PRELIMINARY-PLEASE DO NOT QUOTE Trends & Determinants of Selfinsuring Health Benefits 1997-2004 Philip F. Cooper Kosali I. Simon Why do Firms Self-Insure (and Why Should We Care)? Firms self-insure to lower costs for economic and legal reasons – Over 50% of all insured employees in 1990s received self insured benefits (Jensen, Gabel, Hawkins 2001) States ability to regulate insurance limited when firms self insure – Mandates on benefits or workers, premium tax, coverage continuation, community rating etc. Prior ResearchPrevalence and trends in self insurance McDonnell et al (1986) – Over 50% of employees with ESI are in selfinsured plans in 1984, varies by firm size Acs, Long and Marquis (1996) – 42% of employees with ESI are in self-insured plans in 1987, 32% in 1991, 41% in 1993 33% of employees with ESI are in self insured plans in 1997, down from 40% in 1993 1993 and 1997 RWJF Park (2000) – % of employees in firms that self insure at least one plan in 1993, large variation by states NMES 1987, HIAA 1991, RWJF 1993 Marquis and Long (1999) – Prevalence Summary: % of Insured Employees in Self-insured Plans, by Year HCFA survey of employers, 1984 1993 NEHIS 60% % of insured employees in self-insured plans 50% 40% 30% 20% 10% 0% 1980 1985 1990 1995 2000 2005 Year Gabel, Jensen and Hawkins (2003) – % of workers in self insured plans 55% in 1993, 57% in 1996, 52% in 1999, 50% in 2001 HIAA/KPMG/HRET surveys of employers 93,96,99,01 •Caution: survey designs vary across studies so numbers not directly comparable •Many of these studies show prevalence and trends by firm size, industry, plan type (HMO vs PPO etc), premiums Influence of State Regulations on Self Insurance Cross sectional studies – – – Morrisey and Jensen (1993) Garfinkel (1995) Park (2000) Studies covering more than one year – Gabel and Jensen (1989) – Jensen and Morrisey (1990) finds that mandates are expensive; so is self insurance – – Jensen, Cotter and Morrisey (1995) Studies on effect of state mandates and other regulations on decision to insure Jensen and Gabel (1992) Gruber (1994) Kaestner and Simon (2002) – Buchmueller et al (2007) Overall picture-firm size matters, but state regulations do not appear important, at least not in more recent years. Our contributions Uses rich data new to this literature Multiple years of the same survey, recent years We examine – A) Recent trends in self insurance (descriptive) – B) Regression models to consider impact of state regulations, establishment, and local market characteristics on decision to self insure Data Medical Expenditure Panel Survey – Insurance Component (MEPS-IC) 1997-2004 – Large nationally representative annual employer survey ~ – – – – 25,000 establishments Health insurance plan info – type, self-insured/ purchased Establishment characteristics State level estimates Response rate ~ 78 percent ARF State mandates State Mandates State regulation mandated benefits Small group reform Premium taxes Stop loss regulation Number of Workers Enrolled in Selfinsured Plans 40,000,000 30,000,000 20,000,000 10,000,000 0 1997 1998 1999 Source MEPS-IC 1997-2004 2000 2001 2002 2003 2004 Percent of Active Enrollees in Selfinsured Plans 60 50 40 30 20 10 0 1997 1998 1999 2000 Source MEPS-IC 1997-2004 2001 2002 2003 2004 Percent of Establishments that offer a Self-insured Plan 40 30 20 10 0 1997 1998 1999 2000 Source MEPS-IC 1997-2004 2001 2002 2003 2004 Percent of Establishments that Offer a Self-Insured Plan by Firm Size 100 80 Less than 50 More than 50 500 or more 60 40 20 0 1997 1998 1999 2000 2001 2002 2003 2004 Source MEPS-IC 1997-2004 Percent of Establishments that Offer a Self-Insured Plan by Whether Multiple Location Firm 80 60 One More than one 40 20 0 1997 1998 1999 2000 2001 2002 2003 2004 Source MEPS-IC 1997-2004 Average Single Premium $4,000 $3,000 Purchased Self-Insured $2,000 $1,000 $0 1999 2000 2001 2002 Source MEPS-IC 1997-2004 2003 2004 Average Family Premium $12,000 $10,000 $8,000 $6,000 $4,000 $2,000 $0 Purchased Self-Insured 1999 2000 2001 Source MEPS-IC 1997-2004 2002 2003 2004 Percent of Establishments that Self-Insure and Offer a Purchased Plan 25 20 15 10 5 0 1997 1998 1999 2000 Source MEPS-IC 1997-2004 2001 2002 2003 2004 Logit Results Probability of Offering A Self-Insured Plan(significant) Increase likelihood Decrease likelihood – Firms size – Low wage – Multiple locations – Retail trade, services relative to manufacturing Conclusion No statistically significant effects from mandated – Suggests they don’t drive the decision to self-insure Multiple location and size matter Future work will add more state regulation (re- insurance limits)