What Does 2005 Hold? Mark S. Rzepczynski, Ph.D The 5

advertisement

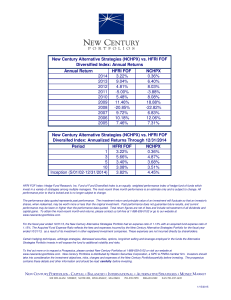

INC What Does 2005 Hold? The 5th Annual Alternative Investments for Institutional Investors Conference Mark S. Rzepczynski, Ph.D President and Chief Investment Officer You Cannot Look in the Rearview Mirror to Find the Answers INC • Performance reordering – the best strategies change • Style changes – focused strategies more risk sensitive • Dynamic industry changes – growth is an issue “Human History is a Race Between Education and Catastrophe” — H.G. Wells INC • What we know: ¾ Performance persistence does not exist ¾ Volatility persistence does exist ¾ Style alpha high and traditional benchmark tracking error high • What we don’t know: ¾ Whether recent past is a view of the future ¾ Attribution with dynamic strategies ¾ Style risks Are We “Gambling with Fair Dice”? INC • Faced with uncertainty as well as risk ¾ Risk ~ countable (measurable with a sample) ¾ Uncertainty ~ no sample of events • We do not like losses ¾ Desire satisfaction, but suffer from regret – negative skew problem • Yet, overconfident of what we know ¾ Law of small numbers Optimization Provides Insights INC An Optimizer Focuses on Some Familiar Strategies and Changes Others Significantly 100% 90% 80% 70% 60% 50% The Expected and Actual Sharpe Ratio Can be Very Different for a Hedge Fund Portfolio CISDM CTA Return (Equally Weighted) 3.25 HFRI Distressed Securities Index 2.75 HFRI Equity Hedge Index 2.25 HFRI Fixed Income (Total) 1.75 HFRI Relative Value Arbitrage Index 40% 30% HFRI Merger Arbitrage Index 20% HFRI Equity Market Neutral Index 10% HFRI Convertible Arbitrage Index 0% 1999 2000 2001 2002 Sources: CISDM, Hedge Fund Research, Inc. 2003 1.25 0.75 0.25 -0.25 1999 2000 2001 Optimized from past 3 years 2002 2003 Realized from current year Coherence is a Big Risk INC • What if hedge funds move together? ¾ We can measure overall correlation through coherence Coherence measures the amount of order with a set of assets or managers Between zero and one; (zero, no order; one, perfect order) ¾ Styles driven by limited common factors ¾ Fads, herding or contagion across managers and investors Coherence Between Traditional Assets and Hedge Funds Has Changed INC Correlative Coherence A Measure of the Order Across Assets Has Increased 0.55 0.5 0.4 0.35 0.3 0.25 Traditional assets and hedge funds Correlative coherence Traditional assets Correlative coherence -9 4 Ju n95 De c95 Ju n96 De c96 Ju n97 De c97 Ju n98 De c98 Ju n99 De c99 Ju n00 De c00 Ju n01 De c01 Ju n02 De c02 Ju n03 De c03 Ju n04 0.2 De c Coherence 0.45 Sources: CISDM, Hedge Fund Research, Inc. & Standard & Poor’s You May Want to be Incoherent! INC • “True” diversification vs. pseudo-diversification ¾ Diversification by the style not the numbers • Convergence versus Divergence ¾ View of the world makes a difference Convergent (mean-reverting view) Divergent (mean-fleeing view) • What should be the price of skew? Threshold Risk also Important INC • What is your target return? • Downside risk is what we are afraid of ¾ Originally discussed by Markowitz ¾ Selling volatility funds actually creates more potential for downside risk • Upside potential also a problem ¾ Higher Sharpe ratios may lead to a return shortfall Cases or Situations as Stress Analysis INC • Stress behavior has to be tied to events ¾ Case based reasoning can be applied What are the events you expect and fear? Are they protected with the hedge funds you have? • What can we expect for 2005 ¾ The unknown will happen ¾ What is hot today will not be tomorrow ¾ Analysis is important but the beginning point Notes INC Although offering potential benefits, an investment with JWH is speculative, involves a high degree of risk, and is designed only for sophisticated investors who are able to bear the loss of more than their entire investment. Some, but not all, of the risk factors that should be considered prior to making an investment decision include: forward contract trading, which is not afforded the regulatory protection of exchanges or the Commodity Exchange Act and may subject an investor to greater risks than trading on US exchanges; trading on non-US futures exchanges, which are not regulated by any US government agency and may involve certain risks not applicable to trading on US exchanges; currency risks associated with foreign-denominated margin deposits; possible failure of brokerage firms or futures exchanges; illiquid markets, which may make it more difficult to establish or liquidate a position at a given price. For more details on these and other risk factors, please refer to JWH’s current disclosure document. OTHER This presentation does not constitute an offer to sell or a solicitation for any managed account and cannot disclose all risks and significant elements of the JWH investment programs. Solicitations can only be made with a JWH disclosure document, which is available at the offices of JWH upon request. Further details of past performance and definitions of terms used to state past performance are presented in the disclosure document. An investment with JWH is speculative, involves a high degree of risk, and is designed only for sophisticated investors who are able to bear the loss of more than their entire investment. Read and examine the disclosure document before seeking JWH's services. PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS. INC