Consumer Staples Scott Yanjun Yiqin

advertisement

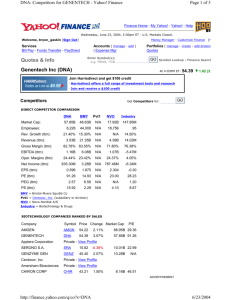

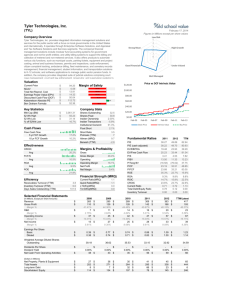

Consumer Staples Scott Yanjun Yiqin Lorillard Best Known For Newport Brand of Cigarettes. Newport represents 85.7% of corporate sales. Newport is the leading menthol cigarette. Lorillard Financial Performance Company Data Price ($) Date of Price 52-wk Range Market Cap Shares O/S (mil) Beta Dividend Yield P/E (ttm) EPS (ttm) $53.35 March 28, 2014 $40.01 - $56.85 $19.3B 362.2 0.4 4.61% 16.85 3.166 Stock Price Investment Thesis • • • • Currently Trading Near its High P/E Ratio Smoking Rates Consistently Declining World Tobacco Prices Increasing High Taxation Per Pack of Cigarettes Sold. Profit Drivers Lorillard Per Share Data 2013 2012 2011 2010 2009 2008 Tangible Bk. Val. -6.17 NM -3.82 NM 0.19 1.25 Cash Flow 3.29 2.92 2.76 2.34 1.98 1.78 Earnings 3.18 2.81 2.66 2.26 1.92 1.72 Dividends 2.20 2.07 1.74 1.42 1.28 0.92 Payout Ratio 69% NM 65% 63% 67% 53% Prices - High 53.27 47.02 40.00 29.90 27.25 29.74 - Low 37.84 35.61 24.13 23.41 17.50 17.77 P/E Ratio - High 17.00 17.00 15.00 13.20 14.00 17.00 - Low 12.00 13.00 9.10 10.40 9.00 10.00 Competition Direct Competitor Comparison Market Cap: Employees: Qtrly Rev Growth (yoy): Revenue (ttm): Gross Margin (ttm): EBITDA (ttm): Operating Margin (ttm): Net Income (ttm): EPS (ttm): P/E (ttm): PEG (5 yr expected): P/S (ttm): MO 73.80B 9,000 -0.01 17.66B 0.59 8.57B 0.47 4.52B 2.26 16.42 1.96 4.19 LO 19.32B 2,900 0.04 6.97B 0.55 2.25B 0.44 1.18B 3.15 16.94 1.41 3.87 RAI 28.47B 5,200 -0.02 8.24B 0.55 3.41B 0.40 1.72B 3.14 16.89 2.11 3.46 Industry 28.47B 5.20K 0.06 8.24B 0.55 3.41B 0.37 N/A 3.14 16.89 2.11 4.09 Implied Valuation Recommendation • SIM Does Not Currently own the Stock. • No reason to Buy at this time. Conclusion: Hold/Not Purchase Target:56 CVS Caremark Corp A. Company Overview A. Retail Pharmacy B. Pharmacy Business C. Corporate Segment B. Recent News A. Tobacco Exit B. Earnings Report C. Valuation A. Key Drivers A. Health Care Reform B. Pricing Competition C. Consumer Spending A. DCF B. Multiple Valuation Health Care Reform Pricing Competition Pharmacies and drug stores face increasing competition in 2014 from mass merchandisers Private health insurance coverage usually can lower the price of pharmaceutical products and exerts downward pricing pressure through managed care organizations. Consumer Spending In 2014, per capita disposable income is expected to increase at a slower pace, representing a potential hurdle for the industry Recent News-Contract Renewal The most important event for the company recently is the its three-year contract to provide integrated pharmacy services to over five million federal employees, retirees, and dependents. The announcement pushed the stock price to $75, the highest price throughout its history mainly It helped reduce the concern of aggressive pricing behavior in retail segment and provided further evidence of the strength of CVS' integrated PBM/retail model. Recent News-Earnings Report EPS for 4Q13 is $1.12, representing $0.01 above consensus. The FY2013 net revenue increased by 3% compared to 2012, and the gross margin has increased by 50bps. On the PBM side, the company has strong health plan relationships as management cited a footprint spanning 25 states covering 70% of the eligible exchange population and a leading presence in Medicaid managed care. Valuation-Growth Forecast Valuation-DCF Valuation-Sensitivity Valuation-Multiples Conclusion: SELL; Target:69.55(-); -75~80 bps A. Company Overview A. B. C. D. E. F. Eurasia & Africa Europe Latin America North America Pacific Bottling Investment B. Financial Highlights A. Segment growth B. Operating margin C. Recent News A. B. C. D. Brazil & China investment Domestic health issue Electric fleet Overcompensated CEO? Valuation KO DPS NSRGY Market Cap: 169.23B 10.61B 240.05B 126.18B 278.81B Employees: 130,600 19,000 333,000 274,000 274.00K -0.04 46.85B 0.61 13.10B 0.24 -0.01 6.00B 0.58 1.32B 0.18 0 98.97B 0.48 18.55B 0.16 0.01 66.42B 0.53 12.34B 0.15 0.14 66.42B 0.53 12.34B 0.13 Net Income (ttm): 8.58B 624.00M 10.73B 6.73B N/A EPS (ttm): P/E (ttm): PEG (5 yr expected): P/S (ttm): 1.9 20.22 2.88 3.64 3.05 17.63 2.28 1.79 3.35 22.44 5.22 2.42 4.32 19.18 2.43 1.91 4.32 24.11 2.63 1.91 25.90% 27.39% 16.47% 29.01% 24.00% Qtrly Rev Growth (yoy): Revenue (ttm): Gross Margin (ttm): EBITDA (ttm): Operating Margin (ttm): Return on Equity (ttm): PEP Industry Investment Thesis • Strong fundamentals • World Cup Speculation • Dividend Parachute Growth Contribution Volume1 Price, Structural Product & Currency Changes Geographic Fluctuations Mix Total Consolidated 2% (3%) 1% (2%) (2%) Eurasia & Africa 7% —% 2% (7%) 2% Europe (1) — 5 — 4% Latin America 1 (1) 10 (8) 4% North America — (1) 1 — — Pacific 5 (2) (4) (6) (5%) Bottling Investments 4 (18) 1 (1) (14%) Revenue vs. Income % of total Operating margin 100% 21.80% 2,763 6 39.3 1,087 11 4,645 10 61.5 2,859 28 4,748 10 61.3 2,908 28 21,574 46 11.3 2,432 24 5,372 11 46.1 2,478 24 7,598 16 1.5 115 1 Revenue Consolidated Eurasia & Africa Europe Latin America North America Pacific Bottling $ 46,854 Income $ 10,228 % of total 100% Incremental • Cost saving initiatives: • 300 – 450 million annually as planned; 150 -200 as estimated Worst Cost Saving Best guess Best 100 200 350 • FY2014 revenue: Worst Best guess Best Consolidated -0.9% 2.1% 3.7% Eurasia & Africa -0.1% 4.7% 2.3% Europe -1.1% 0.9% 1.9% Latin America 2.1% 4.6% 6.1% North America -2.8% -0.8% 0.7% Pacific -2.1% 0.9% 3.9% Bottling Investments -2.2% 0.7% 2.7% Analyst: Yanjun Gu 2014/3/29 Year Revenue % Grow th Operating Income Operating Margin Interest Interest % of Sales Taxes Tax Rate Net Income Terminal Discount Rate = Terminal FCF Growth = 2014E 47,838 2.1% 10,811 22.6% 96 0.20% 2,972 24.8% 7,935 % Grow th 2015E 49,058 2.6% 10,842 22.1% 98 0.20% 3,033 24.6% 7,907 2016E 50,530 3.0% 11,521 2017E 52,045 3.0% 11,970 2018E 53,607 3.0% 12,330 8.5% 3.0% 2019E 55,215 3.0% 12,699 2020E 56,871 3.0% 13,080 2021E 58,578 3.0% 13,473 2022E 60,335 3.0% 13,877 2023E 62,145 3.0% 14,293 2024E 64,009 3.0% 14,722 22.8% 23.0% 23.0% 23.0% 23.0% 23.0% 23.0% 23.0% 23.0% 101 104 107 110 114 117 121 124 128 0.20% 0.2% 0.2% 0.2% 0.2% 0.2% 0.2% 0.2% 0.2% 3,020 24.6% 8,602 2,964 24.6% 9,110 3,053 24.6% 9,384 3,145 24.6% 9,665 3,239 24.6% 9,955 3,336 24.6% 10,254 3,436 24.6% 10,561 3,540 24.6% 10,878 3,646 24.6% 11,204 -0.4% 8.8% 5.9% 3.0% 3.0% 3.0% 3.0% 3.0% 3.0% 3.0% 2,033 2,109 2,163 2,228 2,294 2,363 2,434 2,507 2,582 2,660 2,740 4.3% 4.3% 4.3% 4.3% 4.3% 4.3% 4.3% 4.3% 4.3% 4.3% 4.3% 241 241 263 208 214 221 227 234 241 249 256 0.5% 0.5% 0.5% 0.4% 0.4% 0.4% 0.4% 0.4% 0.4% 0.4% 0.4% Subtract Cap Ex 1,914 1,914 1,766 1,301 643 497 398 293 241 249 256 Capex % of sales 4.0% 3.9% 3.5% 2.5% 1.2% 0.9% 0.7% 0.5% 0.4% 0.4% 0.4% 8,344 9,262 10,245 11,249 11,752 12,218 12,702 13,144 13,538 13,944 0.6% 11.0% 10.6% 9.8% 4.5% 4.0% 4.0% 3.5% 3.0% 3.0% Add Depreciation/Amort % of Sales Plus/(minus) Changes WC % of Sales Free Cash Flow 8,296 % Grow th NPV of Cash Flows NPV of terminal value Projected Equity Value Free Cash Flow Yield 73,684 115,496 189,179 4.84% 39% 61% 100% Current Price $ 38.66 Implied equity value/share $ 42.67 Upside/(Downside) to DCF 10.4% Best Guess Stage I Worst Best Guess Ideal Price 40.74 42.67 43.71 Stage II Worst Best Guess Ideal Price 41.00 43.17 44.59 +% 6.5% 12.1% 15.8% Stage I: adjust revenue growth Stage II: Factor in cost saving Sensitivity $ 43.17 7.0% 7.5% 8.0% 8.5% 9.0% 9.5% 10.0% 1.50% 43.81 40.07 36.91 34.20 31.85 29.80 27.99 2.00% 48.06 43.60 39.88 36.73 34.04 31.70 29.66 2.50% 53.26 47.82 43.38 39.68 36.55 33.87 31.55 3.00% 59.75 52.99 47.59 43.17 39.49 36.38 33.71 3.50% 68.10 59.45 52.73 47.36 42.96 39.30 36.20 4.00% 79.23 67.76 59.16 52.48 47.13 42.76 39.11 4.50% 94.82 78.84 67.43 58.87 52.22 46.90 42.55 World Cup 14.3% 18.2% ? Dividend Policy • Paid increasing dividends for 52 consecutive years • Coca-Cola has a Dividend yield of 3.16% with increasing dividends for 25+ years Conclusion: BUY; Target 43.17( +12.1%); + 150 bps Recommendation Not doing anything about Lorillard and Phillip Morris. Sell CVS 75 to 80 bps, and use the proceeds to buy KO for 150 bps. Ticker LO PM KO PEP CVS CPB Current Target Price Price 53 83 38 84 74 44 56 85 43 78 70 33 Return /Loss 6% 2% 12% -7% -5% -25% Current Recommendation New Weight Weight 0% 0% 0% 0% 5.1% 0% HOLD HOLD BUY HOLD Sell Hold 0% 0% 1.4% 0% 4.3% 0%