Document 11015328

advertisement

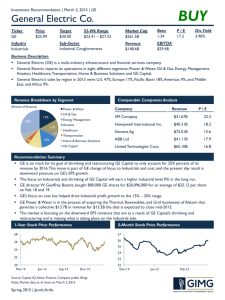

SUMMER 2015 SIM SECTOR PRESENTATION MATERIALS SECTOR JULY 15, 2015 ALIX PITTS & JD PISULA AGENDA SECTOR OVERVIEW BUSINESS ANALYSIS ECONOMIC ANALYSIS FINANCIAL ANALYSIS VALUATION ANALYSIS RECOMMENDATION SECTOR OVERVIEW The Industry Classifica3on Benchmark (ICB) is an industry classifica3on taxonomy launched by Dow Jones and FTSE in 2005 and now owned solely by FTSE Interna3onal. It is used to segregate markets into sectors within the macroeconomy. The ICB uses a system of 10 industries, par33oned into 19 supersectors, which are further divided into 41 sectors, which then contain 114 subsectors. The Basic Materials Sector consists of the following company types: SECTOR OVERVIEW LARGEST COMPANIES IN MATERIALS SECTOR SECTOR OVERVIEW S&P WEIGHTS Materials 3.13% U3li3es 3% Energy 8% Telecommuni-­‐ ca3on Services 2% Materials U3li3es 2.25% 3% Informa3on Technology 20% Consumer Staples 9% Energy 7% Telecommunica3-­‐ on Services 3% Informa3on Technology 21% Consumer Staples 8% Financials 17% Industrials 10% Consumer Discre3onary 13% SIM WEIGHTS Health Care 15% Financials 18% Industrials 9% Consumer Discre3onary 13% Health Care 16% SECTOR OVERVIEW Following a 10 year run of performance above S&P 500– fueled by BRIC development par3cularly China, the Basic Materials Sector has lagged of late. Contrasted with Healthcare which is accelera3ng on demographics (aging, growing, longer lives), the Basic Materials sector is beset by forecasted so\ demand and pricing pressure on oversupply and slowing China growth, which has fueled 100% of global growth in this sector over the preceding 5 year period. Sources: Morningstar Research & Charles Schwab SECTOR OVERVIEW YEAR-­‐TO-­‐DATE PERFORMANCE SECTOR OVERVIEW THREE-­‐YEAR PERFORMANCE SECTOR OVERVIEW INDUSTRY PERFORMANCE BUSINESS ANALYSIS PORTER’S FIVE FORCES MODEL • Materials is in the mature phase • Growth reflects the overall rate of the economy • Stable earnings BUSINESS ANALYSIS Sizable sector (roughly 4% of US market cap), with greater than market PE ra\o, and forecasted decelera\on in sales and earnings growth = precarious valua\on zone. BUSINESS ANALYSIS -­‐ Consistent with a mid-­‐cycle phase, Materials are currently underperforming -­‐ When will we enter a Late Cycle Phase? ECONOMIC ANALYSIS Slowing growth reflected in con0nued sector underperformance Requires investors to choose wisely within subsectors Sources: Ned Davis Research Charles Schwab Research ECONOMIC ANALYSIS TRENDS TO WATCH -­‐ Commodity prices -­‐ Currency headwinds -­‐ Low growth in Europe -­‐ Slowdown in China -­‐ Momentum in US Automo\ve -­‐ US Housing and Commercial Construc\on -­‐ Shale gas investments -­‐ Specula\on risk FINANCIAL ANALYSIS -­‐ P/E has fallen over the last few years and is es3mated to fall further -­‐ P/S, P/B and EV/Sales have grown recently, but are expected to shrink over the next few years FINANCIAL ANALYSIS -­‐ Sales per share have been mostly flat and this trend is expected to con3nue -­‐ While margins have 3ghtened recently, es3mates show that improved margins are expected in the near future VALUATION ANALYSIS -­‐ Based upon historical values, the Materials sector is rich on a P/E and P/B basis -­‐ Materials trade a slight premium to the SPX, but most analysts expect this trend to end and a discount to develop RECOMMENDATION -­‐ Con3nue to UNDERWEIGHT -­‐ Global growth prospects create uncertainty for this sector -­‐ Remember sector sub-­‐segments are not all alike -­‐ Avoid Mining and Metals -­‐ Avoid value traps -­‐ Search for diversified companies that are mildly less cyclical and specula3ve