Chapter 6

advertisement

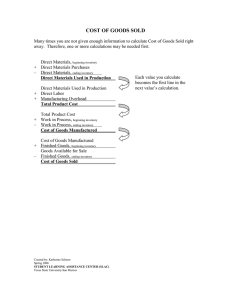

Chapter 6 Periodic and Perpetual Inventory Systems There are two methods of handling inventories: • • the periodic inventory system, and the perpetual inventory system With the periodic inventory system, the firm calculates its Cost of Goods Sold at the end of the year. The firm takes its beginning inventory, and adds its purchases for the period. This gives the firm all the goods that pass through the firm for the period (the goods available for sale). The firm then takes a physical inventory. This gives the firm what is left at the end of the period. The ending inventory is then subtracted from the available goods figure to get the cost of goods sold. Two disadvantages of the periodic method are: • • This method does not give the firm much information on the theft or spoilage of goods. (Everything not present is assumed to be sold.) Unless a physical inventory is taken, the firm does not know what its cost of goods sold is during the period (as opposed to the end of the period). An advantage of the periodic method is that it is a easy system to maintain. With the perpetual inventory system, the firm keeps track of its cost of goods sold on a continual basis. Thus, at any given time, the firm can estimate its current inventory levels. At the end of the period, a physical inventory is taken. Any discrepancy with the estimated inventory level and the actual inventory level is then attributed to theft and spoilage. An advantage of the perpetual system is that it provides information about theft and you have a Cost of Goods Sold figure whenever needed. A disadvantage of the perpetual system used to be that it was very expensive to maintain this type of system. With the use of computers and scanners, the marginal cost to implement a perpetual system may be minimal. What we have discussed to date is the perpetual inventory system. Differences Between Periodic and Perpetual Inventory Systems Periodic a. Purchase inventory on credit: D. Purchases Cr. Accounts Payable Perpetual D. Merchandise Inventory Cr. Accounts Payable b. Transportation Costs on purchases: D. Freight In Cr. Accounts Payable D. Freight In Cr. Accounts Payable c. Purchases Returns and Allowances: D. Accounts Payable Cr. Purchases Ret & Allow. D. Accounts Payable Cr. Merchandise Inventory D. Accounts Payable Cr. Cash D. Accounts Receivable Cr. Sales Cost of Goods Sold Cr. Merchandise Inventory d. Payments on Accounts Payable: D. Accounts Payable Cr. Cash e. Sale of Merchandise on Credit: D. Accounts Receivable Cr. Sales D. f. Payment of Delivery Costs D. Freight Out Expense Cr. Cash D. Freight Out Expense Cr. Cash D. Sales Returns and Allowances Cr. Accounts Receivable Merchandise Inventory Cr. Cost of Goods Sold g. Return of Merchandise Sold: D. Sales Returns and Allowances Cr. Accounts Receivable D. f. Receipts on Accounts Receivable: D. Cash Cr. Accounts Receivable D. Cash Cr. Accounts Receivable With the perpetual inventory system, you have the Cost of Goods Sold at any given time. You just look at the balance of the Cost of Goods Sold account. With the periodic inventory system, there is no Cost of Goods Sold account. Instead, you must calculate the Cost of Goods Sold by netting all of the inventory accounts. They are all closed to Income Summary, and the net amount which results places the Cost of Goods Sold as a debit in the Income Summary account -- as would have been the case under the perpetual inventory system if you had just closed out the Cost of Goods Sold account. Cost of Goods Sold: + + - Beginning Balance of Inventory (debit balance) Purchases (debit balance) Purchase Returns & Allowances (credit balance) Purchase Discounts (credit balance) Freight In (debit balance) -------------------------------------------Cost of Goods Available Ending Balance of Inventory -------------------------------------------Cost of Goods Sold Income Summary Account: INCOME SUMMARY (PARTIAL ENTRIES) Beginning Balance of Inventory Purchase Returns & Allowances Purchases Purchase Discounts Freight In Ending Balance of Inventory Cost of Goods Sold You close out the Inventory account. There were no additions to inventory during the year. Thus, Inventory is the beginning inventory: D. Income Summary Cr. Inventory $50,000 $50,000 You then close out all of the temporary/nominal accounts: D. Income Summary Cr. Purchases $300,000 D. Income Summary Cr. Freight-In $10,000 D. Purchase Returns & Allowances Cr. Income Summary $20,000 D. Purchase Discounts Cr. Income Summary $30,000 $300,000 $10,000 $20,000 $30,000 You finally add the current inventory figure (from physical inventory at end of year) to Income Summary and the Inventory account. You previously closed the Inventory account. This now adds the ending inventory figure to the Inventory account. After this, Inventory reflects the end of the year figure. D. Inventory Cr. Income Summary $40,000 $40,000 You now have the correct Cost of Goods figure as a debit balance in the Income Summary. If you had used the perpetual system and maintained a Cost of Goods Sold account, it would have had a debit balance (it is an expense). The Cost of Goods Sold account would have been closed, and it would have resulted in a debit entry to the Income Summary account. INCOME SUMMARY (PARTIAL ENTRIES) Beginning Balance of Inventory $50,000 Purchase Returns & $20,000 Allow. Purchases 300,000 Purchase Discounts 30,000 Ending Balance of Inventory 40,000 Freight In Cost of Goods Sold 10,000 $270,000 You get the same result if you use the formula: + + - Beginning Balance of Inventory (debit balance) Purchases (debit balance) Purchase Returns & Allowances (credit balance) Purchase Discounts (credit balance) Freight In (debit balance) -------------------------------------------Cost of Goods Available Ending Balance of Inventory -------------------------------------------Cost of Goods Sold $50,000 300,000 -20,000 -30,000 10,000 ---------$310,000 -40,000 -----------$270,000 Inventory Categories Inventory is often referred to as merchandise inventory by a retailer. Manufacturers have three types of inventory: raw materials, work in process, and finished goods. When they purchase raw materials, it goes into raw materials. When the company starts to make the product, the materials leave raw materials and get added to work in process. In work in process, the cost of the materials are combined with the cost of the labor (direct labor) and the factory overhead. Components of Inventory Cost Inventory cost is defined as the price paid to acquire the inventory and generally includes invoice price less purchases discounts, freight, insurance in transit, taxes, tariffs, inspection costs and preparation costs. It is basically everything that is paid in order to get the inventory ready to sell. Ownership of Goods The term "FOB shipping point" means that the seller transfers title to the goods at the seller’s place of business. The buyer pays shipping costs. For example, if you order a car from Ford and the invoice says FOB Detroit, then you pay the shipping costs and the car belongs to you as soon as it leaves the factory. The term "FOB destination" means that the seller transfers title to the goods at the buyer’s place of business. The seller pays shipping costs. For example, if you order a car from Ford and the invoice says FOB Los Angeles, then Ford pays the shipping costs and the car belongs to you when it arrives. Merchandise in transit is included in the buyer' s inventory if title to the goods has passed (e.g., FOB shipping point). Goods in transit shipped FOB destination belong to the seller. Sometimes companies enter into a consignment agreement where goods are transferred physically to another company without title transferring. Consigned goods belong to the consignor. They are not included in the consignee’s (the company doing the sale … not the actual owner) inventory. Inventory Costing Methods Under the Periodic Method A company must choose an inventory costing method. When identical items of merchandise are purchased at different prices during the year, it usually is impractical to monitor the actual goods flow and record the corresponding costs. Instead, the accountant will make an assumption about the cost flow and will use one of the following methods: • • • • specific identification average-cost first-in, first-out (FIFO) last-in, first-out (LIFO) The alternative methods have different effects on net income, income taxes, and cash flows. The implementation of these methods is effected by whether the company uses the perpetual system or the periodic system. We will first discuss the periodic system. In the following discussion, we will assume that the following purchases of inventory were made during June: Units Purchased: Units Sold: June June 1 6 13 20 25 10 30 Units in Ending Inventory: 50 50 150 100 150 -----500 units @ units @ units @ units @ units @ 70 210 -----280 units units 220 units $1.00 $1.10 $1.20 $1.30 $1.40 units units Specific Identification Under the specific identification method, you identify which goods were purchased on which dates (e.g., using serial numbers or labels). You then keep track of which goods were sold and which goods are still on hand at the end of the period. This method reflects the actual flow of goods. Assume that you identify that you sold the following units: 50 50 100 80 units from June 6 units from June 13 units from June 20 units from June 25 60 x 50 x 100 x 80 x $1.10 $1.20 $1.30 $1.40 = = = = $55 $60 $130 $112 -----$357 Cost of Goods Sold : You identify that you still have these goods in inventory at the end of the year: 50 100 70 units from June 1 units from June 13 units from June 25 50 x 100 x 70 x $1.00 = $1.20 = $1.40 = $50 $120 $98 -----$268 Cost of Remaining Inventory : This method is not common because it is expensive to keep track of which items are sold. This is especially true when you sell high volumes of goods. This method permits companies to manipulate income by choosing to sell the high- or low-cost items. The specific identification method is used primarily for high-priced items such as computer processors, automobiles, expensive furniture & jewelry. Average Cost Under the average cost method, a weighted average cost per unit is first computed for the goods available for sale during the period. This is accomplished by dividing the cost of goods available for sale by the units available for sale. June 1 6 13 20 25 Units Purchased: 50 50 150 100 150 -----500 Average Cost Per Unit units @ units @ units @ units @ units @ $1.00 $1.10 $1.20 $1.30 $1.40 = = = = = $50 $55 $180 $130 $210 -------$625 $625/500 = $1.25 units Then the average cost per unit is multiplied by the number of units in ending inventory to obtain the cost of ending inventory. Ending Inventory Cost of Goods Sold = 220 = 280 units @ units @ $1.25 $1.25 = = $275 $350 This method has the advantage of leveling the effects of variations in cost. Cost increases and decreases are leveled out. A disadvantage of this method is that the most current costs are not used in income determination. First-In, First-Out Under the first-in, first-out (FIFO) method the cost of the first items purchased is assigned to the first items sold. The 280 units sold are assumed to come from the first units: 50 50 150 30 units from June 1 units from June 6 units from June 13 units from June 20 60 x 50 x 100 x 80 x $1.00 $1.10 $1.20 $1.30 = = = = Cost of Goods Sold : $50 $55 $180 $39 -----$324 Therefore, ending inventory consists of the most recent purchases. 70 150 units from June 20 units from June 25 70 x 150 x $1.30 = $1.40 = Cost of Remaining Inventory : $91 $210 -----$301 During periods of rising prices, FIFO yields the highest net income of the four methods. Last-In, First-Out Under the last-in, first-out (LIFO) method, the last items purchased are assumed to be the first items sold. The 280 units sold are assumed to be: 150 100 30 units from June 25 units from June 20 units from June 13 Cost of Goods Sold : 150 x 100 x 30 x $1.40 = $1.30 = $1.20 = $210 $130 $36 -----$376 Therefore, ending inventory is assumed to consist of items from the earliest purchases. 50 50 120 units from June 1 units from June 6 units from June 13 50 x 50 x 120 x $1.00 = $1.10 = $1.20 = Cost of Remaining Inventory : $50 $55 $144 -----$249 When a company uses LIFO, it must report, in the notes to its financial statements, what its inventory would have been using FIFO. The difference between the two numbers is called the LIFO Reserve: Inventory Using LIFO LIFO Reserve Inventory Assuming FIFO $249 52 ------$301 Reporting LIFO reserve enables financial analysts to make allowances for the use of LIFO when comparing companies. The LIFO reserve, if positive, indicates how much higher retained earnings would have been had the company used FIFO. In the prior example, the difference in net income would have been equal to the difference in Cost of Goods Sold (an expense): COGS Under FIFO LIFO Reserve COGS Under LIFO $324 52 ------$376 An advantage of LIFO is that, during periods of rising prices, LIFO best matches current merchandise costs with current sales prices. This results in the lowest net income of the four methods. This is a major advantage when considering tax costs. Lower income results in lower income taxes. You have to use the same method for financial & tax purposes. The lower net income is also a major disadvantage of LIFO when financial reporting is considered. LIFO makes the company look less profitable (lower income), however most users of financial statements will take this into account when evaluating the company. Another disadvantage is that the inventory valuation under LIFO is often unrealistic. Also, LIFO is not accepted in most other countries. A LIFO liquidation occurs when sales have reduced inventories below the levels established in prior years. When prices have been rising steadily, a LIFO liquidation produces unusually high profits. This retrains the company from reducing inventory levels when it may be in the company’s best interests to do so. Comparison of the Methods During periods of rising prices, FIFO produces a higher net income than LIFO, and the average-cost method produces net income that is somewhere between those of FIFO and LIFO. During periods of falling prices, the reverse is true. Even though LIFO best follows the matching rule, FIFO provides a more up-todate ending inventory figure for balance sheet purposes. Inventory Methods Under the Perpetual System The pricing of inventories under the perpetual system differs from pricing under the periodic system. Under the perpetual system, the cost of goods sold is determined at the time of sale, and the cost of ending inventory is determined after every inventory transaction. The specific identification method produces the same results under the perpetual system as under the periodic system. The FIFO method also produces the same results regardless of the system used. The first units are always the first units no matter when you do the calculation. Average Cost Under the Perpetual System Using the average-cost method in a perpetual system, a moving average is computed after each purchase. June 1 6 Units Purchased: 50 50 -----100 Average Cost Per Unit units @ units @ $1.00 = $1.10 = $50 $55 -------$105 $105/100 = $1.05 units This cost is used for the 70 units sold on June 10 ($73.50). The remaining units will be considered to cost $1.05 until the next calculation. Calculation -June Sale 10 10 Balance 10 13 20 25 Units Purchased: 100 -70 -----30 150 100 150 -----430 Average Cost Per Unit units @ units @ $1.05 = $1.05 = units @ units @ units @ units @ $1.05 $1.20 $1.30 $1.40 units $551.50/430 = $105.00 -$73.50 ---------$31.50 $180.00 $130.00 $210.00 -------$551.50 $1.28 This cost is used when 210 units are sold on June 30 ($268.80). The remaining 220 units in inventory are valued using the $1.28 cost ($282.70). The Cost of Goods Sold is $342.30 ($73.50 + 268.80). LIFO Under the Perpetual System LIFO produces different figures under the perpetual system because you use the last units purchased before the individual sale: June 10 Sale 50 units from June 6 20 units from June 1 50 x 20 x $1.10 = $1.00 = Cost of Goods Sold : $55 $20 -----$75 Remaining inventory is assumed to consist of items from the earliest purchases. June 10 Remaining Units 30 units from June 1 30 x $1.00 = Cost of Remaining Inventory : $30 -----$30 The most recent goods acquired prior to the June 30 sale is used on that date: 150 60 units from June 25 units from June 20 Cost of Goods Sold : 150 x 100 x $1.40 = $1.30 = $210 $78 -----$288 The Cost of Goods Sold for the month is $363 ($75 + $288). The ending inventory is assumed to consist of items from the earliest purchases that have not been sold previously: 30 150 40 units from June 1 units from June 13 units from June 29 30 x 150 x 40 x $1.00 = $1.20 = $1.30 = Cost of Remaining Inventory : $30 $180 $52 -----$262 Lower of Cost or Market Inventory is carried at the lower of cost or market. This is an example of conservatism. We do not want unsold obsolete inventory carried at high historical costs. The market value of inventory is defined as current replacement cost or net realizable value (sales price less selling expenses). Market value of inventory may fall below its cost because of physical deterioration, obsolescence, or a decline in price level. There are three basic methods for implementing the lower of cost or market comparison. You may do it on a: • • • specific item level major category level, or total inventory level To determine the lower of cost or market: • • • First, cost is determined by using the FIFO, LIFO, Specific Identification or Weighted Average methods; Second, calculate the market value (Replacement cost or Net Realizable Value; and Third, compare cost to market. The tax rules do not permit all of the methods described above. For example, the total inventory comparison is not acceptable for federal income tax purposes. Also, for tax purposes, you may not use lower of cost or market method when using the LIFO method. Inventory Errors Cost of goods available is assigned to goods sold and ending inventory. Recalling that cost of goods available less ending inventory equals cost of goods sold, it can be seen that the higher the cost of ending inventory, the lower the cost of goods sold and the higher the gross profit and net income. The converse also is true. Because the cost of ending inventory is needed to compute the cost of goods sold, it affects net income dollar for dollar. It is most important to match cost of goods sold with sales so that a proper determination of net income will result. This year' s ending inventory automatically becomes next year' s beginning inventory. Because beginning inventory also affects net income dollar for dollar, an error in this year' s ending inventory results in misstated net income for both this year and next year. When ending inventory is understated, the Cost of Goods Sold will be too high. Because you are subtracting a high number as an expense (COGS), the net income for the period will be understated. This year’s ending inventory becomes next year’s beginning inventory. Thus, next year’s beginning inventory will be too low. This will result in a lower Cost of Goods Sold for the second period. Because you are subtracting a COGS figure that is too low, the net income in the second year will be overstated. The differences in net income for the two years will offset each other. This Year COGS Beg. Bal. + Purch. Available -End. Inv. COGS Net Income $ XXX +XXX --------$XXX -Too Low -----------Too High ======= Next Year COGS Beg. Bal. + Purch. Available -End. Inv. Too Low $ Too Low + XXX -------------$ Too Low XXX -------------- COGS $ Too Low ======== Net Income Too High When ending inventory is overstated, the Cost of Goods Sold will be too low. Because you are subtracting a low number for COGS, the net income for the period will be overstated. This year’s ending inventory becomes next year’s beginning inventory. Thus, next year’s beginning inventory will be too high. This will result in a higher COGS for the second period. Because you are subtracting a COGS figure that is too high, the net income for the second period will be understated. This Year COGS Beg. Bal. + Purch. Available -End. Inv. COGS Net Income $ XXX +XXX --------$XXX -Too High -----------Too Low ======= Next Year COGS Beg. Bal. + Purch. Available -End. Inv. Too High $ Too High + XXX -------------$ Too High -XXX -------------- COGS $ Too High ======== Net Income Too Low Financial Statement Analysis Financial Analysts pay particular attention to a company’s inventory. Although a company wants to have enough inventory to meet the demands of its customers, it doesn’t want to have too much inventory because it ties up resources, and the inventory can become obsolete. The desire to minimize inventory levels has led to the implementation of a JustIn-Time operating environment by many companies. Under the Just-In-Time system, a company tries to have its inventory arrive just at the time they are needed. In determining inventory levels, management must balance the cost of handling, storing, and financing inventories with the cost of lost sales and dissatisfied customers. For example, Dell is considered to have a competitive advantage over its competitors because it keeps relatively low levels of inventory and still meets the demands of its customers very quickly. Two ratios used in this area are: • • Inventory Turnover Ratio Days in Inventory Inventory Turnover Ratio The Inventory Turnover Ratio is used to measure inventory levels and is computed by dividing cost of goods sold by the average inventory. It indicates the number of times, on average, inventory is sold during the period. Cost of Goods Sold ---------------------------Average Inventory Days In Inventory This is also called “Average Days’ Inventory On Hand”. This ratio indicates the average number of days between the purchase and sale of inventory. It is traditionally computed by dividing the number of days in a year by the inventory turnover. 365 ------------------------------------------Inventory Turnover Ratio It is easier for me to remember this formula if I think of it as follows. First, calculate how much inventory you sell in a day: Cost of Goods Sold -------------------------365 Now that you have the inventory sold in one day, divide that figure into your average inventory level for the year: Average Inventory ------------------------------------------Inventory Sold in One Day Mathematically, this is the same formula. Estimating Inventory If you use the periodic inventory system, then you probably take a physical inventory once a year because it is very expensive. When preparing interim financial statements, companies usually do not want to go to the expense of conducting a physical inventory. Instead, the company estimates its inventories based upon its sales figures using two methods: • • retail method, and gross margin method. As you can see below, they are really doing the same thing, but they approach it from different angles. Both are based on knowing the relationship between product cost and retail values. Retail Method of Inventory Valuation The retail method of inventory estimation can be used when there is an overall constant relationship between the cost and the sales price for goods over a period of time. To apply the retail method: a. Goods available for sale is first determined both at cost and at retail. Beginning Inventory Net Purchases (includes Freight-In) Goods Available For Sale Cost $ 40,000 110,000 -----------$150,000 Retail $ 55,000 145,000 -----------$200,000 b. Then, calculate the cost-to-retail ratio. In this case, it is 75% ($150,000/$200,000). c. Sales for the period are subtracted from goods available for sale (using retail values) to produce ending inventory at retail. Retail Value of Goods Available for Sale Less: Sales for Period Retail Value of Remaining Inventory $200,000 -160,000 ------------$40,000 d. Finally, ending inventory at retail is multiplied by the cost-to-retail ratio to produce an estimate of ending inventory at cost. The estimated cost of remaining inventory in this case is $30,000 ($40,000 x 75%). Gross Margin Method of Inventory Valuation The gross margin method (gross profit method) of inventory estimation assumes that the percentage of gross profit for a business remains relatively stable from year to year. The gross profit method involves three steps. First, estimate the cost of goods sold by multiplying sales by (one minus the gross profit percentage). In this case, the gross profit percentage is 25%, and one minus the gross profit percentage is 75% (1-25%). Sales x 1 - Gross Profit Percentage Estimated Cost of Goods Sold $160,000 X 75% -------------$120,000 Next, use the estimated Cost of Goods Sold in the Calculation of ending inventory. Beginning Inventory Net Purchases at Cost Goods Available For Sale Less: Estimated COGS Estimated Ending Inventory $40,000 110,000 ------------$150,000 -120,000 -----------$30,000