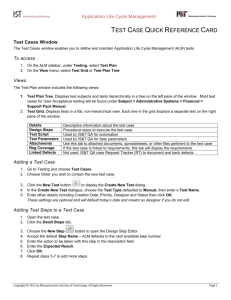

Optimal Decentralized ALM

Jules H. van Binsbergen, Stanford University

Michael W. Brandt, Duke University and NBER

Ralph S.J. Koijen, University of Chicago

Rotman ICPM Forum, Toronto

June 3-4 2008

© Michael W. Brandt, 2008

All rights reserved without exception

Motivation

Motivation

Decentralized investment management

• Institutions decentralize investment decisions along asset classes

– Example

CIO

Fixed Income

Portfolio Manager

Equities

Portfolio Manager

– Why?

Division of labor

Specialization ) Generating value (i.e., lower transaction cost or

positive alpha) within an asset class requires specialized skill

© Michael W. Brandt 2008

3

Optimal Decentralized ALM

Motivation

Misalignment of objectives

1. Suboptimal diversification

– Joint optimization by CIO over all assets dominates best

combination of portfolios optimized by portfolio managers

within asset-classes

– Sharpe (1981) and Elton and Gruber (2004)

2. Different risk preferences

– Portfolio managers take more or less risk than CIO desires

– CIO does not generally know the managers’ risk preferences

– van Binsbergen, Brandt, and Koijen (2008)

3. Mismatch risk between assets and liabilities

– Portfolio managers do not consider liabilities in their optimization

– Main motivation for this project

© Michael W. Brandt 2008

4

Optimal Decentralized ALM

Motivation

Benchmarking

• Performance benchmarks are commonly used to evaluate and

compensate portfolio managers

– Emphasis is on measuring effort or skill

– Benchmarks are taken as exogenously given (e.g., cash or index)

• We examine to what extent optimally designed benchmarks can

alleviate the misalignment induced by decentralization

• To be realistic, we focus on

– Benchmarks that are tradable portfolios and can be matched by

the portfolio managers (i.e., no cross-benchmarking)

– Benchmarks that do not depend on unknown quantities

– Unconditional benchmarks

© Michael W. Brandt 2008

5

Optimal Decentralized ALM

Motivation

Objective of our study

• Quantify in an intuitive way the economic cost of decentralization

– How much active skill do delegated portfolio managers have to

have in order to justify decentralization?

• Show how to construct benchmarks that perfectly align objectives

and achieve the same outcome as if the investment process was

centralized and the CIO had the skills of the portfolio managers

– Full benefits of diversification

– Optimal mismatch risk

– Optimal alpha overlay

© Michael W. Brandt 2008

6

Optimal Decentralized ALM

Motivation

Objective of our study (cont)

• Show how to operationalize our approach

– Our optimally constructed benchmarks depend on the portfolio

managers’ risk tolerances and active skill levels

– Three possibilities

Take an ex-ante stance on both sets of parameters

Construct an empirical cross-sectional distribution and

incorporate the resulting “parameter uncertainty”

Limit the role of both sets of parameters through constraints

Integrated and fully operational approach for decentralized

liability driven investment (LDI) management

© Michael W. Brandt 2008

7

Optimal Decentralized ALM

Problem setup

Problem setup

Pension fund

• CIO

– Liabilities

Exogenous with Treasury-like dynamics

– Assets

Centralized portfolio management (7 assets)

– Fixed income indices (Aaa, Baa, and Treasuries)

– Equity indices (Growth, Intermediate, Value)

– Cash

Decentralized portfolio management (3 assets)

– Fixed income manager

– Indices + orthogonal alpha technology

– Equities manager

– Indices + orthogonal alpha technology

– Cash

– Preferences = power utility over AT/LT

© Michael W. Brandt 2008

9

Optimal Decentralized ALM

Problem setup

Portfolio managers

• Fixed income manager (4 assets)

– Indices (Aaa, Baa, Treasuries)

– Independent alpha technology

– No cash position

– Preferences = power utility over A1T/B1T

• Equities manager (4 assets)

– Indices (Growth, Intermediate, Value)

– Independent alpha technology

– No cash position

– Preferences = power utility over A2T/B2T

• Two types of benchmarks (cash or optimally chosen)

© Michael W. Brandt 2008

10

Optimal Decentralized ALM

Cost of decentralization

Cost of decentralization

Decomposition

Cost of Decentralization

=

Suboptimal Diversification

+

Asset/Liability Mismatch

Alpha

© Michael W. Brandt 2008

12

Optimal Decentralized ALM

Cost of decentralization

Suboptimal diversification

• Cash benchmarks

• No alpha technologies

• Portfolio managers have relative risk aversion of 10

© Michael W. Brandt 2008

13

Optimal Decentralized ALM

Cost of decentralization

Centralized ALM

• CIO’s optimal allocation to the 6 risky assets

max SR weights

liability hedging weights

• Note

– No liability hedging with ° = 1 (log utility)

– Full liability immunization as ° ! 1

© Michael W. Brandt 2008

14

Optimal Decentralized ALM

Cost of decentralization

Centralized ALM (cont)

© Michael W. Brandt 2008

15

Optimal Decentralized ALM

Cost of decentralization

Decentralized ALM with cash benchmarks

• Both portfolio managers maximize their (absolute) SR

with

which includes their alpha technologies (technically ¤ ¤C)

• CIO invests optimally in the 2 managed portfolios and cash

© Michael W. Brandt 2008

16

Optimal Decentralized ALM

Cost of decentralization

Decentralized ALM with cash benchmarks (cont)

© Michael W. Brandt 2008

17

Optimal Decentralized ALM

Cost of decentralization

Cost of decentralization

• How much alpha do the portfolio managers have to add for the

CIO to be indifferent between centralized and decentralized ALM?

IR

© Michael W. Brandt 2008

18

Optimal Decentralized ALM

Optimal benchmarks for delegated ALM

Optimal benchmarks for decentralized ALM

Optimal benchmarks

• Response of the portfolio managers to benchmark with weights ¯i

• Note

– Benchmarks are ineffective with ° = 1 (log utility)

– Tracking error volatility ! 0 as ° ! 1

© Michael W. Brandt 2008

20

Optimal Decentralized ALM

Optimal benchmarks for decentralized ALM

Optimal benchmarks (cont)

• Understanding how portfolio managers respond to benchmarks,

the CIO’s optimal benchmark choice is

where xiC is the CIO’s optimal allocation to the portfolio manager’s

assets including the manager’s alpha technology

• These benchmarks induce the first-best solution

– Full benefits of diversification

– Optimal mismatch risk

– Optimal alpha overlay

Optimal benchmarks achieve the same outcome as if the

investment process was centralized and the CIO had the

skills of the portfolio managers

© Michael W. Brandt 2008

21

Optimal Decentralized ALM

Optimal benchmarks for decentralized ALM

Optimal benchmarks (cont)

© Michael W. Brandt 2008

22

Optimal Decentralized ALM

Optimal benchmarks for decentralized ALM

Optimal benchmarks (cont)

© Michael W. Brandt 2008

23

Optimal Decentralized ALM

Practical implementation

Practical implementation

Unknown quantities

• The optimal benchmarks depend on two unknown quantities

– Portfolio managers’ risk tolerance

– Portfolio managers’ active skill (IC)

• Unknown quantities can be dealt with the same way as they

usually are in portfolio choice problems

– “Plug-in” = pick values and proceed as if they known

– Bayesian = construct a subjective cross-sectional distribution of

risk tolerance and active skill levels (be careful, they are likely

highly correlated) and then integrate out the unknown quantities

© Michael W. Brandt 2008

25

Optimal Decentralized ALM

Practical implementation

Empirical solution

• Looking at past returns on active managers through the lens of a

structural model of delegated portfolio management (like ours),

we can learn a lot about managers’ risk preferences and skill

) Koijen (2008)

• Intuition

– Structural models predict how much beta exposure and active risk

managers take on as a function of their risk aversion and skill

– Beta exposure and active risk can be measured fairly accurately

(especially when compared to historical alpha estimates)

– These estimates can then be inverted to risk aversion and skill

© Michael W. Brandt 2008

26

Optimal Decentralized ALM

Practical implementation

Empirical solution (cont)

• E.g., cross-sectional distribution of relative risk aversion of U.S.

mutual fund managers

© Michael W. Brandt 2008

27

Optimal Decentralized ALM

Extensions and conclusions

Extension and conclusions

Extensions

• Long-only constraints

• Risk constraints at the portfolio manager level

• Alternative CIO preferences (van Binsbergen and Brandt, 2007)

• Other suggestions?

© Michael W. Brandt 2008

29

Optimal Decentralized ALM

Extension and conclusions

Conclusions

• Three contributions

– Quantify in an intuitive way the economic costs of decentralization

– Show how to construct benchmarks that perfectly align objectives

and achieve the same outcome as if the investment process was

centralized and the CIO had the skills of the portfolio managers

– Show how to operationalize our approach

• Integrated and fully operational approach for decentralized ALM

© Michael W. Brandt 2008

30

Optimal Decentralized ALM