4464-Chapter

advertisement

HFT 4464

Chapter 2

Financial Markets &

Financial Instruments

1

Chapter 2 Introduction

This chapter will provide an introduction to

financial markets and common financial

instruments.

Financial markets are where suppliers of

capital (firms) interact with buyers

(investors).

Often this is done through intermediaries

such as brokers.

2-2

Why Do People Invest?

Investing is not just something other

people do.

College education is an investment.

Investing is more than just hoping to

“make some money.”

It involves deferring present consumption

in the hopes of higher future consumption.

2-3

Equity Capital

Types of equity capital

Preferred stock

Common stock

This course focuses more on common

stock.

No guarantee of dividend

One share, one vote

Shareholders vote on key issues such as

composition of board of directors, choice

of auditing firm, and others.

2-4

Why Purchase Common Stock?

A purchaser is looking for at least one of

two possibilities:

1. Stream of dividend payments (current

income)

2. Increase in stock price (capital gain)

Holding period return:

{ ( (sales price – purchase price) + dividends ) / Purchase Price } x 100

2-5

Holding Period Return Example

You purchased a share of McDonald’s stock

one year ago for $18.00.

You earn $2.00 in dividends during the year.

Today you sell the stock for $18.50.

What is your holding period return?

(($18.50 – $18.00) + $2) / $18.00 = 0.1389

0.1389 x 100 = 13.89% (before taxes)

2-6

Bonds

Held by lenders

Receive repayment over time

Semi-annual interest payments

At maturity, amount is repaid (principal)

This is a series of cash flows that has value

Priced on an index relative to 100

If a $1,000 bond sells for “102,” it sells for

$1,020

2-7

How to Interpret Bond Information

Bond

Curr. Yld

Hilton 73/4 04

7.2%

Vol

40

Close Chg

101

+1/2

The Hilton bond pays 7.75% interest and matures in

2004.

The annual interest divided by the current price is

7.2 percent. (Note: this is not the return you will

receive if you hold the bond till maturity.)

40,000 bonds were traded that day.

The bond closed at $1,010 which is $.50 higher

than the previous day. 2-8

Capital Markets

Represents a diverse group of investments

Stock market

Bond market

Mortgage market

Futures market

2-9

Stock Market

New York Stock Exchange (NYSE)

Founded in 1792

Physical

location on Wall Street in

New York

Approximately

2,800 companies

offering securities here

Membership

offered in the form of

seats

2-10

Stock Market

Nasdaq

National Association of Securities Dealers

and Automated Quotations

Not

a physical location like the NYSE

(“over the counter”)

Represents

Fastest

a network of securities dealers

growing securities market

Makes

use of “market makers”—help

ensure liquidity of trading

2-11

Bond Market

Corporate bonds can be traded through the

NYSE

Most bonds are traded over the counter

Bond ratings

The

lower the letter, the greater the quality

Quality refers to the risk of default

Companies rating bonds

Standard

and Poor’s

Moody’s

2-12

Important Features of Bonds

How are bond prices and interest rates

related?

As interest rates rise, bond prices fall.

Some bonds are callable.

Company can repurchase bonds at a

certain price during a certain time.

2-13

Mortgage Market

Pooling of home mortgages by

government agencies

FNMA

and GNMA are two examples.

Mortgages

are packaged and resold

as securities to investors.

Investors

are often large institutional

investors like pension funds.

2-14

Money Market

Market for short-term debt instruments

Certificates of Deposit

Commercial

paper

Investors

loan to large companies for a very

short period of time (9 months or less).

Treasury

Loans

Bills / Bonds

to the U.S. Treasury

Zero-Coupon bonds

Issued at a discount—no interest payments

2-15

Risk Free Rate

Raising Capital

Primary market

Initial Public Offering (IPO)

Common

stock is sold to underwriter

(investment banker)

Investment banker sells to clients

2003 scandal/settlement

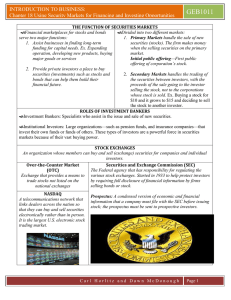

Secondary market

Investor to investor, where most

trading occurs

2-16

Features of Stock Trading

Bid vs. ask

Bid

is the price you will pay to own a share

Ask is the price you would receive to sell

your share

Difference goes to broker

Average NYSE trade takes 22 seconds

Significant reliance upon computers

Trading halt in June 2001

2-17

Hedging Risk

We can add value by decreasing the risk

(variability) of cash flows.

The concept of insurance as hedging:

You buy insurance and if nothing

happens to your house, you still have

the house.

If your house is damaged, insurance

pays for it and the house is rebuilt.

2-18

Forward and Futures Contracts

Spot price—price paid for a commodity today

Change in commodity prices present, risk to

buyer and seller

Example: Orange juice grower (seller) and

restaurant owner (buyer)

Prices help growers determine what and how

much to produce and restaurants need to

establish menu price

2-19

Forward Contracts

An agreement to sell an asset at a fixed

price for delivery in the future.

Cash payment is not required until delivery.

However, each party must trust the other to

perform.

The unique nature of each contract makes

them difficult to sell to third parties.

2-20

Futures Contracts

Similar to forward contracts, except:

Terms

of contract are standardized, such as

amounts and delivery dates.

Clearinghouse acts as go-between to help

ensure performance.

Contracts are traded on the Chicago Board of

Trade or Chicago Mercantile Exchange.

Most contracts are never delivered.

Parties take opposite positions to offset

original position.

2-21

Foreign Exchange

As international trade barriers are removed,

more business is conducted away from

home country.

Nearly 65% of McDonald’s 2002 revenues

originated from outside the U.S.

U.S. companies must report financial

operations in U.S. currency.

2-22

Foreign Exchange Example

You operate a hotel in France and accept

the Euro.

When the Euro strengthens, this means it

takes fewer Euros to buy $1 worth of goods.

As the Euro strengthens, your profits

increase upon conversion.

100,000Euros x $1/1Euro = $100,000 usd

100,000Euros x $2/1Euro = $200,000 usd

2-23

Can we hedge this risk?

Similar to commodities, we want to lock in a

“price” for our Euros—an exchange rate at

a future date.

We can buy a forward or futures contract to

accomplish this.

Who would be on the other side of this

transaction?

A French company (or other company

accepting the Euro) operating in the U.S.

2-24

Lenders to the Hospitality Industry

Commercial banks

Traditionally largest lender

Bank makes a “spread”—difference

between interest rate on loans and rate on

deposits

Interest = principal x rate x time

Types of loans

Fully amortized (principal and interest)

Interest only

2-25

Lenders to the Hospitality Industry

Real Estate Investment Trusts (REITS)

There

are equity and mortgage REITS

Special tax treatment if they pass through at

least 95 percent of earnings to investors

Insurance companies and pension funds

Receive

large monthly cash flows from

premiums and contributions

Try to match assets (loans) to liabilities (policies

and pension needs)

2-26

Measures of Stock Market Performance

Dow Jones Industrial Average

Index of 30 large companies

Weighted by stock price

Standard and Poor’s 500 (S&P 500)

500 companies

Fairly common measure of overall stock

market performance

Movement is similar to the Dow

2-27

Some Stock Market Statistics

Mean—weighted average

Mean

Dow annual return (1950–2001) = 9.01%

Mean S&P 500 annual return = 9.63%

Returns in a single year have varied from –

30% to +44%

This uncertainty around the mean is called

variance

Another measure is standard deviation, the

square root of the variance

2-28

Some Stock Market Statistics

Can we measure the relationship between

two individual stocks, two stock indices, or

an individual stock and a stock index?

Correlation coefficient =

Range is from –1.0 to +1.0

+1.0 is perfect positive correlation

-1.0 is perfect negative correlation

The Dow and the S&P 500 are highly

positively correlated

2-29

Homework Assignment

Problems 1,2,3,5,9

30