Managerial accounting

advertisement

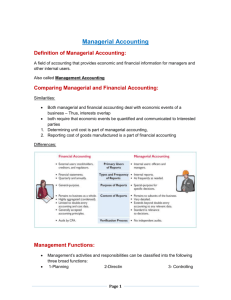

Islamic University of Gaza Managerial Accounting Chapter 1 Dr. Hisham Madi 1-1 What Is Managerial Accounting? Managerial accounting is a field of accounting that provides economic and financial information for managers and other internal users. Managerial accounting applies to all types of businesses. 1-2 Corporations Partnerships Proprietorships Not-for-profit Why Accounting is Essential for Decision Makers and Managers 1-3 Managerial accounting adds value to the organization by helping managers do their jobs more efficiently and effectively. Accounting information is used in decision making. MANAGERIAL ACCOUNTING vs. FINANCIAL ACCOUNTING 1-4 The Manager’s Role Management Functions Planning Directing Maximize short-term profit and market share. Commit to environmental protection and social programs. Add value to the business. 1-5 Coordinate diverse activities and human resources. Implement planned objectives. Provide incentives to motivate employees Hire and train employees. Produce smoothrunning operation. Controlling Keeping activities on track. Determine whether goals are met. Decide changes needed to get back on track. May use an informal or formal system of evaluations. Managerial Accounting Basics Organizational Structure Organization charts show the interrelationships of activities and the delegation of authority and responsibility within the company. 1-6 Managerial Accounting Basics 1-7 Stockholders own the corporation, but they manage it indirectly through a board of directors they elect. The board formulates the operating policies for the company or organization. The chief executive officer (CEO)has responsibility for managing the business. the CEO delegates responsibilities to other officers overall Managerial Accounting Basics 1-8 Responsibilities within the company are frequently classified as either line or staff positions. Employees with line positions are directly involved in the company’s primary revenue-generating operating activities. Examples of line positions include the vice president of operations, vice president of marketing, plant managers, supervisors, and production personnel. Employees with staff positions are involved in activities that support the efforts of the line employees. employees in finance, legal, and human resources have staff positions Managerial Accounting Basics 1-9 The chief financial officer (CFO)is responsible for all of the accounting and finance issues the company faces. The CFO is supported by the controller and the treasurer Business Ethics 1-10 All employees are expected to act ethically. Many organizations have codes of business ethics. Past financial frauds: ► Enron, ► Global Crossing, ► WorldCom Business Ethics Creating Proper Incentives Systems and controls sometimes create incentives for managers to take unethical actions. the budget is also used as an evaluation tool, some managers try to “game’’ the budgeting process by underestimating their division’s predicted performance so that it will be easier to meet their performance targets 1-11 Controls need to be effective and realistic. Business Ethics Code of Ethical Standards Sarbanes-Oxley Act (SOX) Clarifies management’s responsibilities. Requires certifications by CEO and CFO. Selection criteria for Board of Directors and Audit Committee. 1-12 Substantially increased penalties for misconduct. Manufacturing Costs Managers should ask questions such as the following. 1. What costs are involved in making a product or providing a service? 2. If we decrease production volume, will costs decrease? 3. What impact will automation have on total costs? 4. How can we best control costs? 1-13 Manufacturing Costs Manufacturing Costs Manufacturing consists of activities and processes that convert raw materials into finished goods. Merchandising, which sells merchandise in the form in which it is purchased 1-14 Manufacturing Costs Direct Materials Raw Materials Basic materials and parts used in manufacturing process. Direct Materials Raw materials that can be physically and directly associated with the finished product during the manufacturing process. Examples include flour in the baking of bread, syrup in the bottling of soft drinks, and steel in the making of automobiles 1-15 Manufacturing Costs Direct Materials Indirect Materials 1-16 Not physically part of the finished product or they are an insignificant part of finished product in terms of cost, because their physical association with the finished product is too small in terms of cost Considered part of manufacturing overhead. Manufacturing Costs Direct Labor Work of factory employees that can be physically and directly associated with converting raw materials into finished goods. Bottlers at Coca-Cola, and bakers at Sara Lee, are employees whose activities are usually classified as direct labor Indirect Labor Work of factory employees that has no physical association with the finished product or for which it is impractical to trace costs to the goods produced. 1-17 Manufacturing Costs Indirect Labor Work of factory employees that has no physical association with the finished product or for which it is impractical to trace costs to the goods produced. Examples include wages of factory maintenance people, factory time-keepers, and factory supervisors. Like indirect materials, companies classify indirect labor as manufacturing overhead 1-18 Manufacturing Costs Manufacturing Overhead Costs that are indirectly associated with manufacturing the finished product. Includes all manufacturing costs except direct materials and direct labor. Also called factory overhead, indirect manufacturing costs, or burden. 1-19 Manufacturing Costs 1-20 Allocating direct materials and direct labor costs to specific products is fairly straightforward. Good recordkeeping can tell a company how much plastic it used in making each type of gear, or how many hours of factory labor it took to assemble a part. But allocating overhead costs to specific products presents problems. How much of the purchasing agent’s salary is attributable to the hundreds of different products made in the same plant? Product Versus Period Costs Product Costs Direct materials Direct labor Manufacturing overhead Components: Costs that are an integral part of producing the finished product. 1-21 Recorded in “inventory” account. Not an expense (COGS) until the goods are sold. Product Versus Period Costs Period Costs Charged to expense as incurred. are costs that are matched with the revenue of a specific time period rather than included as part of the cost of a salable product. 1-22 Non-manufacturing costs. Includes all selling and administrative expenses. Product Versus Period Costs 1-23 A bicycle company has these costs: tires, salaries of employees who put tires on the wheels, factory building depreciation, wheel nuts, spokes, salary of factory manager, handlebars, and salaries of factory maintenance employees. Classify each cost as direct materials, direct labor, or overhead. Direct Materials Tires. Spokes. Handlebars. 1-24 Direct Labor Salaries of employees who put tires on the wheels. Overhead Factory depreciation. Factory manager salary. Factory maintenance employees salary. Manufacturing Costs in Financial Statements Income Statement Under a periodic inventory system, the income statements of a merchandiser and a manufacturer differ in the cost of goods sold section. “COGS” 1-25 Manufacturing Costs in Financial Statements Cost of Goods Manufactured Cost of Goods Sold Components – (Periodic Inventory System) 1-26 Manufacturing Costs in Financial Statements Cost of goods sold sections of merchandising and manufacturing income statements 1-27 Manufacturing Costs in Financial Statements Determining the Cost of Goods Manufactured Total Work in Process – (1) cost of beginning work in process and (2) total manufacturing costs for the current period. Total Manufacturing Costs – sum of direct material costs, direct labor costs, and manufacturing overhead in the current year. 1-28 Illustration 1-8 1-29 Manufacturing Costs in Financial Statements Balance Sheet Inventory accounts for a manufacturer The balance sheet for a merchandising company shows just one category of inventory. 1-30 Manufacturing Costs in Financial Statements Balance Sheet Current assets sections of merchandising and manufacturing balance sheets 1-31 Managerial Accounting Today Focus on the Value Chain Refers to all business process associated with providing a product or service. For a manufacturing firm these include the following: 1-32 Managerial Accounting Today Just-In-Time Inventory Methods Inventory system in which goods are manufactured or purchased just in time for sale. Total Quality Management (TQM) 1-33 Reduce defects in finished products, with the goal of zero defects. Managerial Accounting Today Theory of Constraints Constraints (“bottlenecks” ) limit the company’s potential profitability. A specific approach to identify and manage these constraints in order to achieve company goals. Enterprise Resource Planning (ERP) 1-34 Software programs designed to manage all major business processes. Managerial Accounting Today Activity-Based Costing (ABC) 1-35 Allocates overhead based on use of activities. Results in more accurate product costing and scrutiny of all activities in the value chain. Managerial Accounting Today Balanced Scorecard 1-36 Evaluates operations in an integrated fashion. Uses both financial and non-financial measures. Links performance to overall company objectives. 1-37