and Media Services")

Pensions and

Other

Postretirement

Benefits

17

Copyright © 2007 by The McGraw-Hill Companies, Inc. All rights reserved.

17-2

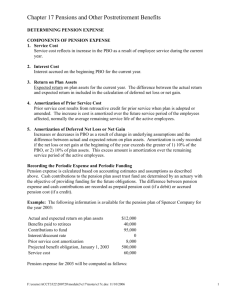

Nature of Pension Plans

I agree to make payments

into a fund for future

retirement benefits for

employee services.

Sponsor

I am the employee for

whom the pension plan

provides benefits.

Participant

17-3

Nature of Pension Plans

1.

2.

3.

4.

5.

For a pension plan to qualify for special tax

treatment it must meet the following

requirements:

Cover at least 70% of employees.

Cannot discriminate in favor of highly

compensated employees.

Must be funded in advance of retirement through

a trust.

Benefits must vest after a specified period of

service.

Complies with timing and amount of contributions.

17-4

Nature of Pension Plans

The right to receive earned pension

benefits vest (vested benefits) when it is

no longer contingent on continued

employment.

17-5

Learning Objectives

Explain the fundamental differences between a

defined contribution pension plan and a

defined benefit pension plan.

17-6

Defined Contribution

Plans

Contributions are

established by

formula or

contract.

Employer deposits

an agreed-upon

amount into an

employee-directed

investment fund.

Employee

bears all risk of

pension fund

performance.

17-7

Defined Benefit

Pension Plans

Employer is

committed to

specified

retirement

benefits.

Retirement

benefits are based

on a formula that

considers years of

service,

compensation

level, and age.

Employer bears

all risk of

pension fund

performance.

17-8

Defined Benefit Plan

Pension expense is measured by

assigning pension benefits to periods

of employee service as defined by the

pension benefit formula.

A typical benefit formula might be:

1% × Years of Service × Final year’s salary

So, for 35 years of service and a final salary of $80,000,

the employee would receive:

1% × 35 × $80,000 = $28,000 per year

17-9

Pension Expense – An Overview

Components of Pension Expense

+

Service cost ascribed to employee service this period

+

Interest accrued on pension liability

+ or - Return on plan assets

+

Amortized portion of Prior Service Cost

+ or - Losses or gains from revision of pension liability and plan assets

=

Pension expense

17-10

Learning Objectives

Distinguish among the vested benefit

obligation, the accumulated benefit obligation,

and the projected benefit obligation.

17-11

Pension Obligation

Present value of

additional benefits

related to projected

pay increases.

Present value of

nonvested benefits

at present pay

levels.

Present value of

benefits at present

pay levels.

Projected Benefit

Obligation

Accumulated

Benefit Obligation

Vested Benefit

Obligation

VBO ABO PBO

17-12

Learning Objectives

Describe the five events that might change the

balance of the PBO.

17-13

Projected Benefit Obligation

The PBO changes as a result of:

Cause

Service Cost

Interest Cost

Prior Service

Cost

Loss or Gain on

PBO

Retiree Benefits

Paid

Effect

+

+

+

+ or -

Frequency

Each period

Each period (except the first period of

the plan)

Only if the plan is amended (or initiated)

that period

Whenever revisions are made in the

pension liability estimate

Each period (unless no employees have

yet retired under the plan)

17-14

Pension Obligation

The PBO changes as a result of:

Cause

Service Cost

Effect

+

Frequency

Each period

Each period (except the first period of

Interest

Cost

Service

cost

+ is the increase

the plan)in the

Prior

Service

the plan is amended

(or initiated)

PBO

attributableOnly

toif employee

service

Cost

+

that period

performed

during

the

period.

Loss or Gain

on

Whenever

revisions

are made in the

PBO

+ or pension liability estimate

Retiree Benefits

Each period (unless no employees have

Paid

yet retired under the plan)

17-15

Pension Obligation

The PBO changes as a result of:

Cause

Service Cost

Effect

+

Frequency

Each period

Each period (except the first period of

Interest Cost

+

the plan)

Prior Service

Only if the plan is amended (or initiated)

Interest cost

is the interest

on the

Cost

+

that period

Loss or Gain on

Whenever

revisions are made in the

PBO during

the period.

PBO

+ or pension liability estimate

Retiree Benefits

Each period (unless no employees have

Paid

yet retired under the plan)

17-16

Pension Obligation

The PBO changes as a result of:

Cause

Service Cost

Effect

+

Frequency

Each period

Each period (except the first period of

Interest Cost

+

the plan)

Prior Service

Only if the plan is amended (or initiated)

Cost

+

that period

Loss or Gain on

Whenever revisions are made in the

Prior

result

from

PBO service

+ or -cost effects

pension liability

estimate

Retiree changes

Benefits

Eachpension

period (unlessbenefit

no employees have

in the

Paid

yet retired under the plan)

formula or plan terms.

17-17

Pension Obligation

The PBO changes as a result of:

Cause

Service

Costor

Loss

Effect

Frequency

+ on PBO results

Each period

gain

from

Each period (except the first period of

Interest

Cost revisions of estimates used

required

+

the plan)

Prior Service to determine

Only if the plan

is amended (or initiated)

PBO.

Cost

+

that period

Loss or Gain on

Whenever revisions are made in the

PBO

+ or pension liability estimate

Retiree Benefits

Each period (unless no employees have

Paid

yet retired under the plan)

17-18

Pension Obligation

The PBO changes as a result of:

Cause

Service Cost

Effect

+

Frequency

Each period

Each period (except the first period of

Interest Cost

plan)the

Retiree+benefits paidtheare

Prior Service

Only if the plan is amended (or initiated)

result of paying

benefits

retired

Cost

+

thatto

period

Loss or Gain on

Whenever revisions are made in the

employees.

PBO

+ or pension liability estimate

Retiree Benefits

Each period (unless no employees have

Paid

yet retired under the plan)

17-19

Learning Objectives

Explain how plan assets accumulate to provide

retiree benefits and understand the role of the

trustee in administering the fund.

17-20

Pension Plan Assets

Pension plan assets (like the PBO) are not

formally recognized on the balance sheet.

A trustee manages the pension plan assets.

17-21

Pension Plan Assets

OVERFUNDED

Market value of plan

assets exceeds the

actuarial present value

of all benefits earned by

participants.

UNDERFUNDED

Market value of plan

assets is below the

actuarial present value

of all benefits earned by

participants.

17-22

Learning Objectives

Describe how pension expense is a composite

of periodic changes that occur in both the

pension obligation and the plan assets.

17-23

Pension Expense

Pension expense is the net cost of:

Service cost

Interest cost

Return on plan assets

Amortization of prior service costs

Gain or loss recognized.

17-24

Defined Benefit Plan

You go to work for Matrix, Inc. on 1/1/06. You are eligible to participate

in the company's defined benefit pension plan. The benefit formula is:

×

×

Annual salary in year of retirement

Number of years of service

1.5%

Annual retirement benefits

You are 25 years old when you start work and may accumulate 40 years

of service before retiring at age 65. If your salary is $200,000 during

your last year of service, you will receive the following annual benefits:

$200,000

×

40

×

1.5%

$120,000

You are not required to make any contributions. The plan vests at the

rate of 20% per year. The plan actuary estimates that upon reaching

age 65, you will receive payments for 15 years. The actuary uses an

8% discount rate in all present value computations.

17-25

Defined Benefit Plan

At December 31, 2006, the end of your first year of service, the

actuary must calculate the present value of the pension benefits

earned by you during 2005. Remember that you will not receive

pension benefits until you are 65 and the actuary estimates

payments will be made for 15 years after you retire. After one year

of service you will have earned $3,000 in pension benefits:

Pension benefits = .015 × 1 yr of service × $200,000

Pension benefits = $3,000

Service cost is the present value of these benefits and is calculated

as follows:

Service cost = $3,000 × 8.559481 × .0497132

Service cost = $1,277

1Present

value of an ordinary annuity at 8% for 15 years.

2Present value of $1 at 8% for 39 years.

17-26

Defined Benefit Plan

Based on the given information, the actuary calculates

your accumulated benefit obligation (ABO) as follows:

Retirement benefits = .015 × 1 yr × $25,000

Retirement benefits = $375

ABO = $375 × 8.55948 × .049713

ABO = $160

Your vested benefit obligation (VBO) is calculated as

follows:

Vested benefits = .015 × 1 × $25,000 × .2

Vested benefits = $75

VBO = $75 × 8.55948 × .049713

VBO = $32

17-27

Defined Benefit Plan

A reconciliation of the VBO, ABO and PBO would look like this:

VBO

$

32

Non-vested benefits

128

ABO

Adjustment for future salary

PBO

$

$

160

478

638

The adjustment for future salary of $478, is determine by the

plan actuary. If you are the only employee at Matrix, the

computations would be similar for future years. Let’s assume

Matrix funds $500 of its pension costs with the plan trustee on

December 31, 2006. The journal entry to record the pension

costs and funding would be:

Pension expense

Accrued pension cost

Cash

638

138

500

17-28

Defined Benefit Plan

Let’s look at an example for Matrix, Inc.

Components of Pension Expense

+

Service cost ascribed to employee service this period

+

Interest accrued on pension liability

+ or - Return on plan assets

+

Amortized portion of prior service cost

+ or - Losses or gains from revision of pension liability and plan assets

=

Pension expense

17-29

Defined Benefit Plan

Actuaries have determined that Matrix, Inc.

has service cost of $150,000 in 2006 and

$155,000 in 2007.

We can begin the process of determining

pension expense for the company.

17-30

Service Cost

1. Service Cost

2006

$ 150,000

2007

$ 155,000

Total Pension Expense

$ 150,000

$ 155,000

17-31

Interest Cost

Interest cost is the growth in PBO

during a reporting period.

Interest cost is calculated as:

PBOBeg × Discount rate

17-32

Interest Cost

Actuaries determined that Matrix, Inc.

had PBO of $500,000 on 1/1/06, and

$640,000 on 1/1/07.

The actuary uses a discount rate of 10%.

17-33

Interest Cost

1. Service Cost

2. Interest Cost

2006

$ 150,000

50,000

2007

$ 155,000

64,000

Total Pension Expense

$ 200,000

$ 219,000

2006: PBO 1/1/06 $500,000 × 10% = $50,000

2007: PBO 1/1/07 $640,000 × 10% = $64,000

17-34

Return on Plan Assets

Actual

Return

Expected

Return

The dividends, interest,

and capital gains

generated by the fund

during the period.

Trustee’s estimate of

long-term rate of

return.

17-35

Return on Plan Assets

The plan trustee reports that plan

assets were $450,000 on 1/1/06,

and $600,000 on 1/1/07.

The trustee uses an expected return

of 9% and the actual return is 10%

in both years.

17-36

Return on Plan Assets

2006

Beginning value of plan assets

Rate of return

Return on plan assets

Beginning value of plan assets $ 450,000

Adjustment (10% - 9%)

1%

Adjusted for gain on plan assets

Expected return on plan assets

$

$

450,000

10%

45,000

4,500

40,500

2007

Beginning value of plan assets

Rate of return

Return on plan assets

Beginning value of plan assets $ 600,000

Adjustment (10% - 9%)

1%

Adjusted for gain on plan assets

Expected return on plan assets

$

$

600,000

10%

60,000

6,000

54,000

17-37

Return on Plan Assets

1. Service Cost

2. Interest Cost

3. Return on Plan Assets

2006

$ 150,000

50,000

(40,500)

2007

$ 155,000

64,000

(54,000)

Total Pension Expense

$ 159,500

$ 165,000

17-38

Amortization of Prior Service Cost

Prior service cost (PSC) results from plan

amendments granting increased pension

benefits for service rendered before the

amendment.

PSC is the present value of the retroactive

benefits, and increases PBO.

17-39

Amortization of Prior Service Cost

Benefits attributable to prior service are

assumed to benefit future periods by:

Improving employee productivity.

Improving employee morale.

Reducing turnover.

Reducing demands for pay raises.

17-40

Amortization of Prior Service Cost

PSC is amortized over the remaining service period

of those employees active at the date of the

amendment who are expected to receive benefits

under the plan.

If most of a plan’s participants are inactive, then

amortize PSC over the participants’ remaining life

expectancy.

17-41

Amortization of Prior Service Cost

Two approaches to amortizing PSC:

Straight-line method

Amortize PSC over the average remaining

service period.

Service method

Amortize PSC by allocating equal amounts to

each employee’s service years remaining.

17-42

Amortization of Prior Service Cost

Effective 1/1/07, Matrix, Inc. amends the retirement

plan to provide increased benefits attributable to

service performed before 1/1/03, for all active

employees.

The present value of the increased benefits (PSC) at

1/1/07, is $60,000.

The average remaining service life of the active

employee group is 12 years.

17-43

Amortization of Prior Service Cost

Since the amendment was not effective

until the beginning of 2007, pension

expense for 2006 is not affected.

2007: $60,000 PSC ÷ 12 = $5,000

17-44

Amortization of Prior Service Cost

1. Service Cost

2. Interest Cost

3. Return on Plan Assets

4. Amortization of PSC

2006

$ 150,000

50,000

(40,500)

0

2007

$ 155,000

64,000

(54,000)

5,000

Total Pension Expense

$ 159,500

$ 170,000

17-45

Gains and Losses

Higher than

Expected

Lower than

Expected

Projected

Benefits

Obligation

Return on

Plan Assets

Loss

Gain

Gain

Loss

17-46

Corridor Amount

Amortization is not required if the net

unrecognized gain or loss at the

beginning of the period is a minimum

amount (corridor amount).

17-47

Corridor Amount

The corridor

amount is 10% of

the greater of . . .

PBO at the

beginning of the

period.

Or

Fair value of plan

assets at the

beginning of the

period.

17-48

Gains and Losses

If the beginning net unrecognized gain or

loss exceeds the corridor amount,

amortization is recognized as . . .

Net unrecognized gain or loss

Corridor

—

at beginning of year

amount

Average remaining service period of active employees

expected to receive benefits under the plan

17-49

Gains and Losses

There was no gain or loss amortized in 2006.

Amounts at January 1, 2007

PBO

Fair value of plan assets

Net gain for 2007

Average service life

$ 640,000

600,000

73,000

9

Let’s determine the amortization of the

net gain in 2007.

17-50

Gains and Losses

Corridor amount ($640,000 x 10%)

Net gain for 2007

Gain in excess of corridor

$ 64,000

73,000

$ 9,000

$9,000 ÷ 9 years = $1,000 per year.

17-51

Pension Expense

1. Service Cost

2. Interest Cost

3. Return on Plan Assets

4. Amortization of PSC

5. Gain Amortized

Total Pension Expense

2006

$ 150,000

50,000

(40,500)

0

0

$ 159,500

2007

$ 155,000

64,000

(54,000)

5,000

(1,000)

$ 169,000

17-52

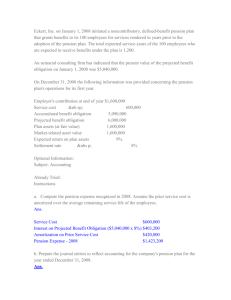

Pension Expense

Matrix contributed $200,000 to the plan

trustee at the end of 2007. The journal entry

to record the pension expense is:

GENERAL JOURNAL

Date

Description

Dec 31 Pension Expense

Prepaid Pension Cost

Cash

Debit

Credit

169,000

31,000

200,000

17-53

Learning Objectives

Understand the interrelationships among the

elements that constitute a defined benefit

pension plan.

17-54

Reconciliation of Pension Amounts

Four “off-balance sheet” accounts:

PBO

Plan Assets

Unamortized PSC

Unamortized Gain or Loss

17-55

Reconciliation of Pension Amounts

The four amounts shown on the

previous slide combine to account for

the one pension account that is

reported on the balance sheet:

prepaid pension asset or pension

liability.

17-56

Minimum Liability

To discourage underreporting of

pension liability, SFAS No. 87

requires recognition of an additional

minimum pension liability under

certain circumstances.

17-57

Measurement Issue

Accumulated Benefit Obligation (ABO)

- Plan Assets at Fair Value

Minimum Pension Liability

This amount is also called the

underfunded ABO.

17-58

Offsetting

SFAS No. 87 requires offsetting of the

pension liability and the plan assets

when determining the minimum liability.

17-59

Additional Liability

An additional pension liability is recognized if total

minimum liability exceeds accrued pension cost.

Total minimum liability

– Accrued pension cost balance (liability)

Additional pension liability balance

Total minimum liability

+Prepaid pension cost balance (asset)

Additional pension liability balance

17-60

Learning Objectives

Describe how pension disclosures fill a

reporting gap left by the minimal disclosures in

the primary financial statements.

17-61

Pension Disclosures – A Compromise

The pension information actually reported in the financial

statements falls short of the conceptual ideal and even shy

of the FASB’s own preferences. Here are the items

included in the income statement and balance sheet.

Income Statement

Pension expense

Balance Sheet

Assets:

Intangible pension asset

Liabilities:

Pension liability

Shareholders' equity:

Accumulated other comprehensive income:

Unrealized pension cost

17-62

Settlements and Curtailments

Pension plan settlements

Reduce PBO and are viewed as the realization of a

portion of the net unrecognized gain or loss and a

portion of the unrecognized transition asset.

Pension plan curtailments

Often reduce PBO, resulting in a gain, which reduces

accrued pension cost.

17-63

Learning Objectives

Describe the nature of postretirement benefit

plans other than pensions and identify the

similarities and differences in accounting for

those plans and pensions.

17-64

Postretirement Benefit Plan

Encompass all types of retiree health and

welfare benefits including . . .

Medical coverage,

Dental coverage,

Life insurance,

Group legal services, and

Other benefits.

Postretirement Health Benefits and

Pension Benefits Compared

Pension Plan Benefits

Usually based on

years of service.

Identical payments

for same years of

service.

Cost of plan usually

paid by employer.

Vesting usually

required.

Postretirement Health

Benefits

Typically unrelated to

service.

Payments vary

depending on

medical needs.

Company and retiree

share the costs.

True vesting does not

exist.

17-65

17-66

The Net Cost of Benefits

Estimated medical

costs in each

year of retirement

Less:

Equals:

Retiree

share of

cost

Medicare

payments

Estimated net

cost of benefits

17-67

The Net Cost of Benefits

Estimating postretirement health care benefits is

like estimating pension benefits, but there are

some additional assumptions required:

Current

cost of providing health care benefits (per

capita claims cost).

Demographic characteristics of participants.

Benefits provided by Medicare.

Expected health care cost trend rate.

17-68

Learning Objectives

Explain how the obligation for postretirement

benefits is measured and how the obligation

changes.

17-69

Postretirement Benefit Obligation

Expected (EPBO)

The actuary’s estimate of the total

postretirement benefits (at their

discounted present value) expected

to be received by plan participants.

Accumulated (APBO)

The portion of the EPBO

attributed to employee

service to date.

17-70

Measuring the Obligation

On December 31, our actuary estimates that the

present value of the expected benefit obligation for

your postretirement health care costs is $10,250.

You have worked for the company for 6 years and

are expected to have 30 years of service at

retirement. The actuary uses a 6% discount rate.

Let’s calculate the APBO.

17-71

Measuring the Obligation

EPBO

×

Fraction

attributed to

APBO

=

service to

date

$10,250 ×

6

30

= $2,050

APBO at the beginning of the year.

17-72

Measuring the Obligation

To calculate the APBO at the end of the year,

we start by determining the ending EPBO.

EPBO

Beginning

of Year

×

(1 + Discount Rate)

=

EPBO

End

of Year

$10,250 × 1.06 = $10,865

7

$10,865 ×

= $2,535

30

APBO End

of Year

17-73

Measuring the Obligation

APBO may also be calculated like this:

APBO beginning of the year

Interest cost ($2,050 × 6%)

Service cost ($10,865 × 1/30)

APBO end of the year

$ 2,050

123

362

$ 2,535

The APBO increases because of interest

and the service fraction (service cost).

17-74

Attribution

The process of assigning the cost of

benefits to the years during which

those benefits are assumed to be

earned by employees.

17-75

Learning Objectives

Determine the components of postretirement

benefit expense.

17-76

Postretirement Benefit Expense

Component

Service Cost

Interest Cost

Return on Plan Assets

Prior Service Cost

Losses or Gains

Transition Amount

Postretirement Benefit Expense

Portion of the EPBO attributed to

the current period.

Increase in APBO due to the

passage of time.

Earnings on plan investments, if

plan is funded.

Amortization of compensation cost

from amending the plan. Often a

negative amount.

Amortization of unexpected

changes in either the obligation or

plan assets.

Amortization of the APBO existing

when SFAS 106 was adopted.

17-77

Postretirement Benefit Expense

Component

Postretirement Benefit Expense

Portion of the EPBO attributed to

the current period.

Increase in APBO due to the

Interest Cost

passage of time.

Earnings on plan investments, if

Return

on

Plan

Assets

Interest accrues onplan

theisAPBO

as time passes.

funded.

APBO at the beginning

of theofyear

times thecost

Amortization

compensation

assumed

discount from

rate amending

equals the

cost.a

Prior

Service Cost

theinterest

plan. Often

negative amount.

Amortization of unexpected

Losses or Gains

changes in either the obligation or

plan assets.

Amortization of the APBO existing

Transition Amount

when SFAS 106 was adopted.

Service Cost

17-78

Postretirement Benefit Expense

Component

Postretirement Benefit Expense

Portion of the EPBO attributed to

the current period.

Increase in APBO due to the

Interest Cost

passage of time.

Earnings on plan investments, if

Return on Plan Assets

plan is funded.

Amortization of compensation cost

Unlike pension plans,

many postretirement benefit

Prior Service Cost

from amending the plan. Often a

plans are not funded currently. For funded plans, the

negative amount.

earnings on plan assets

reduce postretirement

Amortization of unexpected

benefit

expense.

Losses or Gains

changes

in either the obligation or

plan assets.

Amortization of the APBO existing

Transition Amount

when SFAS 106 was adopted.

Service Cost

17-79

Postretirement Benefit Expense

Component

Postretirement Benefit Expense

Portion of the EPBO attributed to

the current period.

Increase in APBO due to the

Interest Cost

passage of time.

Earnings on plan investments, if

Return on Plan Assets

plan is funded.

Amortization of compensation cost

Prior Service Cost

from amending the plan. Often a

negative amount.

Amortization of unexpected

Prior service cost is

allocated over the average

Losses or Gains

changes in either the obligation or

time from the date of the amendment to the date

plan assets.

for active employees,

not the

expected

Amortization

of the

APBO existing

date.

Transition Amount retirement

when SFAS

106 was adopted.

Service Cost

17-80

Postretirement Benefit Expense

Component

Postretirement Benefit Expense

Portion of the EPBO attributed to

the current period.

Increase in APBO due to the

Interest Cost

passage of time.

The amount subject to amortization

is the

net gain or

Earnings on plan

investments,

if loss at

Return on Plan Assets

plan

is funded.

the beginning of the year

in excess

of 10% of the APBO or

cost the

10% of the plan assets.Amortization

The excessofiscompensation

amortized over

Prior Service

Cost

from amending

plan.employees.

Often a

average

remaining

service

period ofthe

active

negative amount.

Amortization of unexpected

Losses or Gains

changes in either the obligation or

plan assets.

Amortization of the APBO existing

Transition Amount

when SFAS 106 was adopted.

Service Cost

17-81

Amortize Net Losses or Gains

APBO

Return on

Plan Assets

Higher Than Expected

Loss

Gain

Lower Than Expected

Gain

Loss

17-82

Postretirement Benefit Expense

Component

Postretirement Benefit Expense

Portion of the EPBO attributed to

the current period.

Increase in APBO due to the

Interest Cost

passage of time.

Earnings on plan investments, if

Return on Plan Assets

plan is funded.

Amortization of the transition

amount is part of expense in the

Amortization of compensation cost

current

period.

reporting,

Prior

ServiceFor

Costfinancial

from

amendingthe

the amortization

plan. Often a reduces

current earnings. For income

tax amount.

purposes, income is reduced

negative

when actual payments are

made. This

creates a temporary

Amortization

of unexpected

difference

financial

and taxable

income.

Losses

or Gainsbetweenchanges

in either

the obligation

or

plan assets.

Amortization of the APBO existing

Transition Amount

when SFAS 106 was adopted.

Service Cost

17-83

Amortization of Transition Amount

An employer may choose to recognize:

The entire transition obligation immediately,

or

Amortize the transition obligation on a straightline basis over the plan participants’ future

service periods (or 20 years if that is longer).

17-84

Determining the Expense

Recall our example of postretirement benefits.

APBO beginning of the year $ 2,050

Interest cost ($2,050 × 6%)

123

Service cost ($10,865 × 1/30)

362

APBO end of the year

$ 2,535

Let’s calculate postretirement benefits expense.

17-85

Determining the Expense

Service cost

$

362

Interest cost

123

Because

most

healthNone

plans

Actual return

onpostretirement

plan assets

are

not funded,

there

arecost

no fund assets,

Amortization

of prior

service

None

noAmortization

credit for of

prior

service, and no net

loss.

net loss

None

Amortization of transition liability

85

Postretirement benefit expense

$

570

The beginning APBO ($2,050) is the initial transition liability.

Your service life is 24 years (30 - 6). The amortization amount

is $85 rounded ($2,050 ÷ 24 years).

17-86

Pension Disclosures

The disclosure requirement of pension plans and

postretirement benefits are very similar. On this and the

next three screens are the disclosures for FedEx in the

Appendix to Chapter 1.

• Description of the pension plan.

• Estimates of the obligations PBO, ABO, vested benefit

obligation, EPBO, and APBO).

17-87

Pension Disclosures

• The percentage of total plan assets for each major

category of assets (equity securities, debt securities, real

estate, other) as well as a description of investment

strategies, including any target asset allocations and risk

management practices.

• A breakdown of the components of the annual pension and

postretirement benefit expenses for 2004, 2003, and 2002.

17-88

Pension Disclosures

• A reconciliation of the changes in the plans’ benefit

obligation and fair value of assets over a two year period

ended May 31, 2004, and a statement of the funded

status.

• The discount rates, the assumed rate of compensation

increases used to measure the PBO, the expected longterm rate of return on plan assets and the expected rate

of increase in future medical and dental benefit costs.

17-89

Pension Disclosures

• Estimated benefit payments presented separately for

years 2005-2009 and in the aggregate for years 20102014.

• Estimate of expected contributions to fund the plan for

2005.

• Other information to make it possible for interested

analysts to reconstruct the financial statements with plan

assets and liabilities included

17-90

Service Method of

Allocating Prior

Service Cost

Appendix 17

17-91

The Service Method

The allocation approach that reflects the declining

service pattern of employees is called the service

method. The method requires that the total number of

service years for all employees be calculated. This

calculation is usually done by the actuary.

Assume Matrix, Inc. has 2,000 employees and the

company’s actuary determined that the total number of

service years of these employees is 30,000. We would

calculate the following amortization fraction:

30,000

2,000

= 15 average service years

17-92

End of Chapter 17

and Media Services")