Chapter 2

The Pursuit of the

Conceptual Framework

Introduction

What is the conceptual framework?

The Early Theorists

Paton and Canning

DR Scott and his conceptual framework

Early Authoritative and Semi-authoritative

Organizational Attempts to Develop the Conceptual

Framework of Accounting

A Tentative

Statement of

Accounting

Principles

Affecting

Corporate

Reports

A

Statement

of

Accounting

Principles

APB

Statement

No. 4

An

Introduction

to Corporate

Accounting

Standards

ASOBAT

ARSs

No. 1

and

No. 3

The Trueblood Committee

1.

2.

3.

4.

Committee report specified the following

four information needs of users:

Making decisions concerning the use of limited resources

Effectively directing and controlling organizations

Maintaining and reporting on the custodianship of resources

Facilitating social functions and controls

Objectives of financial reporting

Statement on Accounting Theory and

Theory Acceptance

Rationale for the committee’s approach

The approaches to accounting theory

were condensed into

1.

2.

3.

Classical

Decision Usefulness

Information Economics.

Criticisms of the approaches to theory

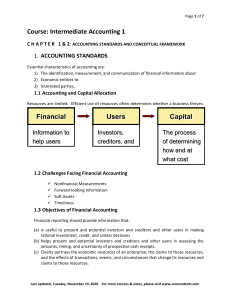

The FASB’s Conceptual Framework

Project

The objectives identify the goals

and purposes of financial

accounting; whereas, the fundamentals are the

underlying concepts that help achieve those objectives.

These concepts are designed to provide guidance in:

1.

2.

3.

Selecting the transactions, events and circumstances to be

accounted for

Determining how the selected transactions, events, and

transactions should be measured

Determining how to summarize and report the results of events,

transactions and circumstances.

SFAC No. 1 “Objectives of Financial

Reporting By Business Enterprises”

1.

2.

3.

4.

5.

6.

7.

Assess cash flow prospects

Report on enterprise resources,

claims against resources and changes in them

Report economic resources, obligations and owners

equity

Report enterprise performance and earnings

Evaluate liquidity, solvency, and flow of funds

Evaluate management stewardship and performance

Explain and interpret financial information

No. 2 “Qualitative Characteristics of

Accounting Information

Addresses the question: What makes

accounting information useful?

Develops a Hierarchy of Accounting

Qualities

A Hierarchy of Accounting Qualities

Users of Accounting

Information

Decision makers

and their characteristics

(for example, understanding

of prior knowledge)

Pervasive Constraint

Benefits > Costs

Understandability

User-specific qualities

Decision Usefulness

Primary Decision-specific

qualities

Relevance

Reliability

Timeliness

Ingredients of

primary qualities

Predictive

value

Verifiability

Neutrality

Feedback

value

Comparability and Consistency

Threshold for

recognition

Materiality

Representational

Faithfulness

No. 5 “Recognition and Measurement in

Financial Statements of Business

Enterprises”

Sets forth recognition criteria and

guidance on what information should be incorporated

into financial statements and when this information

should be reported

Defined comprehensive income as:

Revenues

Less: Expenses

Plus: Gains

Less: Losses

= Earnings

Earnings

Plus or minus cumulative

accounting adjustments

Plus or minus other

non-owner changes in equity

= Comprehensive Income

No. 5 “Recognition and Measurement

in Financial Statements of Business

Enterprises”

Measurement Issues

1.

Definitions.

2.

The item meets the definition of an element contained in

SFAC No. 6.

Measurability.

3.

It has a relevant attribute measurable with sufficient

reliability.

Relevance.

4.

The information about the item is capable of making a

difference in user decisions.

Reliability.

The information is representationally faithful, verifiable, and

neutral.

No. 6 “The Elements of Financial

Statements”

Defines the ten elements of financial

statements that are used to measure the

performance and position of economic

entities

These elements are discussed

in more depth in Chapters 6

and 7.

SFAC No. 7 “Using Cash Flow Information

and Present Value in Accounting

Measurements”

Accounting measurement is a very broad topic.

Consequently, the FASB focused on a series of questions relevant to

measurement and amortization conventions that employ present

value techniques. Among these questions are:

What are the objectives of using present value in the initial recognition of

assets and liabilities? And, do these objectives differ in subsequent

fresh-start measurements of assets and liabilities?

Does the measurement of liabilities at present value differ from the

measurement of assets?

How should the estimates of cash flows and interest rates be

developed?

What are the objectives of present value when used in conjunction with

the amortization of assets and liabilities?

How should present value amortizations be used when the estimates of

cash flows change?

SFAC No. 7 “Using Cash Flow Information and Present

Value in Accounting Measurements”

Present value measurements that fully captures the

economic differences between assets should include the

following elements:

1.

An estimate of the future cash flows

2.

Expectations about variations in the timing of those cash flows

3.

The time value of money represented by the riskfree rate of interest

4.

The price for bearing the uncertainty

5.

Other, sometimes unidentifiable, factors including illiquidity and

market imperfections

SFAC No. 7 “Using Cash Flow Information and

Present Value in Accounting Measurements”

Approaches to present value

1.

2.

Traditional

Expected cash flow

Incorporating probabilities

The objective is to estimate the value of the assets

required currently to settle the liability with the holder

or transfer the liability to an entity with a comparable

credit standing

Use of the interest method

Principles Based vs. Rules Based

Accounting Standards

Continuum ranging from

highly rigid standards on one end

to general definitions of economics-based concepts on the

other end.

Example: Goodwill

Previous practice:

Goodwill is to be amortized over a 40 life until it is fully amortized.

New FASB rule:

Goodwill is not amortized.

Any recorded goodwill is to be tested for impairment and written

down to its current fair value on an annual basis.

FASB Questions

1.

Do you support the Board’s proposal for a principles-based approach to U. S. standard

setting?

Will that approach improve the quality and transparency of U. S. financial accounting and

reporting?

2.

Should the Board develop an overall reporting framework as in IAS 1?

If so, should that framework include a true and fair override?

3.

Under what circumstances should interpretive and implementation guidance be

provided under a principles-based approach to U.S. standard setting?

Should the Board be the primary standard setter responsible for providing that guidance?

4.

Will preparers, auditors, the SEC, investors, creditors, and other users of financial

information be able to adjust to a principles-based approach to U.S. standard setting?

If not, what needs to be done and by whom?

5.

6.

What other factors should the Board consider in assessing the extent to which it should

adopt a principles-based approach to U.S. standard setting?

What are the benefits and costs (including transition costs) of adopting a principlesbased approach to U.S. standard setting?

How might those benefits and costs be quantified?

Principles Based vs. Rules Based

Accounting Standards

The AAA’s position

Dissenting opinion

International Convergence

FASB & IASB pledged

Achieve compatibility

Maintain compatibility

FASB-IASB Financial Statement

Presentation Project

Establish common standard

Goals

Understand past and present financial position

Understand changes and causes of changes

Evaluate future cash flows

FASB-IASB Financial Statement

Presentation Project

3 Phases

A. What constitutes complete set of statements?

1.

2.

3.

4.

Financial position

Earnings and comprehensive income

Cash flows

Changes in equity

FASB-IASB Financial Statement

Presentation Project

3 Phases

B. Fundamental issues for presentation of

information

C. Presentation of interim financial information in

U.S. GAAP

Prepared by Kathryn Yarbrough, MBA

Copyright © 2009 John Wiley & Sons, Inc. All rights reserved.

Reproduction or translation of this work beyond that permitted in

Section 117 of the 1976 United States Copyright Act without the

express written consent of the copyright owner is unlawful. Request

for further information should be addressed to the Permissions

Department, John Wiley & Sons, Inc. The purchaser may make backup copies for his/her own use only and not for distribution or

resale. The Publisher assumes no responsibility for errors,

omissions, or damages, caused by the use of these programs or from

the use of the information contained herein.