Chapter 16: Consumption

advertisement

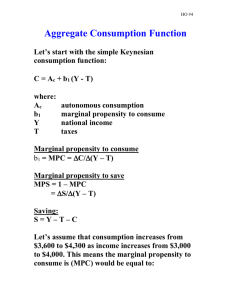

Chapter 16: Consumption John M. Keynes: Absolute Income Hypothesis Consumption is a linear function of disposable personal income, C = C + cY C = consumption expenditure Y = disposable income C = autonomous consumption (intercept of the line) c = marginal propensity to consume (slope of the line) Properties of Consumption Function Consumption is determined by current income Marginal propensity to consume (MPC = ΔC/ΔY) is between zero and one (0<c<1) Average propensity to consume (APC = C/Y) falls as income rises Short-run Consumption Function Consumption expenditure C = C + cY Constant APC c C Disposable income Empirical Evidence High income families have a higher marginal propensity to save (MPS = 1 – MPC) High income families have a higher average propensity to save (APS = 1 – APC); APC falls with the level of income In the long-run, autonomous consumption falls to zero (C = 0) Long-run Consumption Function Consumption expenditure C = ćY Variable APC; Ĉ=0 ć Ĉ Disposable income Irving Fisher: Intertemporal Choice Consumption decisions are based on current and future income Current period income = current income plus present value of future income: Y1 + Y2 / (1 + r), where r is a discount rate Future period income = future income plus future value of current income: Y2 + (1 + r)Y1 The Intertemporal Budget Line Future Period B C2 A Y2 C2 C C1 Y1 C1 Current Period The Intertemporal Budget Line Along BC, there is a trade-off between current and future consumption spending Along AB, C1<Y1, but C2>Y2: consumers would save in current period to finance consumption in second period Along AC, C1>Y1, but C2<Y2: consumers would borrow in current period and will pay off debt in future period Consumer Preferences Consumer preferences are shown by a family of indifference curves Any combination of current and future consumption along an indifference curve provides the same level of satisfaction for the consumer A higher indifference curve yields combinations with greater satisfaction Consumer Preferences Future Period Combination B is preferred to combination A because it yields more in both periods B A Current Period The Consumer’s Optimum Consumer equilibrium is achieved at the tangency of the highest attainable indifference curve and the budget line The tangency determines the optimum allocation of consumption spending in both periods; i.e. highest level of satisfaction within the budget The Consumer’s Optimum Future Period Higher income shifts the budget line up, positioning the consumer on a higher indifference curve and consumer’s optimum C2f C1f B A C1c C2c Current Period Franco Modigliani: Life Cycle Hypothesis Consumption depends on income and wealth C = Consumption expenditure W = Consumer wealth R = Length of productive life time T = Years of life Consumption Function C = (W + RY)/T = (1/T)W + (R/T)Y Define: α = 1/T is the MPC out of wealth β = R/T is the MPC out of income C = αW + βY Consumption Function C = αW + βY Consumption expenditure β 1 αW Disposable income For the United States, α = 0.02 and β = 0.60. Consumption Function Consumption expenditure αW2 αW1 Disposable income Increased wealth shifts the consumption function upward. Consumer Behavior over Life Time Consumption spending is a stable function of income Consumers save their leftover income Consumers accumulate wealth during the productive lifetime Consumer finance retirement by dissaving and selling-off their assets Consumer Behavior over Life Time $ Wealth Income Saving Consumption Dissaving R T Years Milton Friedman: Permanent Income Hypothesis Measured income consists of permanent and transitory income; Y = YP + YT Permanent income is the average income we make during years of productive life Transitory income is the random variation from the average Consumption Function Consumption is a function of permanent income C = αYP Consumers use saving and borrowing to smooth consumption in response to transitory changes in income Determinants of Consumption Combining all the theories, we can conclude that consumption depends on Current income Expected future income Wealth Interest rate