Chapter 20

advertisement

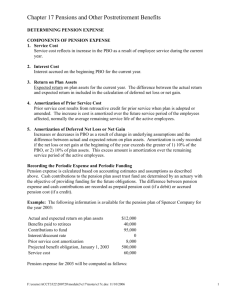

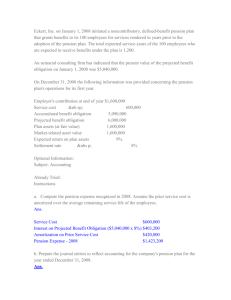

Chapter 20 Including FASB 158 Accounting for Postemployment Benefits Intermediate Accounting 10th edition Nikolai Bazley Jones An electronic presentation by Norman Sunderman Angelo State University COPYRIGHT © 2007 Thomson South-Western, a part of The Thomson Corporation. Thomson, the Star logo, and South-Western are trademarks used herein under license. 2 Objectives 1. Understand the characteristics of pension plans. 2. Explain the historical perspective of accounting for pension plans. 3. Explain the accounting principles for defined benefit plans, including computing pension expense and recognizing pension liabilities and assets. 4. Account for pensions. 5. Understand disclosures of pensions. 3 Objectives 6. Explain the conceptual issues regarding pensions. 7. Understand several additional issues related to pensions. 8. Explain other post-employment benefits. 9. Account for OPEBs. 10. Explain the conceptual issues regarding OPEBs. 11. Understand present value calculations for pensions. (Appendix) 4 Defined Contribution Plans The employer contributes a defined sum to a third party plan trust. Amounts to be funded are determined by the plan. The plan invests the contributed assets, which earn income, and makes distributions to retirees. There is no promise for specific future benefits. Market risk is borne by the employee. Accounting for the firm is relatively straightforward. For profit companies contribute to 401(k) plans and nonprofit organizations contribute to 403(b) plans. 5 Characteristics of a Pension Plan A pension plan requires that a company provide income to its retired employees in return for services they provided during their employment. 6 Defined Benefit Plans The retirement income, normally paid monthly, usually is determined on the basis of the employees earnings and length of service with the company. $50,000 average salary X 2.5% per year X 30 years = $37,500 pension per year Internal Revenue Qualifications Most companies design their pension plans to meet the Internal Revenue Code qualifications, which state that: 1. Employer contributions are deductible for income tax purposes when paid. 2. Pension fund earnings are exempt from income taxes. 3. Employer contributions to the pension fund are not taxable to the employees until they receive their pension benefits. 7 8 Pension Relationships 9 Defined Benefit Plans The employee is promised a certain amount of benefits at retirement. The amount received is based upon variables such as -Years of service -Ending salary or average of best (three) years -Multiplier, such as 2.5% per year of service -Age, if retiring early, a deduction will be made The employer remains liable for the benefits and bears the market risk. The employer is the trust-beneficiary. The accounting by the firm is complex. 10 Projected Benefit Obligation The projected benefit obligation is the actuary’s estimate of the present value of benefits attributed to date based on future salary levels. 11 Accumulated Benefit Obligation The accumulated benefit obligation is the actuary’s estimate of the present value of benefits attributed to date based on current salary levels. 12 Components of Pension Expense 1. 2. 3. 4. 5. +Service cost for the year. Increases pension expense. +Interest on projected benefit obligation (liability). Beginning PBO times the discount or settlement rate. Increases pension expense. -Expected return on plan assets during the year. Fair value of plan assets at beginning of year times expected long-term rate of return on plan assets. Generally decreases pension expense. +Amortization of prior service cost = Present value of additional benefits/modification of the plan amortized over the remaining service lives of active employees. Generally increases pension expense. +Gain or loss = Amortization of the cumulative net gain or loss from previous periods that has not yet been included in pension expense, in excess of the corridor. 13 Service Cost Service cost is the actuarial present value of the benefits attributed by the pension benefit formula to service rendered by the employees during the current period. 14 Interest Cost Interest cost is the increase in the projected benefit obligation due to the passage of time. 15 Expected Return on Assets The expected return on plan assets is the expected increase in plan assets due to investing activities. The expected return on plan assets, if positive, will decrease pension expense. 16 Expected Return on Plan Assets Projected Benefit Obligation Projected Benefit Obligations Grows to Equal Expected at Beginning of Period = Retirement Obligation Present Value of Benefits Earned to Date Retirement Interest = Projected Benefit x Discount Cost Obligation Rate Expected Return on Plan Assets During Period Plan assets at Beginning of Period at Fair Value Assets Used to Pay Retirement Benefits Assets Grow to Equal the Amounts Needed to Pay Retirement Benefits 17 Prior Service Cost When a defined benefit plan is either initiated or amended, credit is often given to employees for years of service provided before the date of initiation or amendment. 18 Prior Service Cost The retroactive benefit Prior service cost is reported to a pension plan is theas a liability and as a negative element of Other prior service cost. Comprehensive Income for the year at the date of the plan amendment. 19 Methods of Amortization Prior service cost may be amortized to pension expense over future service periods of employees active at the time of the plan amendment using either the straight-line or years-of-service method. 20 Straight-line Method The average remaining service life of employees expected to receive benefits is calculated by dividing the total future service years by the number of employees. Total future service years = average remaining service life Number of employees expected to receive benefits 21 Years-of-Service Method The Board prefers a years-of-service amortization method where prior service cost is divided by the number of future service years to be worked by participating employees, to obtain a cost per service-year. This cost per service-year is multiplied by the number of service years consumed each year. 22 Years-of-Service Method At the beginning of 2007, Watts Company had nine employees who are expected to receive pension benefits. One employee (A) is expected to retire after three years, one (B) after 4, two (C,D) after 5, two (E,F) after 6 and three (G,H,I) after 7 years. 23 Years-of-Service Method At that time, the company’s actuary computed the prior service cost at $400,000. 24 Straight-Line Amortization The seven employees will provide 50 years of service, so the average service provided will be 50 / 7 = 5.56 years. The prior service cost of $400,000 divided by 5.56 years equals $71,942 to be amortized to pension expense each year. 25 Gain or Loss A gain or loss from previous periods arises because the actual amount of the PBO is different from what was assumed and because of changes in actuarial assumptions. 26 Gain or Loss The gain or loss for the year is recorded as a liability or asset and in Other Comprehensive Income for the year. Accrued/Prepaid Pension Cost 15,300 Other Comprehensive Income (gain) 15,300 27 Gain or Loss The excess of the accumulated gain or loss over a “corridor” amount is amortized over the remaining service life of active employees expected to receive benefits under the plan. 28 Amortization of Gain or Loss The minimum amortization required is computed by dividing the total accumulated gain or loss subject to amortization at the beginning of the year by the average remaining service period of active employees expected to receive benefits. The amount subject to amortization is the excess of 10% of the greater of the beginning balances of the projected benefit obligation and the fair value of the assets value. Use absolute values. 29 Amortization of Gain or Loss 1. Amortization of any unrecognized net loss from previous periods is added to compute pension expense, or 2. Amortization of any unrecognized net gain from previous periods is deducted to compute pension expense. 30 Computation of Net Gain or Loss Use January 1 cumulative gain or loss for computation. Jan. 1 Cumulative Net Loss Year (Gain) Projected Benefit Obligation Actual Fair Value of Plan Assets 2007 $13,000 $110,000 2008 (2,300) 2009 2010 Corridor Excess Net Loss (Gain) Amortized Net Loss (Gain) $100,000 $11,000 $2,000 $200 135,000 130,000 13,500 ---- ---- 18,700 168,000 170,000 17,000 1,700 170 27,500 230,000 215,000 23,000 4,500 450 Assume the average remaining service period is 10 years. Divide By 10 years Component of pension expense 31 Net Gain or Loss December 31, 2007: Amortized $200 of January 1 accumulated net loss to pension expense. December 31, 2007: Accrued/Prepaid Pension Cost Other Comprehensive Income 200 200 (Amount amortized to pension expense during 2007) 32 Net Gain or Loss December 31, 2007: Accrued/Prepaid Pension Cost Other Comprehensive Income 15,300 15,300 (Difference between $13,000 loss on January 1 and $2,300 gain on December 31) December 31, 2008: Other Comprehensive Income Accrued/Prepaid Pension Cost 21,000 21,000 (Difference between $2,300 accumulated gain on January 1 and $18,700 accumulated loss on December 31) 33 Projected Benefit Obligation Beginning projected benefit obligation + Prior service cost added this year = Adjusted beginning projected benefit obligation + Service cost for the period + Interest cost on beginning PBO + Actuarial losses (or – Actuarial gains) - Payments to retirees = Ending projected benefit obligation 34 Plan Assets Beginning fair value of plan assets + Actual return on pension plan assets + Contributions by the company - Payment to retirees = Ending fair value of plan assets 35 Pension Expense Equal to Funding Facts for the Carlisle Company 1. The company adopts a pension plan on January 1, 2007. No retroactive benefits were granted to employees. 2. The service cost each year is: 2007, $400,000; 2008, $420,000; 2009, $432,000. 3. The projected benefit obligation at the beginning of each year is: 2008, $400,000; and 2009, $840,000. Continued 36 Pension Expense Equal to Funding 4. The discount rate is 10%. 5. The expected long-term rate of return on plan assets is 10%. 6. The company adopts a policy of funding an amount equal to the pension expense and makes a payment at the end of each year. 7. Plan assets are based on the amounts contributed each year, plus a return of 10%, less $20,000 to retired employees (beginning 2008). 37 Pension Expense Equal to Funding December 31, 2007: Pension Expense Cash 400,000 400,000 December 31, 2008: Pension Expense Cash Service cost (from actuary) Interest cost ($400,000 x 10%) Expected return on plan assets ($400,000 x 10%) Pension expense 420,000 420,000 $420,000 40,000 (40,000 ) $420,000 38 Balance-Plan Assets Plan Assets Cash from 2007 400,000 Return in 2008 40,000 Cash from 2008 420,000 Bal. 1/1/09 840,000 Paid to retirees 2008 20,000 39 Balance-PBO Projected Benefit Obligation 400,000 Service cost 2007 420,000 Service cost 2008 40,000 Interest on 1/1/08 PBO Benefits paid to retirees in 2008 20,000 840,000 Bal. 1/1/09 40 Pension Expense Equal to Funding December 31, 2009: Pension Expense Cash Service cost (from actuary) Interest cost ($840,000 x 10%) Expected return on plan assets ($840,000 x 10%) Pension expense 432,000 432,000 $432,000 84,000 (84,000 ) $432,000 Note that the interest cost and the return on the plan assets offset each other each year. 41 Funding Greater Than Pension Expense Carlisle Company funds $405,000 in 2007, $425,000 in 2008, and $435,000 in 2009. December 31, 2007: Pension Expense Accrued/Prepaid Pension Cost Cash 400,000 5,000 405,000 Asset 42 Funding Greater Than Pension Expense December 31, 2008: Pension Expense Accrued/Prepaid Pension Cost Cash 419,500 5,500 Service cost (from actuary) $420,000 Interest cost ($400,000 x 10%) 40,000 Expected return on plan assets ($405,000 x 10%) (40,500 ) Pension expense $419,500 Asset balance is now $5,000 + $5,500 425,000 43 Balance-Plan Assets Plan Assets Cash from 2007 405,000 Return 2008 40,500 Cash from 2008 425,000 Bal. 1/1/09 850,500 Paid to retirees 2008 20,000 44 Funding Greater Than Pension Expense December 31, 2009: Pension Expense Accrued/Prepaid Pension Cost Cash Service cost (from actuary) Interest cost ($840,000 x 10%) Expected return on plan assets ($850,500 x 10%) Pension expense 430,950 4,050 435,000 $432,000 84,000 (85,050 ) $430,950 The balance in the asset account is $14,550 ($5,000 + $5,500 + $4,050) Pension Expense Less Than Pension Funding & Expected Return Different from Both Actual Return & Discount Rate Carlisle Company funds $415,000 in 2007, $425,000 in 2008, and $440,000 in 2009. The expected return is 11% and the actual return is 12% each year. December 31, 2007: Pension Expense Prepaid/Accrued Pension Cost Cash 400,000 15,000 415,000 45 Pension Expense Less Than Pension Funding & Expected Return Different From Both Actual Return & Discount Rate December 31, 2008: Pension Expense Prepaid/Accrued Pension Cost Cash Service cost (assumed) Interest cost ($400,000 x 10%) Expected return on plan assets ($415,000 x 11%) Pension expense 414,350 10,650 425,000 $420,000 40,000 (45,650 ) $414,350 The balance in the asset account is $25,650 46 47 Balance-Plan Assets Plan Assets Cash from 2007 415,000 Return 2008 49,800 Cash from 2008 425,000 Bal. 1/1/09 869,800 Paid to retirees 2008 20,000 48 Balance-PBO Projected Benefit Obligation 400,000 Service cost 2007 420,000 Service cost 2008 40,000 Interest on 1/1/08 PBO Benefits paid to retirees in 2008 20,000 840,000 Bal. 1/1/09 Pension Expense Less Than Pension Funding and Expected Return Different From Both Actual Return &Discount Rate December 31, 2009: Pension Expense Prepaid/Accrued Pension Cost Cash Service cost Interest cost ($840,000 x 10%) Expected return on plan assets ($869,800 x 11%) Pension expense 420,322 19,678 440,000 $432,000 84,000 (95,678 ) $420,332 The balance in the asset account is $49,478 49 50 Difference Between Expected and Actual Return Because the 12% actual return is $49,800, which is $4,150 higher than the $45,650 expected return, a journal entry must be made to Accrued/ Prepaid Pension Cost and Other Comprehensive Income for the year. A gain increases income. Accrued/ Prepaid Pension Cost Other Comprehensive Income 4,150 4,150 51 Pension Expense Including Amortization of Prior Service Cost Carlisle Company awarded retroactive benefits to employees when it adopted the pension plan. The prior service costs were estimated to be $2 million, which is to be amortized over 20 years. Carlisle decided to increase its contributions to $705,000 in 2007, $715,000 in 2008, and $730,000 in 2009. 52 Pension Expense Including Amortization of Prior Service Cost As required by FAS 158, the prior service costs of $2 million must be recorded as a liability and also as a negative element of Other Comprehensive Income for the year. Other Comprehensive Income 2,000,000 Accrued/Prepaid Pension Cost 2,000,000 Pension Expense Including Amortization of Prior Service Cost December 31, 2007: Pension Expense Accrued/Prepaid Pension Cost Cash 700,000 5,000 Service cost $400,000 Interest cost ($2,000,000 x 10%) 200,000 Amortization of prior service cost ($2,000,000/ 20 years) 100,000 Pension expense $700,000 705,000 53 54 Pension Expense Including Amortization of Unrecognized Prior Service Cost The 2007 pension expense includes $100,000 amortization of prior service cost ($2,000,000/ 20 years). Therefore, the company must record an adjusting entry to increase 2007 Other Comprehensive Income. Accrued/Prepaid Pension Cost 100,000 Other Comprehensive Income 100,000 55 Balance-PBO Projected Benefit Obligation 400,000 Service cost 2007 2,000,000 Prior service cost 200,000 Interest on 1/1/07 PBO 2,600,000 Bal. 1/1/08 Pension Expense Including Amortization of Prior Service Cost December 31, 2008: Pension Expense Prepaid/Accrued Pension Cost Cash Service cost (assumed) Interest cost ($2,600,000 x 10%) Expected return on plan assets ($705,000 x 11%) Amortization of prior service cost Pension expense 702,450 12,550 $420,000 260,000 (77,550 ) 100,000 $702,450 715,000 56 57 Pension Expense Including Amortization of Prior Service Cost The 2008 pension expense also includes $100,000 amortization of prior service cost so the company must record an adjusting entry to increase 2008 Other Comprehensive Income. Accrued/Prepaid Pension Cost 100,000 Other Comprehensive Income 100,000 58 Balance-PBO Projected Benefit Obligation 400,000 Service cost 2007 Benefits paid 2,000,000 Prior service cost to retirees 200,000 Interest on 1/1/07 PBO in 2008 420,000 Service cost 2008 20,000 260,000 Interest on 1/1/07 PBO 3,260,000 Bal. 1/1/09 59 Balance-Plan Assets Plan Assets Cash from 2007 705,000 Return in 2008 84,600 Cash from 2008 715,000 Bal. 1/1/09 1,484,600 Paid to retirees 2008 20,000 Pension Expense Including Amortization of Prior Service Cost December 31, 2009: Pension Expense Accrued/Prepaid Pension Cost Cash Service cost Interest cost ($3,260,000 x 10%) Expected return on plan assets ($1,484,600 x 11%) Amortization of prior service cost Pension expense 694.694 35,306 730,000 $432,000 326,000 (163,306 ) 100,000 $694,694 60 61 Disclosures According to FASB Statement No. 132R and 158, a company must disclose specific information about a defined benefit pension plan, including the following: 62 Disclosures 1. A reconciliation of the beginning and ending balances of the projected benefit obligation. 3. The components and amount of pension expense. 2. A reconciliation of the beginning and ending balances of the fair value of the plan assets. 4. The discount rate, the rate and the expected long-term rate of return on the plan assets. 63 Required Funding A company must fund its pension plan each year at an amount that at least equals the service cost for the year plus the amount needed to amortize any underfunding over a maximum of seven years. 64 Summary of Journal Entries 1. Pension expense. Entries to Accrued/Prepaid Pension Cost and Other Comprehensive Income 2. Record prior service cost. 3. Record difference between expected return and actual return. 4. Record amortization of prior service cost. 5. Record amortization of cumulative gain or loss. 6. Record changes in PBO (not illustrated in text). ---------------------------------------------------7. Close Other Comprehensive Income to Accumulated Other Comprehensive Income 65 Termination Benefits Paid to Employees FASB Statement No. 88 requires that a company record a loss and a liability for termination benefits when the following two conditions are met: 1. The employee accepts the offer, and 2. The amount can be reasonably estimated. 66 Other Postemployment Benefits Many companies offer additional benefits to former employees after their retirement--widely referred to as OPEB. What are the major differences between postretirement healthcare benefits and pensions? 67 Other Postemployment Benefits Item Pensions Beneficiary Retired employee (some residual benefit to surviving spouse) Benefits Defined, fixed dollar amount, paid monthly Funding Healthcare Retired employee, spouse, and dependents Not limited, paid as used, varies geographically Funding legally required Usually not funded and tax deductible because not legally required and not tax deductible 68 OPEB Benefits The net postretirement benefit expense includes the following components: 1. 2. 3. 4. 5. Service cost Interest cost Expected return on plan assets Amortization of prior service cost Amortization of net gain or loss 69 Illustration of Accounting for OPEB Livingston Company adopts a healthcare plan for retired employees on January 1, 2007. At that time the company has two employees and one retired employee. The discount rate is 10%, all employees were hired at age 25 and will become eligible for full benefits at age 55. The retired employee was paid $1,500 postretirement healthcare benefits in 2007. The company determines its accumulated postretirement benefit obligations to be $100,000. Continued 70 Illustration of Accounting for OPEB Service cost (actuarially determined) Interest cost ($100,000 x 0.10) Expected return on plan assets Amortization of prior service cost ($100,000 ÷ 5) Gain or loss Postretirement Benefit Expense Continued $ 1,100 10,000 0 20,000 0 $31,100 71 Illustration of Accounting for OPEB January 1, 2007 Other Comprehensive Income 100,000 Accrued Postretirement Benefit Cost 100,000 December 31, 2007 Postretirement Benefit Expense Accrued Postretirement Benefit Cost 31,100 31,100 72 Illustration of Accounting for OPEB To record the payment of retirement benefits Accrued Postretirement Benefit Cost Cash 1,500 1,500 To record amortization of prior service cost Accrued Postretirement Benefit Cost 20,000 Other Comprehensive Income 20,000 73 Chapter 20 Task Force Image Gallery clip art included in this electronic presentation is used with the permission of NVTech Inc.