Slide 1

advertisement

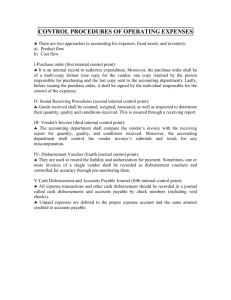

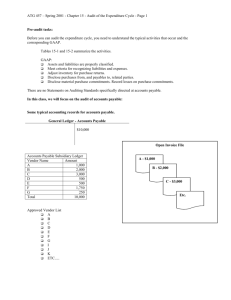

Modern Auditing: Assurance Services and the Integrity of Financial Reporting, 8th Edition William C. Boynton California Polytechnic State University at San Luis Obispo Raymond N. Johnson Portland State University Chapter 15 – Auditing the Expenditure Cycle Chapter Overview The Expenditure Cycle Develop Audit Objectives Understanding the Entity and Environment Inherent Risk, Including the Risk of Fraud • Management Misstatement of Expenditures – Understate expenses – Understate payables • Other Misstatement Factors – – – – High volume of transactions Unauthorized purchases Misappropriation Duplication of payments Analytical Procedures Consideration of Internal Control Components • Control Environment • Risk Assessment • Information and Communication • Monitoring Study Break 1. The expenditure cycle consists of all of the following activities, except: A. B. C. D. Purchase transactions Cash disbursement transactions Sales transactions Purchase adjustments C. Sales transactions Study Break 2. This analytical procedure calculates the average number of days it takes to retire accounts payables. A. B. C. D. Current ratio Quick ratio Cost of Goods Sold to Accounts Payable Accounts Payable Turn Days D. Accounts Payable Turn Days Purchase Transactions – Documents and Records • Purchase requisition • Purchase order • Approved vendor master file • Open purchase order file • Receiving report • Receiving file • Vendor Invoice Purchase Transactions – Common Documents and Records • Voucher • Exception reports • Voucher summary • Voucher register • Purchase transactions file • Accounts payable master file • Suspense files Purchase Transactions – Functions and Control Activities • Initiating Purchases – Placing vendors on an authorized vendor list – Requisitioning goods and services – Preparing purchase orders • Receipt of Goods and Services – Receiving the goods – Storing goods received for inventory – Returning goods to vendor • Recording Liabilities Systems Flowchart – Purchase Transaction Systems Flowchart – Purchase Transaction Systems Flowchart – Purchase Transaction Study Break 3. This item is a written offer from the purchasing department to a vendor or supplier to purchase goods or services specified in the order. A. B. C. D. Purchase requisition Purchase order Receiving report Receiving file B. Purchase order Study Break 4. This function of processing of purchase transaction includes placing vendors on an authorized vendor list and preparing purchase orders. A. B. C. D. Initiating purchases Receipt of goods and services Recording liabilities Paying liabilities A. Initiating purchases Cash Disbursement Transactions– Common Documents and Records • Check • Check Summary • Cash Disbursements Transaction File • Cash Disbursements Journal or Check Register Cash Disbursement TransactionsFunction and Control Activities • Computerized System – Paying the Liability – Recording the Disbursement • Manual System – Paying the Liability – Recording the Disbursement Systems Flowchart – Cash Disbursement Transactions Study Break 5. This record is a report of total checks issued in a batch or during a day. A. B. C. D. Check Check summary Cash disbursements transaction file Check register B. Check summary Purchase Adjustment Transactions– Common Documents and Records • Purchase Return Authorization • Shipping Report • Debit Memo Purchase Adjustment Function and Controls • Purchase Returns and Allowances • Other Controls • Tests of Controls Substantive Tests of Accounts Payable Balances • Determining Detection Risk for Tests of Details – Existence and Occurrence – Completeness – Rights and Obligations – Valuation and Allocation – Presentation and Disclosure Designing Substantive Tests • Initial Procedures • Analytical Procedures Designing Substantive Tests • Tests of Details of Transactions – Vouch Recorded Payables to Supporting Documentation – Perform Cutoff Tests • Purchases cutoff tests • Cash disbursement cutoff tests • Purchase return cutoff tests – Perform Search for Unrecorded Payables • Subsequent payments Designing Substantive Tests • Tests of Details of Balances – Accounts Payable Confirmations – Reconcile Unconfirmed Payables to Vendor Statements • Tests of Details of Disclosures Study Break 6. This is a report prepared on the shipment of goods to vendors showing the kinds and quantities of goods shipped. A. B. C. D. Purchase Return Authorization Shipping Report Debit Memo Check Summary B. Shipping Report Study Break 7. These items include all checks issued or vouchers paid after the balance sheet date. A. B. C. D. Purchase return cutoff tests Check summary Subsequent payments Confirmation of accounts payable C. Subsequent payments