p210203

advertisement

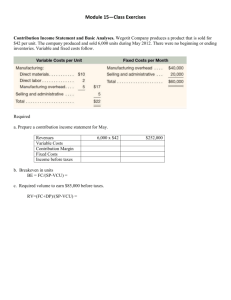

Cost-Volume-Profit Analysis Chapter 3 Accounting Principles II AC 2102 - Fall Semester, 1999 Chapter 15 - 1 Overview of CVP Analysis • Is a powerful tool for planning & decision making • Focuses on the interrelationships between costs, quantity sold, and price • Can quickly show the economic impact of different operational/financial circumstances and decisions • Can be a valuable tool to identify economic problems & assist in pinpointing the necessary solution Chapter 15 - 2 Some of the Key Issues CVP Analysis Addresses • The number of units or dollars of revenue required to break-even • The impact of a given reduction in fixed costs on the break-even point and overall profitability • The impact of an increase in price on profitability • The sensitivity of profits to changes in Chapter 15 - 3 prices, costs or volume levels Break-Even Point In Units • The break-even point is where total revenues equals total cost – The point of zero profit • In terms of units, the break-even point is the number of units sold which will result in a zero profit level • Several work steps are required to perform a break-even analysis Chapter 15 - 4 Work Steps Required To Perform a Cost-Volume-Profit Analysis • 1st Step: Define a “unit” • 2nd Step: Separate costs into fixed and variable components – Note: this second step requires the separating of mixed costs into their fixed and variable components • 3rd Step: Apply the appropriate mathematical analysis and equations Chapter 15 - 5 Some Possible Definitions of a “Unit” (i.e., units “produced” and sold) • Automobile Company: Cars • Hospital: Patient-Days • Hotel: (1) Guest-Days (2) Number of Occupied Rooms (3) % of Rooms Occupied • Soft-drink Company: Cans of 12-ounce equivalents • Pharmacy: Cannot be defined in “units” Chapter 15 - 6 Separating Costs Into Their Fixed & Variable Components • In most problems presented in text books this step has already been performed – i.e., in most C-V-P problems, the costs that are fixed and variable are already defined • It should be clearly understood that in practice this is the most difficult step in a C-V-P analysis • In the accounting records costs are only defined by nature of the expense (salaries, insurance, etc.) – i.e., the cost behavior pattern of each cost is not identified in the accounting records Chapter 15 - 7 Contribution Margin • Contribution margin is an extremely useful and insightful concept • Two Definitions: Price - Variable Costs per Unit = CM per unit or Total Revenue - Total Variable Costs = Total Contribution Margin • Note: It is not the same as Gross Margin – Gross Margin = Revenues - Cost of Goods Sold Chapter 15 - 8 Two Ways of Calculating The Contribution Margin Per Unit Basis: = Contribution Per Unit/Price Per Unit Contribution Margin Ratio: = Total Contribution Margin/Total Revenues Chapter 15 - 9 Mathematical Analysis When Dealing With Unit Data • Breakeven Point: = Total Fixed Costs/Contrib. Margin Per Unit • Sales Required to Achieve Targeted Profit Level (Before Taxes): = (FC+Targ. PBT) /Contrib. Margin Per Unit Chapter 15 - 10 Mathematical Analysis When Dealing With Total Sales Dollars • Breakeven Point: = Total Fixed Costs/Contrib. Margin Ratio • Sales Required to Achieve Targeted Profit Level (Before Taxes): = (FC+Targ. PBT) /Contrib. Margin Ratio Chapter 15 - 11 Other Key Concepts • Margin of Safety: = Actual Sales - Breakeven Sales - can be expressed in units or sales dollars • Operating Leverage: = The ratio of a firm’s fixed costs to its variable costs • Degree of Operating Leverage: = Contribution Margin/Operating Income Chapter 15 - 12