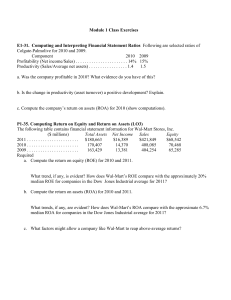

Intro & Ratios

advertisement

Introduction to Finance What is Finance? Finance is the study of how people and businesses evaluate investments and raise capital to fund them. Corporate Finance addresses the following three questions: What long-term investments should the firm choose? 2. How should the firm raise funds for the selected investments? 3. How should short-term assets be managed and financed? 1. 3 Forms of Business Organization The Sole Proprietorship The Partnership The Corporation 4 Sole Proprietorship It is a business owned by a single individual who is entitled to all of the firm’s profits and is responsible for all of the firm’s debt. The sole proprietors typically raise money by investing their own funds and by borrowing from a bank. Sole Proprietorship (cont.) Advantages: Easy to start No need to consult others while making decisions Organization taxed at the personal tax rate Disadvantages: Owner is personally liable for the business’s debt The business ceases on the death of the proprietor Hard to raise money Partnership: General A general partnership is an association of two or more persons who come together as coowners for the purpose of operating a business for profit. Partnership (cont.) Advantages: Relatively easy to start Organization taxed at the personal tax rate Access to funds from multiple sources or partners Disadvantages: Partners jointly share unlimited liability It is not always easy to transfer ownership Partnership: Limited In limited partnerships, there are two classes of partners: general and limited. The General Partner runs the business and faces unlimited liability for the firm’s debts The Limited Partner does not run the business and is only liable up to the amount invested. Corporation Are the big organizations. Generally established when very large sums of money are required. Main defining characteristic is the separately of ownership (shareholders) from control (management) The Board of directors are elected by the shareholder, and the board appoints the senior management of the firm. Corporation (cont.) Advantages Liability of owners is limited to invested funds Life of corporation is not tied to the owner Easier to transfer ownership Easier to raise Capital Disadvantages Greater regulation Double taxation of dividends Limited Liability Company (LLC) Limited liability company (LLC) combines the tax benefits of a partnership (no double taxation of earnings) with the limited liability benefit of corporation (the owner’s liability is limited to what they invest). Comparison Five Basic Principles of Finance 1. 2. 3. 4. 5. Time Value of Money Risk-Return Trade-off Cash is King Market Prices Reflect Expectations/News People do what is best for them, unless you make them change their mind 14 Time Value of Money A dollar today is worth more than a dollar tomorrow We can invest the dollar today and earn interest. Therefore, in the future we have the dollar invested plus interest Risk-Return Trade-off No one likes risk for its own sake. Therefore people will only take on more risk if they are compensated with higher returns Higher the risk higher expected return Note expected return may not be equal to the realized return. Cash is King Profit, Earnings, Net Income are accounting numbers designed to measure performance. These numbers can be manipulated Cash flows are the actual dollars flowing in and out of the company and can’t be manipulated as easy It is possible for a firm to report profits but have no cash. Cash is King: Follow on Financial decisions should only consider “incremental cash flow” i.e. the difference between the cash flows the company will produce with the new investment and what it would make without the investment. Market Prices Reflect News Investors react quickly to news/information and decisions made by managers. Good News ==> Higher stock prices Bad News ==> Lower stock price. The Goal of Financial Managers What is the correct goal? Maximize profit? Minimize costs? Maximize market share? Maximize shareholder wealth? 20 The Financial Manager The Financial Managers increase shareholder wealth by: 1. Selecting value creating projects 2. Capital Budgeting Decision Making smart financing decisions Capital Structure Decision 21 Financial Markets Firms Stocks and Bonds Money Investors securities Bob Sue money Primary Market Secondary Market 22 Quick Quiz 1. 2. 3. 4. What are the three basic questions Financial Managers must answer? What are the three major forms of business organization? What is the goal of financial management? What is the difference between a primary market and a secondary market? 23 Financial Statements and Cash Flow Financial Statements Company managers, investors, and outside analysts use financial statements to conduct… Cash flow analysis Performance (ratio) analysis The SEC requires U.S. companies to produce financial statements conforming to Generally Accepted Accounting Principles (GAAP), developed by the Financial Accounting Standards Board (FASB). 25 Basic Financial Statements The accounting and financial regulatory authorities mandate the following four types of financial statements: Balance Sheet 2. Income Statement 3. Cash Flow Statement 4. Statement of Shareholder’s Equity 1. The Balance Sheet A snapshot of the firm’s accounting value at a specific point in time What does the company look like today The Balance Sheet Identity is: Assets ≡ Liabilities + Stockholder’s Equity Left Hand Side of the balance sheet must equal the Right Hand Side 27 Balance Sheet Total Value of Assets: Current Assets Total Firm Value to Investors: Current Liabilities Long-Term Debt Fixed Assets 1 Tangible 2 Intangible Shareholders’ Equity 28 U.S. Composite Corporation Balance Sheet 2007 Current assets: Cash and equivalents Accounts receivable Inventories Other Total current assets $140 294 269 58 $761 2006 $107 270 280 50 $707 Fixed assets: Property, plant, and equipment $1,423 $1,274 Less accumulated depreciation (550) (460) Net property, plant, and equipment 873 814 Intangible assets and other 245 221 Total fixed assets $1,118 $1,035 Total assets $1,879 The assets are listed in order by the length of time it would normally take a firm with ongoing operations to convert them into cash. Cash is the most liquid with intangible assets being the least liquid. $1,742 29 Balance Sheet Analysis When analyzing a balance sheet, the Finance Manager should be aware of three concerns: 1. 2. 3. Liquidity Debt versus Equity Value versus Cost 30 Liquidity Refers to the ease and quickness with which assets can be converted to cash—without a significant loss in value Generally the more liquid the asset the lower the rate of return Current assets are more liquid than fixed assets The more liquid a firm’s assets, the less likely the firm is to experience problems meeting short-term cash obligations (Ex. payroll) A profitable but illiquid firm will experience financial distress 31 Debt versus Equity Debt → Liability Promise Equity is the residual Assets to payout cash, an IOU – Liabilities ≡ Equity Debt represents a senior claim on firm assets If the firm goes bankrupt debt holders get paid before equity holders 32 Value versus Cost Accountants are historians, they care about what something cost when purchase Under GAAP, financial statements carry assets at cost Market value is the price at which assets, liabilities, and equity could actually be bought or sold, TODAY Cost and Market Value are two completely different concepts What for did we pay for it, versus what can we sell it 33 The Income Statement Measures financial performance over a specific period of time How has the company performed? The accounting definition of income is: Revenue – Expenses ≡ Income Generally the Income Statement is comprised of several parts: 34 U.S.C.C. Income Statement The operations section of the income statement reports the firm’s revenues and expenses from principal operations. Total operating revenues Cost of goods sold Selling, general, and administrative expenses Depreciation Operating income Other income Earnings before interest and taxes Interest expense Pretax income Taxes Current: $71 Deferred: $13 Net income $2,262 1,655 327 90 $190 29 $219 49 $170 84 $86 35 U.S.C.C. Income Statement The non-operating section of the income statement includes all financing costs, such as interest expense. Total operating revenues Cost of goods sold Selling, general, and administrative expenses Depreciation Operating income Other income Earnings before interest and taxes Interest expense Pretax income Taxes Current: $71 Deferred: $13 Net income $2,262 1,655 327 90 $190 29 $219 49 $170 84 $86 36 U.S.C.C. Income Statement Usually a separate section reports the amount of taxes levied on income. Total operating revenues Cost of goods sold Selling, general, and administrative expenses Depreciation Operating income Other income Earnings before interest and taxes Interest expense Pretax income Taxes Current: $71 Deferred: $13 Net income $2,262 1,655 327 90 $190 29 $219 49 $170 84 $86 37 U.S.C.C. Income Statement Net income is the “bottom line.” Total operating revenues Cost of goods sold Selling, general, and administrative expenses Depreciation Operating income Other income Earnings before interest and taxes Interest expense Pretax income Taxes Current: $71 Deferred: $13 Net income $2,262 1,655 327 90 $190 29 $219 49 $170 84 $86 38 Income Statement Analysis There are three things to keep in mind when analyzing an income statement: Generally Accepted Accounting Principles (GAAP) 2. Non-Cash Items 3. Time and Costs 1. 39 GAAP • • The matching principal of GAAP dictates that revenues be matched with expenses. Thus, income is reported when it is earned, even though no cash flow may have occurred. 40 Non-Cash Items • • • • The income statements also makes allowances for expense where no money changes hands Depreciation is the most apparent example. No firm ever writes a check for “depreciation.” Another non-cash item is deferred taxes, which does not represent a cash flow. Thus, net income is not cash. 41 Time and Costs • • • In the short-run, certain equipment, resources, and commitments of the firm are fixed, but the firm can vary such inputs as labor and raw materials. In the long-run, all inputs of production (and hence costs) are variable. Financial accountants do not distinguish between variable costs and fixed costs. Instead, accounting costs usually fit into a classification that distinguishes product costs from period costs. 42 Taxes “In this world nothing is certain but death and taxes.” Ben Franklin Taxes represent a major cost to the firm Taxes rules change, and are subject to political, not economic forces What this means is that taxes do not need to make economic sense Company is subject to two different tax rates Marginal – the percentage paid on the next Average – the tax bill / taxable income dollar earned 43 Marginal versus Average Rates Suppose your firm earns $4 million in taxable income. What is the firm’s tax liability? .15(50,000) + .25(75,000 – 50,000) + .34(100,000 – 75,000) + .39(335,000 – 100,000) + .34(4,000,000 – 335,000) = $1,356,100 Rate from table 2.3 What is the average tax rate? What is the marginal tax rate? If you are considering a project that will increase the firm’s taxable income by $1 million, what tax rate should you use in your analysis? 44 Net Working Capital • Net Working Capital (NWC)≡ Current Assets – Current Liabilities • NWC is usually positive for a growing firm • Why? 45 U.S.C.C. Balance Sheet $252m = $707- $455 2007 Current assets: Cash and equivalents Accounts receivable Inventories Other Total current assets $140 294 269 58 $761 2006 $107 270 280 50 $707 Fixed assets: Property, plant, and equipment $1,423 $1,274 Less accumulated depreciation (550) (460 Net property, plant, and equipment 873 814 Intangible assets and other 245 221 Total fixed assets $1,118 $1,035 $275m = $761m- $486m 2007 Current Liabilities: Accounts payable Notes payable Accrued expenses Total current liabilities $1,879 $1,742 $197 53 205 $455 Long-term liabilities: Deferred taxes Long-term debt Total long-term liabilities Here we see NWC grow $117 to $104 471 458 $275 million in 2006 from $588 $562 $252 million in 2005. Stockholder's equity: Preferred stock $39 $39 $23 million Common stock ($1 par value) 55 32 Capital surplus 347 327 This increase of $23 million is Accumulated retained earnings 390 347 Lessinvestment treasury stock (26) (20) an of the firm. Total equity Total assets $213 50 223 $486 2006 $805 $725 Total liabilities and stockholder's equity $1,879 $1,742 46 Financial Cash Flow As finance people what we are really interested in is the firm’s actual cash flow Since there is no magic in finance, it must be the case that the cash flow received from the firm’s assets must equal the cash flows to the firm’s creditors and stockholders. CF(A)≡ CF(B) + CF(S) 47 U.S.C.C. Financial Cash Flow Cash Flow from Assets Cash Flow of the Firm Operating cash flow (Earnings before interest and taxes plus depreciation minus taxes) Capital spending (Acquisitions of fixed assets minus sales of fixed assets) Additions to net working capital Total Cash Flow to Investors $238 -173 -23 $42 Cash Flow of Investors in the Firm Debt (Interest plus retirement of debt minus long-term debt financing) Equity (Dividends plus repurchase of equity minus new equity financing) Total $36 6 $42 48 The Cash Flow Statement The Cash Flow Statement is used by firms to explain changes in their cash balances over a period of time by identifying all of the sources and uses of cash for the period spanned by the statement. The Statement of Cash Flows The three components are: Cash flow from operating activities Cash flow from investing activities Cash flow from financing activities 50 U.S.C.C. Cash Flow from Operations Idea: Translate Net Income into cash To calculate cash flow from operations, start with net income, then add back noncash items like depreciation and adjust for changes in current assets and liabilities (other than cash). Operations Net Income Depreciation Deferred Taxes Changes in Assets and Liabilities Accounts Receivable Inventories Accounts Payable Accrued Expenses Notes Payable Other Total Cash Flow from Operations $86 90 13 -24 11 16 18 -3 -8 $199 51 U.S.C.C. Cash Flow from Investing Cash flow from investing activities involves changes in capital assets: acquisition of fixed assets and sales of fixed assets (i.e., net capital expenditures). The cash from sales of our buildings/machinery minus the cost of buildings/machinery we bought Acquisition of fixed assets Sales of fixed assets Total Cash Flow from Investing Activities -$198 25 -$173 52 U.S.C.C. Cash Flow from Financing Cash flows to and from creditors and owners include changes in equity and debt. Retirement of debt (includes notes) Proceeds from long-term debt sales Dividends Repurchase of stock Proceeds from new stock issue Total Cash Flow from Financing -$73 86 -43 -6 43 $7 53 U.S.C.C. Statement of Cash Flows The statement of cash flows is the addition of cash flows from operations, investing, and financing. Operations Net Income Depreciation Deferred Taxes Changes in Assets and Liabilities Accounts Receivable Inventories Accounts Payable Accrued Expenses Notes Payable Other Total Cash Flow from Operations Investing Activities Acquisition of fixed assets Sales of fixed assets Total Cash Flow from Investing Activities Financing Activities Retirement of debt (includes notes) Proceeds from long-term debt sales Dividends Repurchase of stock Proceeds from new stock issue Total Cash Flow from Financing Change in Cash (on the balance sheet) $86 90 13 -24 11 16 18 -3 -8 $199 -$198 25 -$173 -$73 86 -43 -6 43 $7 $33 54 Quick Quiz 1. 2. 3. 4. What is the difference between book value and market value? Which should we use for decision making purposes? What is the difference between accounting income and cash flow? Which do we need to use when making decisions? What is the difference between average and marginal tax rates? Which should we use when making financial decisions? How do we determine a firm’s cash flows? What are the equations, and where do we find the information? 55 Financial Statements Analysis and LongTerm Planning Financial Statements Analysis Common-Size Balance Sheets Compute Common-Size Income Statements Compute all accounts as a percent of total assets all line items as a percent of sales Standardized statements make it easier to compare financial information, particularly as the company grows. They are also useful for comparing companies of different sizes, particularly within the same industry. 57 Ratio Analysis Ratios allow for a better comparison through time and/or between companies Give a sense for how the firm is doing As we look at each ratio, ask yourself: How is the ratio computed? What is the ratio trying to measure and why? What is the unit of measurement? What does the value indicate? How can we improve the company’s ratio? 58 Categories of Financial Ratios Short-term solvency, or liquidity ratios Long-term solvency, or financial leverage ratios Asset management, or turnover ratios Profitability ratios Market value ratios 59 Liquidity Ratios These measure the ability of the firm to meet it’s short term obligations Why Current Ratio = CA / CL 708 / 540 = 1.31 times Quick Ratio (Acid Test) =(CA – Inventory) / CL (708 - 422) / 540 = 0.53 times Cash Ratio = Cash / CL 98 is this important? / 540 = 0.18 times Where do the “raw” numbers come from? 60 Leverage Ratios These measure the ability of the firm to meet it’s long term obligations Why is this important? Total Debt Ratio = (TA – TE) / TA (3588 Debt/Equity = TD / TE (3588 – 2591) / 2591 = 38.5% Equity Multiplier = TA / TE = 1 + D/E 1 - 2591) / 3588 = 28% + .385 = 1.385 Where do the “raw” numbers come from? 61 Coverage Ratios These measure the ability of the firm to pay it’s debt holders Why Times Interest Earned = EBIT / Interest 691 / 141 = 4.9 times Cash Coverage = (EBIT + Depreciation) / Interest (691 do we care about paying the debt holders? + 276) / 141 = 6.9 times Where do the “raw” numbers come from? 62 Inventory Ratios These tell else how efficiently the firm manages it’s inventory Why do we care about this? Do we want these ratios to be high or low? Where do the “raw” numbers come from? Inventory Turnover = Cost of Goods Sold / Inventory 1344 / 422 = 3.2 times Days’ Sales in Inventory = 365 / Inventory Turnover 365 / 3.2 = 114 days 63 Receivables Ratios These tell else how quickly the firm is paid? Why do we care about this? Do we want these ratios to be high or low? Where do the “raw” numbers come from? Receivables Turnover = Sales / Accounts Receivable 2311 / 188 = 12.3 times Days’ Sales in Receivables = 365 / Receivables Turnover 365 / 12.3 = 30 days 64 Total Asset Turnover This tells us how efficiently the firm is turning assets into sales Why do we care about this? Total Asset Turnover = Sales / Total Assets 2311 / 3588 = 0.64 times It is not unusual for TAT < 1, especially if a firm has a large amount of fixed assets. 65 Profitability Measures These measure how efficiently the firm operates Why do we care about these? Where do the raw numbers come from? Profit Margin = Net Income / Sales 363 Return on Assets (ROA) = Net Income / Total Assets 363 / 2311 = 15.7% / 3588 = 10.1% Return on Equity (ROE) = Net Income / Total Equity 363 / 2591 = 14.0% 66 Market Value Measures These tell us how the market (people) feel about the firm Where do these raw numbers come from? Market Price = $88 per share Shares outstanding = 33 million PE Ratio = Price per share / Earnings per share 88 / 11 = 8 times Market-to-book ratio = market value per share / book value per share 88 / (2591 / 33) = 1.12 times 67 The Du Pont Identity Created by Du Pont in 1920 Breaking ROE (NI/TE)into three parts, so we can understand where our return comes from ROE = PM * TAT * EM Calculation ROE = (NI / TE) (TA / TA) ROE = (NI / TA) (TA / TE) = ROA * EM ROE = (NI / TA) (TA / TE) (Sales / Sales) ROE = (NI / Sales) (Sales / TA) (TA / TE) 68 What does it mean? ROE = PM * TAT * EM Profit margin is a measure of the firm’s operating efficiency – how well it controls costs. Total asset turnover is a measure of the firm’s asset use efficiency – how well it manages its assets. Equity multiplier is a measure of the firm’s financial leverage. 69 Using Financial Statements Ratios are not very helpful by themselves: they need to be compared to something Time-Trend Analysis Used to see how the firm’s performance is changing through time Peer Group Analysis Compare to similar companies or within industries SIC and NAICS codes 70 Potential Problems to Remember when Analyzing Financial Statement There is no underlying theory, so there is no definitive way to know which ratios are most relevant Benchmarking is difficult Especially for diversified firms Firms use varying accounting procedures Ex. LIFO versus FIFO Globalization means different accounting regulations Firms have different fiscal years Extraordinary, or one-time, events 71 Financing Growth When growth is slow, the firm may be able to rely on internal financing Just using what they make At higher growth rates, the firm will likely need to go to the capital market for additional financing 72 The Internal Growth Rate The internal growth using the funds it generates The Internal Growth Rate can be calculated with ROA and Plowback Plowback ratio: how much of net income is being reinvested in the company IGR b = Addition to Retained Earnings / Net Income = (ROA * b)/(1-ROA * b) 73 IGR Calculation If a firm has an ROA of 0.132, and a plowback ratio of 0.667, what is its IGR? IGR = (ROA * b )/ (1 – ROA * b) 74 The Sustainable Growth Rate The sustainable growth rate tells us how fast the firm can grow by using internally generated funds and issuing debt, without changing the firm’s capital structure Do you expect this be higher or lower than the internal growth rate? The Sustainable Growth Rate is calculated with ROE and Plowback Just like IGR but use ROE instead of ROA 75 SGR Calculation If the same firm has an ROE of 0.264, what is its SGR? Remember plowback is 0.667 (ROE * b )/ (1 – ROE * b) 76 Quick Quiz 1. 2. 3. 4. 5. How do you standardize balance sheets and income statements? Why is standardization useful? What are the major categories of financial ratios? How do you compute the ratios within each category? What are some of the problems associated with financial statement analysis? 77 Quick Quiz 6. 7. 8. 9. 10. 11. What is the purpose of long-range planning? What are the major decision areas involved in developing a plan? What is the percentage of sales approach? What is the internal growth rate? What is the sustainable growth rate? What are the major determinants of growth? 78