1111534861_341182

advertisement

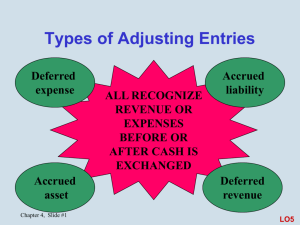

Recognition and Measurement Recognition: formally recording an item in the financial statements of an entity ...but at current value or historical cost? I know I need to record this... Measurement: quantification of the economic effects of the item on the entity LO1 Cash vs. Accrual Basis Cash basis: revenues and expenses are recorded only when cash is received or paid Accrual basis: revenues are recognized when earned; expenses are recognized when incurred LO2 Cash basis statement Accrual basis statement Statement of Cash Flows Income Statement Cash flows from operating activities: Net income: $ 7,000 $(4,000) What accounts for the difference? Revenue Recognition Principle Revenue is recognized when realized and earned—usually at time of sale Exceptions: Long-term contracts Franchises Commodities Installment sales Rent and interest LO3 Matching Principle Match expenses with associated revenues Directly e.g., Inventory Indirectly over period they provide benefits e.g., Buildings Simultaneously upon their acquisition e.g., Utilities LO4 Expense Recognition Income Statement Balance Sheet EXPENSES: ASSETS: Inventory Supplies Prepaid assets PP&E Intangibles when sold Cost of goods sold as used Supplies expense Insurance expense Rent expense over period they provide benefits l Depreciation expense Amortization expense Other expenses (as incurred) Types of Adjusting Entries Deferred expense Accrued asset RECOGNIZE REVENUE OR EXPENSES BEFORE OR AFTER CASH IS EXCHANGED Accrued liability Deferred revenue LO5 Deferred Expense Cash paid before expense is incurred Examples: • • • • Prepaid rent Prepaid insurance Office supplies Property and equipment Costs are initially recorded as assets and allocated to expenses in future periods Deferred Expense Example Prepay rent on office space for one year on September 1 Initial journal entry: 9/1 Prepaid Insurance 2,400 Cash 2,400 Monthly adjusting journal entry: 9/30 Insurance Expense 200 Prepaid Insurance 200 ($2,400 annual × 1/12 = $200 per month for 12 months) Deferred Revenue Cash received before revenue is earned Examples: • Insurance collected in advance • Subscriptions collected in advance • Gift certificates Receipts are initially recorded as liabilities (unearned or refundable receipts) and recorded as revenues in future periods when earned Deferred Revenue Example Received $2,400 for an insurance policy in advance on September 1 Initial journal entry: 9/1 Cash 2,400 Insurance Collected in Advance 2,400 Monthly adjusting journal entry: 9/30 Insurance Collected in Advance 200 Insurance Revenue 200 ($2,400 annual × 1/12 = $200 per month for 12 months) Accrued Liability Expense incurred before cash is paid Examples: • Payroll • Taxes • Interest Record expense (and corresponding liability) in period incurred; pay for it in a future period No cash flow on recording, only when paid Accrued Liability Example Pay biweekly wages of $280,000 At end of month, between pay periods: Wages Expense 40,000 Wages Payable 40,000 Next payday: Wages Payable Wages Expense Cash 280,000 40,000 240,000 Accrued Liability Example #2 On March 1, assume a 9%, 90-day, $20,000 loan is taken out with a bank Initial journal entry: 3/1 Cash 20,000 Notes Payable 20,000 Monthly adjusting journal entry: 3/31 Interest Expense 150 Interest Payable 150 ($20,000 principal × 9% × 3/12 = $450 for 3 months or $450/3 = $150 per month) Accrued Liability Example #2 (continued) To record payment of a 9%, 90-day, $20,000 loan with interest due on May 30 5/30 Interest Payable Interest Expense Notes Payable Cash 300 150 20,000 20,450 Accrued Asset Revenue earned before cash is received Examples: • Rent • Interest Record revenue (and corresponding receivable) in period earned; receive payment in a future period Accrued Asset Example Rent payment of $2,500 due within first 10 days of month First day of the month: Rent Receivable Rent Revenue 2,500 2,500 Upon receipt of cash: Cash Rent Receivable 2,500 2,500 Adjusting Entry Summary Examples: Deferred Expense cash received before expense is incurred Deferred Revenue cash received before revenue is earned Accrued Liability expense incurred before cash is paid Accrued Asset revenue is earned before cash is received Steps in the Accounting Cycle 7. Close the accounts 1. Collect and analyze info 6. Record and post adjusting entries 5. Prepare financial statements 2. Journalize transactions 3. Post transactions to general ledger 4. Prepare work sheet LO6 The Closing Process Purpose: To return the balance of revenue, expense, and dividend accounts to zero to begin the next period to transfer the net income of the period to Retained Earnings Nominal Accounts Revenues Expenses Close to Income Summary Normal balance Normal balance Close to Income Summary $ XX $ XX $ XX $ XX Dividends Normal balance Close to Retained Earnings $ XX $ XX Zero out nominal accounts to start accumulation of next period’s results LO7 Closing Entries Income Summary $XX from expense accounts $XX from revenue accounts (Net loss) or Net Income closed to Retained Earnings Appendix Accounting Tools: Work Sheets Unadjusted Trial Balance Columns Begin by filling in the trial balance accounts and amounts LO8 The Adjusting Entries Columns Make adjustments; formal journal entries are prepared later Adjusted Trial Balance Columns The Income Statement Columns Extend revenue and expense account balances to the income statement The Balance Sheet Columns Extend asset, liability, and equity accounts to the balance sheet End of Chapter 4