Chapter 9: Monopolistic

Competition and Oligopoly

Copyright © 2005 by The McGraw-Hill Companies, Inc. All rights reserved.

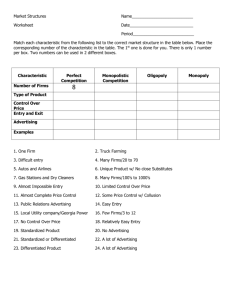

Monopolistic Competition

Monopolistic competition is a market

structure in which many firms sell a

differentiated product and entry into and

exit from the market are relatively easy.

Examples: furniture, jewelry, leather goods,

grocery stores, gas stations, restaurants,

clothing stores and medical care.

Copyright © 2005 by The McGraw-Hill Companies, Inc. All rights reserved.

Characteristics of

Monopolistic Competition

Relatively large number of sellers – firms

have small market shares, collusion is

unlikely and each firm can act independently

Differentiated products – the product is

slightly different and is often promoted by

heavy advertising

Easy entry to, and exit from, the industry –

economies of scale are few, capital

requirements are low but financial barriers

exist

Copyright © 2005 by The McGraw-Hill Companies, Inc. All rights reserved.

Differentiated Products

Product differentiation is a form of

nonprice competition in which a firm tries

to distinguish its product or service from all

competing ones on the basis of attributes

such as design and quality.

Production differentiation entails product

attributes, service, location, brand name

and packaging, and some control over

price.

Copyright © 2005 by The McGraw-Hill Companies, Inc. All rights reserved.

Advertising

The goal of product differentiation and

advertising is to make price less of a factor

in consumer purchases and make product

differences a greater factor.

The intent is to increase the demand for a

product and to make demand less elastic.

Copyright © 2005 by The McGraw-Hill Companies, Inc. All rights reserved.

Pricing and Output in

Monopolistic Competition

The demand curve of a monopolistically

competitive firm is highly, but not perfectly,

elastic.

The price elasticity of demand for a

monopolistic competitor depends on the

number of rivals and the degree of product

differentiation.

The larger the number of rival firms and the

weaker the product differentiation, the greater

the price elasticity of each firm’s demand.

Copyright © 2005 by The McGraw-Hill Companies, Inc. All rights reserved.

The Short Run: Profit or Loss

The monopolistically competitive firm

maximizes profit or minimizes loss in the

short run. It produces a quantity Q at

which MR = MC and charges a price P

based on its demand curve.

When P > ATC, the firm earns an economic

profit.

When P < ATC, the firm incurs a loss.

Copyright © 2005 by The McGraw-Hill Companies, Inc. All rights reserved.

The Long Run:

Only a Normal Profit

In the long-run, firms will enter a profitable

monopolistically competitive industry and

leave an unprofitable one.

A monopolistic competitor will earn only a

normal profit and price just equals average

total cost at the MR = MC output.

Copyright © 2005 by The McGraw-Hill Companies, Inc. All rights reserved.

The Long Run:

Only a Normal Profit

Because entry to the industry is relatively

easy, economic profits attract new rivals.

As new firms enter, the demand curve faced

by the typical firm shifts to the left, reducing its

economic profit.

When entry of new firms has reduced demand

to the extent that the demand curve is tangent

to the ATC curve at the profit-maximizing

output, the firm is just making a normal profit,

leaving no incentive for new firms to enter.

Copyright © 2005 by The McGraw-Hill Companies, Inc. All rights reserved.

The Long Run:

Only a Normal Profit

When the industry suffers short-run

losses, some firms will exit in the long run.

As firms exit, the demand curve of surviving

firms begins to shift to the right, reducing

losses until the firms are just making normal

profit.

Copyright © 2005 by The McGraw-Hill Companies, Inc. All rights reserved.

Pricing and Output in

Monopolistic Competition

Copyright © 2005 by The McGraw-Hill Companies, Inc. All rights reserved.

Monopolistic Competition

and Efficiency

In monopolistic competition, neither

productive nor allocative efficiency occurs

in long-run equilibrium.

Since the firm’s profit-maximizing price (and

average total cost) slightly exceed the lowest

average total cost, productive efficiency is not

achieved.

Since the profit-maximizing price exceeds

marginal cost, monopolistic competition

causes an underallocation of resources.

Copyright © 2005 by The McGraw-Hill Companies, Inc. All rights reserved.

Excess Capacity

The gap between the minimum ATC

output and the profit-maximizing output is

a monopolistically competitive firm’s

excess capacity.

Plants and equipment are unused because

the firm is producing less than the minimumATC output.

Monopolistically competitive industries are

overcrowded with firms each operating below

its optimal capacity.

Copyright © 2005 by The McGraw-Hill Companies, Inc. All rights reserved.

Product Variety

and Improvement

Despite the overcrowded feature,

monopolistic competition does promote

product variety and product improvement.

A firm earning a normal profit will develop and

improve its product in order to regain its

economic profit.

Successful product improvements by one firm

obligates rivals to imitate or improve on that

firm’s temporary market advantage or else

lose business.

Copyright © 2005 by The McGraw-Hill Companies, Inc. All rights reserved.

Oligopoly

Oligopoly is a market structure dominated

by a few large producers of homogeneous

or differentiated products.

Because of their “fewness”, oligopolists

have considerable control over their price.

Examples: tires, beer, cigarettes, copper,

greeting cards, steel, aluminum, automobiles

and breakfast cereals

Copyright © 2005 by The McGraw-Hill Companies, Inc. All rights reserved.

Characteristics of Oligopoly

A few large producers – firms are generally

large and together they dominate the

industry.

Either homogeneous or differentiated

products – the products are standardized, or

differentiated with heaving advertising.

Price maker – the firm can set its price and

output levels to maximize its profit.

Copyright © 2005 by The McGraw-Hill Companies, Inc. All rights reserved.

Characteristics of Oligopoly

Strategic behavior – Self-interested behavior

that takes into account the reactions of

others.

Mutual interdependence – each firm’s profit

depends not entirely on its own price and

sales strategies but also on those of the

other firms.

Blocked entry – barriers to entry exist which

make it hard for new firms to enter.

Copyright © 2005 by The McGraw-Hill Companies, Inc. All rights reserved.

Oligopoly Behavior: A

Game-Theory Overview

Game theory is the study of how people or

firms behave in strategic situations.

It can be used to analyze the pricing behavior of

oligopolists.

Suppose in a two-firm oligopoly (a duopoly),

each firm must chose a pricing strategy, high or

low.

A payoff matrix can be constructed to show

payoffs (profit) to each firm that result from each

combination of strategies.

Copyright © 2005 by The McGraw-Hill Companies, Inc. All rights reserved.

Game Theory Example

Two firms, A and B,

must decide on a

pricing strategy: price

high or price low.

Although firms A and B

are mutually

interdependent, both

can benefit from

collusion. However,

there may be incentive

to cheat.

Firm A

Price High Price Low

Firm B

Price

High

$12

$15

$6

$12

$6

Price

Low

$15

$8

$8

A

B

Copyright © 2005 by The McGraw-Hill Companies, Inc. All rights reserved.

Mutual Interdependence

Each firm’s profit depends on its own

pricing strategy and that of its rival.

In the example, if both firms adopt a highprice strategy, each firm will earn $12 million;

if both adopt a low-price strategy, each will

earn $8 million. If one firm adopts a low-price

strategy while the other adopts a high-price

strategy, the low-price firm will earn $15

million while the other firm earns $6 million.

Copyright © 2005 by The McGraw-Hill Companies, Inc. All rights reserved.

Collusive Tendencies

Oligopolists can often benefit from

cooperation, or collusion.

Collusion is a situation in which firms act

together and in agreement to fix prices,

divide markets, or otherwise restrict

competition.

In the example, firms A and B can agree to

establish and maintain a high-price strategy so

each can earn $12 million.

Copyright © 2005 by The McGraw-Hill Companies, Inc. All rights reserved.

Incentive to Cheat

Oligopolists might have an incentive to

cheat on a collusive agreement if they can

benefit from such action.

In the example, suppose firms A and B agree

to establish and maintain a high-price strategy.

Either firm can cheat and lower its price in

order to increase profit to $15 million (a $3

million increase).

Copyright © 2005 by The McGraw-Hill Companies, Inc. All rights reserved.

Incentive to Cheat

Because of possible incentives to cheat,

independent action by oligopolists may lead

to mutually “competitive” low-price

strategies, which benefit consumers but not

the oligopolists.

In the example, firms A and B will choose a

low-price strategy and earn $8 million each.

Copyright © 2005 by The McGraw-Hill Companies, Inc. All rights reserved.

Kinked-Demand Model

In the kinked-demand model, oligopolists

face a demand curve based on the

assumption that rivals will ignore a price

increase and follow a price decrease.

An oligopolist’s rivals will ignore a price

increase above the going price but follow a

price decrease below the going price.

The demand curve is kinked at this price and

the marginal-revenue curve has a vertical gap.

Copyright © 2005 by The McGraw-Hill Companies, Inc. All rights reserved.

Kinked-Demand Model

Copyright © 2005 by The McGraw-Hill Companies, Inc. All rights reserved.

Price Leadership

Price leadership involves an implicit

understanding that other firms will follow

the lead when a certain firm in the industry

initiates a price change.

A price leader is likely to observe the

following tactics:

Infrequent price changes

Communications

Avoidance of price wars

Copyright © 2005 by The McGraw-Hill Companies, Inc. All rights reserved.

Collusion

Collusion, through price control, may allow

oligopolists to reduce uncertainty, increase

profits, and possibly block potential entry.

One form of collusion is the cartel: a

formal agreement among producers to set

the price and the individual firm’s output

levels of a product.

Copyright © 2005 by The McGraw-Hill Companies, Inc. All rights reserved.

Joint-Profit Maximization

If oligopolistic firms produce an identical

product, and have identical cost, demand,

and marginal-revenue curves, than each

firm can maximize profit using the MR=MC

rule.

Copyright © 2005 by The McGraw-Hill Companies, Inc. All rights reserved.

A profitable oligopolist when rivals

charge the same price, Po

MC

Price

Po

Economic

Profit

ATC

D

Q0

MR

Quantity of output

Joint-Profit Maximization

If rivals charge prices lower than Po, then

the demand curve of the firm charging Po

will shift to the left as its customers turn to

its rivals, and its profits will fall.

The firm can retaliate and cut its price, too,

however, all firms’ profits would eventually fall.

Firms will choose to charge Po and

produce Qo because it is the most

profitable price-output combination.

Copyright © 2005 by The McGraw-Hill Companies, Inc. All rights reserved.

Obstacles to Collusion

Barriers to collusion beyond the antitrust

laws include:

Demand and cost differences

Number firms

Cheating

Recession

Potential entry

Copyright © 2005 by The McGraw-Hill Companies, Inc. All rights reserved.

Oligopoly and Advertising

Each firm’s share of the total market is

generally determined through product

development and advertising for two

reasons:

Product development and advertising

campaigns are less easily duplicated than

price cuts.

Oligopolists have sufficient financial resources

to engage in product differentiation and

advertising.

Oligopoly and Advertising

Positive effects of advertising are:

Enhances competition

Reduces consumers’ search time, direct

costs, and indirect costs

Facilitates the introduction of new products

Negative effects of advertising include:

Alters consumers’ preferences in favor of the

advertiser’s product

Brand-loyalty promotes monopoly power

Oligopoly and Efficiency

Many economists believe the oligopoly

market structure is neither productively

efficient nor allocatively efficient.

This is because many oligopolistic firms price

higher than average total cost and produce

less than the optimal output level.

Copyright © 2005 by The McGraw-Hill Companies, Inc. All rights reserved.

Oligopoly and Efficiency

A few believe that oligopoly is actually less

desirable than pure monopoly, because

government can guard against abuses of

monopoly power but not against informal

collusion among oligopolists that give the

outward appearance of competition

involving independent firms.

Copyright © 2005 by The McGraw-Hill Companies, Inc. All rights reserved.