rate of return

advertisement

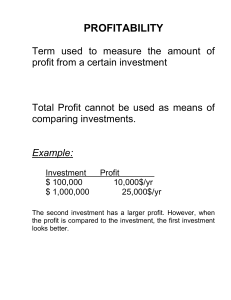

+ Rate of return + Sensitivity analysis coated membrane template Level 2 analysis Raw material costs = $100,000 Purchased equipment costs = $250,000 Lang factors at lowest value of the range Snapshot of TPC Case I tab P4 - membrane coating Basis: per year Materials direct costs (DC) fixed capital invest. (FCI) total capital invest. (TCI) land + buildings = Basis: Total product costs $100,000 $512,500 $729,737 $729,737 $35,000 1 from bill of materials tab from TCI tab from TCI tab from TCI tab from TCI tab year of operation + What is the sensitivity of TPC to raw material cost variations? ± 10%, one standard deviation of raw material costs (bulk chemicals); Standard deviation levels ± 1 standard deviation = 50% of the range ± 2 standard deviations = ~95% of the range For this case, ± 2 standard deviations of raw material costs would give $80,000 and $120,000 as the raw materials cost range Change raw materials costs on bill of materials Tab; read TPC result on TPC Case I Tab TPC vs. raw material costs ± 2 standard deviations; 10% = one standard deviation; notice the TPC sensitivity to raw materials costs total product cost 460,000 total product costs, $/year + 450,000 y = 1.3606x + 288775 R² = 1 440,000 430,000 420,000 410,000 400,000 390,000 0 25,000 50,000 75,000 100,000 125,000 150,000 raw material cost, $/year + What is the sensitivity of TPC to PEC cost variations? Capital cost estimates are within 35% of actual (we take this to be 2 standard deviations) Change PEC costs on PEC Tab; read TCI result on TCI Tab or read TCI, TPC results on TPC Case I Tab TCI, TPC vs PEC effect of PEC on TCI, TPC otal capital investment or total product cost + $1,400,000 y = 2.2438x + 387860 R² = 1 $1,200,000 $1,000,000 TCI $800,000 TPC $600,000 Linear (TCI) Linear (TPC) $400,000 y = 0.893x + 309063 R² = 1 $200,000 $0 $0 $200,000 Purchase equipment costs, $ $400,000 + How can you use sensitivity plots during design? Evaluate high-cost elements for the process, focus on reducing these Rapidly eliminate alternatives that exceed cost quality accuracy Refine cost estimates to evaluate alternatives that have costs within the expected accuracy of the costing methods + Costs due to interest on investment Money has a time value A business expects to receive a return on money invested The amount of the return is related to the degree of risk that the entire investment may be lost + Various investment cost elements Borrowed capital vs. owned capital Interest on owned capital cannot be charged as a true cost Interest effects in a small business $20,000 invested in a start-up – FCI + WC Profit = $8,000 Owned capital: profit = $8,000 Borrowed capital (10% interest): profit = $8,000 – 0.1*$20,000 = $6,000 + Interest effects in a large business New capital can come from issued stocks and bonds, borrowing from banks or insurance companies, depreciation funds set aside, profits not distributed to shareholders,… Source of capital Interest, Actual interest, dividend %/year dividend before taxes, %/yr Actual interest, dividend after taxes, %/yr Bonds 6 6 4 Bank loans 7 7 4.6 Preferred stock 7 10.6 7 Common stock 0 13.6 9 + Including cost of capital in economic analysis Capital is charged at a low interest rate – it could be used for alternative investments, i.e., it could pays off funded debts or be invested in risk-free loans Interest is paid on owned capital at a rate equal to the presetn return on all the company’s capital Design practice for interest and investment costs-alternatives No interest costs are included – all necessary capital comes from owned capital Interest is charged on the total capital investment at a set interest rate + Property taxes Taxes Local government jurisdiction – county or city Excise taxes Charges for import customs, transfer of stocks and bonds Gasoline, alcoholic beverages Indirect, as they are passed to the consumer There may be local excise taxes Income taxes Based on gross earnings = total income – total product cost Federal and state governments (0 – 5% of gross income) + Corporate taxes Normal tax – federal government Surtax – 2nd federal income tax based on gross earnings above a certain limit > $100,000: 34% tax rate Capital gains tax – tax on profits made for the sale of capital assets (land, buildings, equipment); long-term if held more than a year, short-term if held more than a year Contributions – tax deductible up to 10% of taxable income Carry-back, carry-forward of losses – 3 year window + Investment credit – deduction for new investments in machinery, equipment Taxes and depreciation – discussion to follow Excess-profits tax – (national emergencies) Tax returns Cash basis – only money received or paid out during the period Accrual basis – income and expenses included when they occur even if money is not yet received or sent + Depreciation methods Arbitrary, does not include interest costs Straight-line Declining balance Sum-of-the-years digits Accounts for interest on the investment Sinking fund Present worth methods Case study: Harsh’s car V = $20,000 Vs = $500 A = 15 years + deprecia on methods $20,000 Asset value (Harsh' car) Va, str line Va, declining Va, reciprocal Va, double declining $10,000 $0 0 5 10 Usage period, years 15 + Profitability standard Quantifiable standards only operate as guides to decisions Profit evaluation is based on prediction of future results [“…it is hard to make predictions, especially about the future.” – Yogi Berra] A primary factor in evaluations is the consideration of alternatives Typical choices Capital investment in a project with high risk Capital investment in a safe venture + Five common methods for profitability evaluations 1. Rate of return on investment 2. Discounted cash flow on full-life performance 3. Net present worth 4. Capitalized costs 5. Payout period + 1. Rate of return (RoR) Annual RoR on TCI, before taxes = annual profit/(TCI + WC) Annual RoR on TCI, after taxes. Modify annual profit by taxes Annual RoR, capital recovery with minimal profit Generate fictitious expenses at min profit, divide by (TCI+WC) + Example: Rate of return on investment + RoR advantages TCI, WC, income, expenses disadvantages No time value of money Assumes constant costs for projects Depreciation may vary Maintenance costs increase with time Sales volume may increase or decrease + 2. Discounted cash flow rate of return We determine an index (i), or interest rate, that discounts the annual flows to a zero present value at the end of the project life, when properly compared to the initial investment What does i represent? The after-tax interest rate at which the investment is repaid by proceeds from the project, or The maximum after-tax interest rate at which funds could be borrowed for the investment and just break even at the end of the service life. + Discounted cash flow rate of return What is the interest at which this project will pay principal + interest at end of life? Addresses time value of money Computes amount of investment unreturned @ each year over the project life Trial-and-error solution: vary RoR so that the initial investment goes to zero at the end of the project ife It gives the maximum interest rate at which capital can be borrowed when net cash flow just pays all the principle and interest + Estimated cash flow to project year Cash flow to project 0 (110,000) = -(TCI+WC) 1 30,000 2 31,000 3 36,000 4 40,000 5 43,000 + 3. Net present worth Complementary to DCC RoR Substitutes the cost of capital at an interest rate, i, for the discounted cash flow rate of return For the data provided in the DCC ROR problem, we set the interest rate, say 15%, and compute the difference between the present value of the annual cash flows and the initial required investment + + Spreadsheet structure for DCF of present value and net present worth Source: Peters, Timmerhaus, West + 4. Capitalized costs This method is useful for comparing alternatives within a single overall project. Capitalized costs related to investment: Money for initial purchase of equipment, and Generating sufficient funds via interest accumulation to permit perpetual replacement (i.e., sustainability) Example: one process section has alternatives + low or no differences in operating costs, then the alternative giving the least capitalized cost would be the desirable economic choice. + Capitalized costs K= capitalized cost V= initial equipment cost Vreplace = equipment replacement cost n= estimate useful life, years i= interest rate Capitalized cost factor + Capitalized costs inclusion of operating costs Operating costs can be included by adding an additional capitalized cost to cover operating costs during the project life Each annual operating cost is considered as equivalent to a piece of equipment that lasts one year Procedure: Find present (discounted) value of each year’s costs by the prior method (discount factor is applied, d=1/(1+i)n) S Pvi is capitalized by multiplying by the capitalization factor for the initial investment. The total capitalized costs is the sum of this value + operating costs + working capital. + 5. Payout period Minimum length of time necessary to recover the original capital investment via cash flow to the project, based on total income minus all costs except depreciation Interest effects are neglected + Comparison of alternative investments: 5 profitability methods 3 investments with: • different TCI, WC • different service lives • different cash flow and expenses 1. Rate of return on investment 2. Discounted cash flow on full-life performance 3. Net present worth 4. Capitalized costs 5. Payout period + 3 investments investment characteristics investment FCI, $ 1 $ 100,000 2 $ 170,000 3 $ 210,000 WC, $ $ $ $ 10,000 10,000 15,000 Vs, $ $ $ $ 10,000 15,000 20,000 n cash flow annual cash after taxes, expenses, $ $ 5 tabulated $ 44,000 7 $ 52,000 $ 28,000 8 $ 59,000 $ 21,000 cash flow after taxes = total annual income/revenue minus all costs save depreciation and investment interest annual cash expenses = operation, maintenance, taxes, insurance = total annual income - annual cash flow For investment 1: year 1 = $30,000; year 2 = $31,000; year 3 = $36,000; year 4 = $40,000; year 5 = $43,000 investment characteristics investment FCI, $ 1 $ 100,000 2 $ 170,000 3 $ 210,000 WC, $ $ $ $ 10,000 10,000 15,000 Vs, $ $ $ $ 10,000 15,000 20,000 n cash flow annual cash after taxes, expenses, $ $ 5 tabulated $ 44,000 7 $ 52,000 $ 28,000 8 $ 59,000 $ 21,000 cash flow after taxes = total annual income/revenue minus all costs save depreciation and investment interest annual cash expenses = operation, maintenance, taxes, insurance = total annual income - annual cash flow For investment 1: year 1 = $30,000; year 2 = $31,000; year 3 = $36,000; year 4 = $40,000; year 5 = $43,000 + 1. Rate of return on initial investment + Investment 1 Investment 1 TCI $100,000 depreciation cash flow to project year 0 1 2 3 4 5 salvage -$100,000 $30,000 $31,000 $36,000 $40,000 $43,000 $10,000 average profit total initial $ WC Vs $10,000 $18,000 N $10,000 average profit annual CF 5 average annual RoR 16.4% $12,000 $13,000 $18,000 $22,000 $25,000 $18,000 per year $110,000 annual expenses $44,000 avg profit/(FCI+Vs) + Investment 2 Investment 2 TCI $170,000 depreciation cash flow to project year 0 1 2 3 4 5 6 7 salvage -$170,000 $52,000 $52,000 $52,000 $52,000 $52,000 $52,000 $52,000 $10,000 average profit total initial $ WC Vs $10,000 $22,143 N $15,000 average profit annual CF annual expenses 7 52000 $28,000 average annual RoR 16.6% $29,857 $29,857 $29,857 $29,857 $29,857 $29,857 $29,857 $29,857 per year $180,000 avg profit/(FCI+Vs) + Investment 3 Investment 3 TCI $210,000 depreciation cash flow to project year 0 1 2 3 4 5 6 7 8 salvage -$210,000 $59,000 $59,000 $59,000 $59,000 $59,000 $59,000 $59,000 $59,000 $10,000 average profit total initial $ N Vs WC $15,000 $23,750 $20,000 average profit annual CF annual expenses $21,000 $59,000 8 average annual RoR 15.7% $35,250 $35,250 $35,250 $35,250 $35,250 $35,250 $35,250 $35,250 $35,250 per year $225,000 avg profit/(FCI+Vs) + Summary table investment initial $ profit (avg) avg RoR 1 $110,000 $18,000 16.4% 2 $180,000 $29,857 16.6% 3 $225,000 $35,250 15.7% Which do we choose? All have similar average rates of return? All are above the ‘minimum’ 15% return. + Average RoR, incremental investment We can also compare these investments to each other as follows: The project investment follows the order, 1,2, and 3 Pairwise, find the ratio of the profit difference to the initial investment difference The investment with the highest value is preferred + Differential rate of return D differential comparison D profit investment RoR 2 to 1 $11,857 $70,000 16.9% 3 to 2 $5,393 $45,000 12.0% Project 2 is better than project 1; Project 2 is better than project 3 (less efficient use of capital for 3) investment characteristics investment FCI, $ 1 $ 100,000 2 $ 170,000 3 $ 210,000 WC, $ $ $ $ 10,000 10,000 15,000 Vs, $ $ $ $ 10,000 15,000 20,000 n cash flow annual cash after taxes, expenses, $ $ 5 tabulated $ 44,000 7 $ 52,000 $ 28,000 8 $ 59,000 $ 21,000 cash flow after taxes = total annual income/revenue minus all costs save depreciation and investment interest annual cash expenses = operation, maintenance, taxes, insurance = total annual income - annual cash flow For investment 1: year 1 = $30,000; year 2 = $31,000; year 3 = $36,000; year 4 = $40,000; year 5 = $43,000 + Minimum payout period No interest charge + Minimum payout period no interest charge investment depr. FCI avg profit/yr avg depr./yr payout period 1 $90,000 $18,000 $18,000 2.50 2 $155,000 $29,857 $22,143 2.98 3 $190,000 $35,250 $23,750 3.22 Investment 1 has the lowest payout period, and is recommended investment characteristics investment FCI, $ 1 $ 100,000 2 $ 170,000 3 $ 210,000 WC, $ $ $ $ 10,000 10,000 15,000 Vs, $ $ $ $ 10,000 15,000 20,000 n cash flow annual cash after taxes, expenses, $ $ 5 tabulated $ 44,000 7 $ 52,000 $ 28,000 8 $ 59,000 $ 21,000 cash flow after taxes = total annual income/revenue minus all costs save depreciation and investment interest annual cash expenses = operation, maintenance, taxes, insurance = total annual income - annual cash flow For investment 1: year 1 = $30,000; year 2 = $31,000; year 3 = $36,000; year 4 = $40,000; year 5 = $43,000 + Discounted cash flow RoR Investment 1 FCI $100,000 WC $10,000 n= 5 years salvage $10,000 interest rate when investment is just repaid by the cash flow at end of service life RoR estimate of i 20.7% use Solver, Goal Seek to find i for residual = 0 cash flow to project discount present year cash flow factor value 0 $110,000 1 $30,000 0.8284 $24,852 2 $31,000 0.6862 $21,273 3 $36,000 0.5685 $20,464 4 $40,000 0.4709 $18,836 5 $43,000 0.3901 $16,774 WC+salvage $20,000 $7,802 sum CF $200,000 net present value $110,000 TCI + WC $110,000 when residual = 0, net cash flow just pays for principal + interest residual = $0 target value Investment 2 FCI $170,000 WC $10,000 n= 7 years salvage $15,000 interest rate when investment is just repaid by the cash flow at end of service life RoR estimate of i 22.8% use Solver, Goal Seek to find i for residual = 0 cash flow to project discount present year cash flow factor value 0 $170,000 1 $52,000 0.8145 $42,356 2 $52,000 0.6635 $34,501 3 $52,000 0.5404 $28,102 4 $52,000 0.4402 $22,890 5 $52,000 0.3586 $18,645 6 $52,000 0.2921 $15,187 7 $52,000 0.2379 $12,371 WC+salvage $25,000 $5,947 sum CF $389,000 net present value $180,000 TCI + WC $180,000 when residual = 0, net cash flow just pays for principal + interest residual = $0 target value Investment 3 FCI $210,000 WC $15,000 n= 8 years salvage $20,000 interest rate when investment is just repaid by the cash flow at end of service life RoR estimate of i 21.4% use Solver, Goal Seek to find i for residual = 0 cash flow to project discount present year cash flow factor value 0 $210,000 1 $59,000 0.8240 $48,618 2 $59,000 0.6790 $40,064 3 $59,000 0.5596 $33,014 4 $59,000 0.4611 $27,205 5 $59,000 0.3800 $22,418 6 $59,000 0.3131 $18,473 7 $59,000 0.2580 $15,223 8 $59,000 0.2126 $12,544 WC+salvage $35,000 $7,441 sum CF $507,000 net present value $225,000 TCI + WC $225,000 when residual = 0, net cash flow just pays for principal + interest residual = $0 target value + DCF RoR DCD RoR’s are similar: 20.7%, 22.8%, and 21.4% This method works well when the service lives of the projects are the same; with different service lives, the net present worth method is better Approximate method, narrow range of service lives Pair-wise comparison: base time is the longer service life investment characteristics investment FCI, $ 1 $ 100,000 2 $ 170,000 3 $ 210,000 WC, $ $ $ $ 10,000 10,000 15,000 Vs, $ $ $ $ 10,000 15,000 20,000 n cash flow annual cash after taxes, expenses, $ $ 5 tabulated $ 44,000 7 $ 52,000 $ 28,000 8 $ 59,000 $ 21,000 cash flow after taxes = total annual income/revenue minus all costs save depreciation and investment interest annual cash expenses = operation, maintenance, taxes, insurance = total annual income - annual cash flow For investment 1: year 1 = $30,000; year 2 = $31,000; year 3 = $36,000; year 4 = $40,000; year 5 = $43,000 + Net present worth Investment 1 FCI $100,000 WC $10,000 n= 5 years salvage $10,000 RoR estimate of i 15.0% set minimum interest target cash flow to project discount present year cash flow factor value 0 $110,000 1 $30,000 0.8696 $26,087 2 $31,000 0.7561 $23,440 3 $36,000 0.6575 $23,671 4 $40,000 0.5718 $22,870 5 $43,000 0.4972 $21,379 WC+salvage $20,000 $9,944 sum CF $200,000 net present value TCI + WC net present worth = $127,390 $110,000 $17,390 Investment 2 FCI $170,000 WC $10,000 n= 7 years salvage $15,000 RoR estimate of i 15.0% set minimum interest target cash flow to project discount present year cash flow factor value 0 $170,000 1 $52,000 0.8696 $45,217 2 $52,000 0.7561 $39,319 3 $52,000 0.6575 $34,191 4 $52,000 0.5718 $29,731 5 $52,000 0.4972 $25,853 6 $52,000 0.4323 $22,481 7 $52,000 0.3759 $19,549 WC+salvage $25,000 $9,398 sum CF $389,000 net present value TCI + WC net present worth = $225,740 $180,000 $45,740 Investment 3 FCI $210,000 WC $15,000 n= 8 years salvage $20,000 RoR estimate of i 15.0% set minimum interest target cash flow to project discount present year cash flow factor value 0 $210,000 1 $59,000 0.8696 $51,304 2 $59,000 0.7561 $44,612 3 $59,000 0.6575 $38,793 4 $59,000 0.5718 $33,733 5 $59,000 0.4972 $29,333 6 $59,000 0.4323 $25,507 7 $59,000 0.3759 $22,180 8 $59,000 0.3269 $19,287 WC+salvage $35,000 $11,442 sum CF $507,000 net present value TCI + WC net present worth = $276,194 $225,000 $51,194 + Net present worth Investment 1 = $17,400 Investment 2 = $45,700 Investment 3 = $51,200 Project 3 is preferred investment characteristics investment FCI, $ 1 $ 100,000 2 $ 170,000 3 $ 210,000 WC, $ $ $ $ 10,000 10,000 15,000 Vs, $ $ $ $ 10,000 15,000 20,000 n cash flow annual cash after taxes, expenses, $ $ 5 tabulated $ 44,000 7 $ 52,000 $ 28,000 8 $ 59,000 $ 21,000 cash flow after taxes = total annual income/revenue minus all costs save depreciation and investment interest annual cash expenses = operation, maintenance, taxes, insurance = total annual income - annual cash flow For investment 1: year 1 = $30,000; year 2 = $31,000; year 3 = $36,000; year 4 = $40,000; year 5 = $43,000 + Capitalized costs + Capitalized cost method Determine the capitalized cost for the original investment such that we could achieve an indefinite number of replacements + the capitalized present value of the cash expenses + working capital Method Get the present value of the annual cash expenses Determine the capitalized present value These are computed at the target interest rate, 15% capitalized costs investment FCI, $ WC, $ Vs, $ n 1 $100,000 $10,000 $10,000 2 $170,000 $10,000 $15,000 3 $210,000 $15,000 $20,000 target interest = Investment 1 2 3 annual cash flow cash after taxes, expenses, $ $ 5 tabulated $44,000 7 $52,000 $28,000 8 $59,000 $21,000 15% Cr Vs Cn $90,000 $10,000 $44,000 $155,000 $15,000 $28,000 $190,000 $20,000 $21,000 we want the minimum capitalized cost capitalized capitalized Wc cost cost factor $10,000 $492,323 1.99 $10,000 $460,039 1.60 $15,000 $457,277 1.49 n 5 7 8 + ANALYSIS: 5 METHODS 1. Rate of return on investment: project 2 preferred 2. Discounted cash flow on full-life: project 3 preferred 3. Net present worth: project 3 preferred 4. Capitalized costs: project 3 preferred 5. Payout period: project 1 preferred + CRITIQUE RoR, initial investment: does not include the time value of money Minimum payout period: does not include the time value of money DCF RoR, net present worth, capitalized costs: All include the time value of money While project 3 is preferred over project 2, the choice is narrow A more accurate evaluation is needed Go from straight line to a more realistic depreciation method Go from end-of-year costs to continuous interest compounding Variations in prestart-up costs between alternatives may be a factor to consider + Some heuristics for profitability Select smallest investment for needed service that gives the required return for the company Challenge the accuracy of your estimates: service life for example Consider process risk, particularly if you select a project with a larger-thannecessary investment Turbulent times = usually invest minimum capital Perceived value: green processes can have significant marketing advantages Other factors: gut feel, beat your competition, expand an existing plant,… + Rate of return GOOD LUCK!!!