INTERMEDIATE

ACCOUNTING

Sixth Canadian Edition

KIESO, WEYGANDT, WARFIELD, IRVINE, SILVESTER, YOUNG, WIECEK

Prepared by:

Gabriela H. Schneider, CMA; Grant MacEwan College

CHAPTER

13

Intangible Assets

Learning Objectives

1. Describe the characteristics of intangible assets.

2. Discuss the recognition and measurement

issues of acquiring intangibles.

3. Explain how specifically identifiable intangibles

are valued subsequent to acquisition.

4. Identify the types of specifically identifiable

intangible assets.

5. Explain the conceptual issues related to

goodwill.

Learning Objectives

6. Describe the accounting procedures for recording

goodwill at acquisition and subsequently.

7. Differentiate between research and development

expenditures and describe and explain the

rationale for the accounting for each.

8. Identify other examples of deferred charges and

the accounting requirements for them.

9. Identify the disclosure requirements for

intangibles, including deferred charges.

Intangible Assets

Intangible Asset Specifically

Issues

Identifiable

Intangibles

Goodwill

Characteristics

Patents

Recognition

Current

standards

Copyrights

Negative

Goodwill

Trademarks

Recognition and

Leaseholds

measurement at

Franchises

acquisition

Valuation after

acquisition

Intellectual Deferred Charges

Financial

Capital

and Long-term

Statement

Prepayments

Disclosure and

Presentation

Valuation after

acquisition

Impairment

Balance Sheet

Research and

development

Income

costs

Statement

Pre-operating

Illustrative

costs

disclosures

Initial operating

losses

Organization costs

Advertising costs

Conceptual

questions

Intangibles: Characteristics

CICA Handbook, Section 3062, broadly

•

defines intangible assets as:

lacking physical existence

non-financial assets

•

•

•

Characteristics include:

identifiability

2. manner of acquisition

3. expected period of benefit

4. separability from an entire enterprise

1.

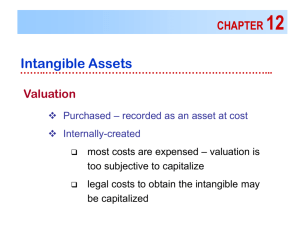

Recognition and Measurement

Purchased Intangibles

• Measured at cost – fair value at acquisition

• Cost follows same definition as with tangible capital

assets

• Purchase of identifiable intangibles is generally

straightforward

– Value is more easily determined

• Business combinations leads to goodwill

• Goodwill: (as an example)

– does not generate easily identifiable cash flows

– is not readily separable from the business entity

– control does not lead to contractual or legal rights

• Value (cost) of goodwill becomes a residual amount

Recognition and

Measurement

• Goodwill should be accounted for and

reported separately from other

intangibles

• Identifiable intangibles with similar

characteristics should be grouped and

reported together

• Subsequent costs (betterments) are

capitalized

Valuation of Intangible

Assets

Intangibles

InternallyCreated

Purchased

Specifically

Identifiable

Goodwilltype assets

Deferred

Charges

Specifically

Identifiable

Capitalize

Capitalize

Capitalize

Restricted

Amounts

Expense,

except direct

costs

Goodwill

type assets

Expense

Valuation after Acquisition

• Intangibles are written-off over their useful

lives, where the assets have determinable useful

lives, not exceeding 40 years

• Where the intangibles have indeterminable

useful lives, they must be written-off over a

period not exceeding 40 years

• If the intangibles have an indefinite infinite life,

the asset remains in the accounts unless it

becomes impaired or its life becomes finite

• Intangibles are considered to have no residual

(salvage) value

Valuation after Acquisition

•

Factors to consider when determining

economic useful life of an intangible:

1. Expected future usage

2. Effects of technological or commercial

obsolescence

3. Level of maintenance expenditures required to

obtain future benefits

•

Method of amortization should be chosen to

match the benefits received, otherwise,

straight-line amortization is used

Specific Intangibles: Types

•

Patents

–

•

Copyrights

–

•

•

relating to creations of authors, painters,

musicians and artists

Trademarks and Trade Names

Leaseholds

–

•

product patents and process patents

Lease Prepayments, Leasehold Improvements and

Capital Leases

Franchises and Licenses

Patents

• A patent gives an exclusive right to the holder

for 20 years

• Costs of purchasing patents are capitalized

• Costs to research and develop patents are

expensed as incurred

• Patents are amortized over the shorter of the

legal life (20 years) or their useful lives

– Normally amortized over 17 years

– First 3 years required to process a patent application

Copyrights

• Copyrights are granted for life of the creator,

plus 50 years

• Copyrights can be sold or assigned, but can

not be renewed

• Copyrights are amortized over their useful life

(not to exceed 40 years)

• Costs of acquiring copyrights are capitalized

• Research and development costs involved are

expenses as incurred

Trademarks and

Trade Names

• Trademarks and trade names are renewable

indefinitely by the original user in periods of

20 years each

• For accounting purposes, trademarks and

trade names are amortized over periods not

exceeding 40 years

• Costs of acquired trademarks or trade names

are capitalized

• If trademarks or trade names are developed

by the business, all direct costs (except R&D

costs) are capitalized

Leaseholds

• A leasehold is a contractual agreement

Details:

– agreement between the lessor (owner) and

the lessee (renter)

– gives the lessee the right to use the

property

– valid for a specific period of time

– in return for stipulated, periodic cash

payments

Leaseholds and Leasehold

Improvements

• Lease prepayments are to be shown as

prepaid expenses, not as intangible assets

• Leasehold improvements (made by the lessee)

revert to the lessor at end of lease term

• Leasehold improvements are amortized over

the shorter of the remaining term of the lease

or useful life of the improvements

• Leasehold improvements are generally shown

in the (tangible) property, plant, and

equipment section

Leases (Capital Leases)

• If the lease agreement transfers all

benefits and risks, the lease is classified

as a capital lease

• The lease is shown as a tangible asset

(at the capitalizable cost), rather than

as an intangible asset

Franchises and Licenses

• A franchise is a contractual agreement

under which the franchisor grants the

franchisee the right to:

– sell certain products or services

– use certain trademarks or trade names

– perform certain functions within a certain

geographical area

Franchises and Licenses

• A franchise may exist for a limited time or for

an indefinite time period

• The cost of a franchise (for a limited time), is

amortized over the franchise term

• A franchise (for an unlimited time), is

amortized over a period not exceeding 40 years

• If a franchise is deemed worthless, the cost

must be written-off immediately

• Annual payments for a franchise are expensed

Goodwill

• Goodwill: the excess of the cost (purchase

price) over the amounts (price) assigned to

tangible and intangible net assets

• Goodwill is the most intangible of all

assets

• Goodwill can be sold only with the

business

Acquired Goodwill: Valuation

Given:

Purchase price (cash):

Book value of assets:

Liabilities:

Market value of assets:

Determine goodwill.

$

$

$

$

400,000

255,000

55,000

350,000

Acquired Goodwill:

Calculation

Goodwill = Purchase Price - Fair value of net assets

$400,000 less 350,000 = $50,000

Entry in the books of the Purchaser:

Assets (various) 405,000

Goodwill

50,000

Liabilities

55,000

Cash

400,000

Negative Goodwill

• “Badwill” or bargain purchase

– Fair value of acquired assets is greater than the

purchase price

• CICA Handbook, Section 1581

– Excess is used to reduce the amounts assigned to

the other acquired assets, except for:

•

•

•

•

financial assets (other than equity method investments)

assets to be sold

future tax assets

prepaid assets that relate to employee future benefit plans

– If any excess remains after such assignment,

remainder treated as an extraordinary gain

Intellectual Capital

• Also known as knowledge assets

• Include (among others), the following:

–

–

–

–

Value of key personnel

Organization adaptability

Customer retention

Strategic direction

• Conceptually cannot be reported as assets as

the company does not have control

• They do, however, create long-term value

(and benefit) to the company

Deferred Charges and

Long-term Prepayments

• Research and Development Costs (R&D)

• Pre-operating and start-up costs

• Organization costs

• CICA Handbook, Section 3070 requires

separate disclosure of deferred charges

and their amortization amounts

Research and Development

(R&D) Costs

• R&D costs not in themselves intangible assets

• They are generally material in amount, and lead to

something that will be patented or copyrighted

• They therefore warrant special consideration

• Challenges in R&D accounting:

• Determining the costs associated with a particular activity or

project

• Determining the size of future benefits, and for how long those

benefits may be realized

• CICA Handbook, Section 3450 governs the accounting of

R&D costs

• All research costs charged to expense when incurred

• Development costs are charged to expense except in certain

defined circumstances

Research and Development

(R&D) Costs

• Research activities:

• involve planned search or critical investigation

aimed at discovery of new knowledge

• may or may not be directed towards a specific

project

• Development activities include:

• translation of research findings or other

knowledge into a plan or design for a new product

or process

• significant improvement to an existing product or

process

Research and Development

(R&D) Costs

•

R&D costs include the following:

1. Direct materials and direct labour

2. Amortization of tangible and intangible assets

used/related to R&D activities

3. Reasonable overhead allocation

•

•

R&D costs are expensed

Development costs are capitalized when all

five of the following conditions are met and

future benefits are reasonably certain

Research and Development

(R&D) Costs

Development cost capitalization criteria:

1. Product/process clearly defined, and costs

can be identified

2. Technical feasibility has been established

3. Management intent to produce and market

or use the product/process

4. If the intent is to sell, a market is clearly

defined. If the intent is to use, there is a

definable use/need

5. Resources exist to complete the project

Pre-operating Costs

•

Costs incurred prior to formal operations

beginning

•

EIC-27 allows for the deferral of pre-

operating costs if three conditions are met:

1. The expenditure relates directly to the business

2. It would not have been incurred if not for the

business

3. The amount is likely to be recovered from future

operations

Financial Statement

Disclosure and Presentation

• Balance Sheet

– Goodwill must be reported as a separate

line item

• Income Statement

– Amortization methods and rates are

disclosed

– Goodwill impairment loss is reported

separately

COPYRIGHT

Copyright © 2002 John Wiley & Sons Canada, Ltd.

All rights reserved. Reproduction or translation of

this work beyond that permitted by CANCOPY

(Canadian Reprography Collective) is unlawful.

Request for further information should be

addressed to the Permissions Department, John

Wiley & Sons Canada, Ltd. The purchaser may

make back-up copies for his / her own use only and

not for distribution or resale. The author and the

publisher assume no responsibility for errors,

omissions, or damages, caused by the use of these

programs or from the use of the information

contained herein.