Indexing Options and More June 20, 2012 Tim Hill, FSA

Indexing Options and More

June 20, 2012

Tim Hill, FSA, MAAA

Milliman, Inc.

1

A Historical Look at US FIA Annual Sales

2

Source: AnnuitySpecs

3

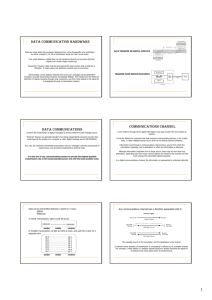

Full year 2011 FIA Sales Results

Full year 2011 VA Sales – Top Ten Companies ($ in millions)

12/31/

11

Rank

Company 2011

Sales

% Chg. vs. 2010

Q4 11Mkt

Share

1 Allianz Life $6,319 -7.8% 19.5%

2 Aviva 4,506 -13.9% 13.9%

3

4

American Equity

GAFRI

4,371

1,847

6.4%

115.1%

13.5%

5.7%

5

6

7

North American

Lincoln National

Midland National

1,673

1,615

1,554

8.4%

-20.3%

-1.5%

5.2%

5.0%

4.8%

8 Jackson National

9 ING

10 Security Benefit

1,497

1,361

941

-11.0%

-23.4%

New

4.6%

4.2%

2.9%

Source: AnnuitySpecs

4

Rate Environment – June 16, 2012

Product Trends

Surrender Charges

Over 50% have 10-year SC

Over 75% have SC <= 10-years

Continued but slowing trend toward 10 / 10

IIPRC, Florida

Agent Commission

Modest trend toward lower commissions

In low rate environment, seems like there will have to be additional cuts

In Bank annuity space clear trend to trade comp for volume

Bonuses

Vast majority of sales include a bonus

Typical bonuses are 5 – 10%

Vesting schedules are a typical way to recoup bonus

Portion of bonus might come with a rider

Average Issue age is 65 unchanged

Qualified percent is unchanged

Average size unchanged

5

6

Product Trends – GLWBs

GLWBs

GLWBs are not as prevalent as on the VA side but growing

On some products, portion electing GLWB > 95%

Overall election likely in the 50 – 60%

Typical Structure

Premiums accumulated at a set percent

6% to 8% compound

7% to 10% simple

Often for 10 years with one renewal available

Payout factors that are similar to VA side

5.0% to 5.5% at 65

Charge is typically bps of benefit base assessed against AV

Challenges

Low interest rate environment

Actuarial Guideline 33

Continued need for bonus and comp

Product Trends – New Indices

7

Current fixed buckets in FIAs between 1.0% and 1.5%

Current caps are around 3 to 4% on S&P 500 strategies

Difficult to tell upside story

How does a company

Blended indices

Blend S&P 500 with a fixed crediting rate

Fixed crediting rate might be low to subsidize S&P portion

0% credited interest Floor applied in aggregate

Use of spread instead of cap to get more upside

Alternative indices

Use a index with lower volatility than S&P 500

Trading off return potential for lower costing option

Challenges

Need to be able to buy option, less liquid than S&P

Limited number of option sellers

No historic experience – Must rely on backcasting

8

Option Pricing 101

Four Inputs into the price of an option

Examples assumes a 2% option budget which would be able to buy a 4% cap or a 20% participation rate

Risk-free interest rate

Typically the swap curve rate for the maturity of the option

1-yr swap curve on 6/14/2012 was 54 bps

Capped strategy

If rate rose to 104 bps, cost of option only increases by a few bps

But, if my option budget increased by 50 bps, could buy 5% cap

Participation rate strategy

If rate rose to 104 bps, cost of option only increases by a few bps and pushes participation rate to 19%

But, if my option budget increased by 50 bps, could buy 25% participation rate

9

Option Pricing 101

Implied Volatility

Volatility is not just a single number but is a complicated surface

1-yr at-the-money vol in example is 19.26%

Capped strategy

If vol cut to 15%, cost of option only decreases by a few bps

Still can only offer 4% cap

Participation rate strategy

If vol cut to 15%, cost of option cut by 19%, pushing participation to 25%

10

Option Pricing 101

Dividend Rate

Since crediting strategies typically use index without dividend, the dividend rate is an input in the option pricing formula

In example dividend assumed to be 2.0%

Capped strategy

If dividend increased to 3%, cost of option decreases by 10 bps allowing cap to increase to 4.25%

Participation rate strategy

If dividend increased to 3%, cost of option cut by 5%, pushing participation to 22%

11

Option Pricing 101

Length of Option

The last input into the option pricing formula is length

In example assumed 1-year option

Capped strategy

If length extended to 2 years, cost of option increases by 11 bps

But, since I only have to buy the option every 2 years I have double the option budget or 4%

Can push cap up to 8%

Participation rate strategy

If length extended to 2 years, cost of option increased by 55%

But, since I only have to buy the option every 2 years I have double the option budget or 4%

Can push participation rate to 25%

12

Creating an Uncapped Strategy

Suppose wanted to create a, 100% participation, uncapped crediting strategy with no spread

Willing to push crediting length to 5 years

Gives an option budget of 5 times 2% = 10%

S&P 500 option would cost around 21.4%

Need to find index with lower volatility

Low Vol S&P 500 uses the 100 stocks subset with the lowest vols

Option would cost around 15%

Defensive funds

Option could cost around 12%

Other possibilities

Blend fund with bond fund or other low correlation fund

Blend with a fixed account paying a crediting rate less than option budget

13

Creating an Uncapped Strategy

Use of spread

Products that have used a spread have traditional back-casted well

S&P 500 has thicker tails (meaning more extreme good and bad years) than option pricing assumes

Getting all of the good years after the first x%

Very sensitive to implied volatility

Buying-up the crediting parameter

Use of a charge to increase the option budget and increase what is offered

Mixed results to date

Extending option reset period beyond 5-years

12-year S&P 500 option in theory could be uncapped with 100% participation and no spread

Would need to find investment bank to price it.

14

Challenges of Using New Indices

Backcasting

Most indices that would be considered are based on set formula

Substitutions can be found for indices that didn’t exist

Third party should be used to do calculation

Marketing

Challenges of gaining acceptance versus familiar

Purchasing options

Limited sources to buy options

Likely best to find a single partner and agree upon parameters

Regulatory

Insure that no way index could be manipulated

Transparency critical

Need to carefully craft marketing materials

15

FIA Predictions

Vast majority of sales still through IMOs

Continued attention on GLWBs

Significant activity in new indices

Continued and accelerated attention from Banks and

Wirehouses

Partial due to challenges on VA side

Desire to tell income story

Moderated product

Sales likely flat due to low interest rate environment

Progress (hopefully) made on AG 33 issues