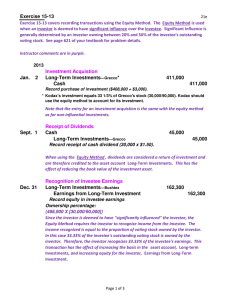

Chapter One

The Equity

Method of

Accounting for

Investments

McGraw-Hill/Irwin

Copyright © 2013 by The McGraw-Hill Companies, Inc. All rights reserved.

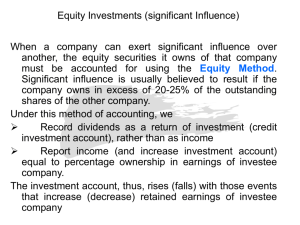

LO 1

Accounting for Investments in

Corporate Equity Securities

GAAP recognizes 3 ways to report

investments in other companies:

Fair-Value Method

Consolidation

Equity Method

The method selected depends upon the degree

of influence the investor has over the investee.

1-2

1-3

Fair Value Method

Investments in equity securities are recorded at cost

and subsequently adjusted to fair value.

Investments classified as Trading Securities:

Held for sale in the short term.

Unrealized holding gains and losses are included in

earnings (net income).

Investments classified as Available-for-Sale

Securities:

Any Securities not classified as Trading.

Unrealized holding gains and losses are reported in

shareholders’ equity as other comprehensive income

(i. e., not included in net income).

1-3

1-4

Consolidation of

Financial Statements

Required when:

• Investor’s ownership exceeds 50% of

investee

•

except when control does not rest with

the majority investor

• One set of financial statements prepared

to consolidate all accounts of the parent

company and all of its controlled subsidiaries

AS A SINGLE ENTITY.

1-4

1-5

LO 2

Equity Method

Use when:

• Investor has the ability to exercise

significant influence on the

investee operations (whether influence is

applied or not)

• Generally used when ownership is

• between 20% and 50%.

• Significant Influence might be present

with much lower ownership percentages.

1-5

1-6

International Standard 28

Investment in Associates

The International Accounting Standards Board (IASB),

similar to FASB, defines “significant influence” as the

power to participate in the financial and operating

policy decisions of the investee, but it is not control or

joint control over those policies.

If investor has 20% or more ownership, it is presumed

to have significant influence, unless it is demonstrated

not to be the case.

If investor holds less than 20% ownership, it is

presumed it does not have significant influence, unless

influence can be clearly demonstrated.

1-6

General Ownership Guidelines

Investor Ownership of the Investee’s Shares

Outstanding

Fair Value

0%

Consolidated Financial

Statements

Equity Method

20%

Usually lack

of control or

significant

influence.

50%

Significant influence

generally assumed

(20% to 50%

ownership).

100%

Financial statements

of all related

companies must be

consolidated.

1-7

LO 3

General Reporting Guidelines

Fair

Value

1. Investor

records

investment at

“cost”.

2. Investor

recognizes cash

dividends from

investee as

income.

Equity

Method

1: Same as Fair Value

2: Investor recognizes

its share (% of ownership) of investee’s net

income (net loss) as an

increase (decrease) in

the investment

account and dividends

as a decrease.

Consolidated

Financial

Statements

One set of financial

statements are

prepared to combine

accounts of the

investor and all of

its investees AS A

SINGLE ENTITY.

1-8

1-9

Special Procedures

for Special Situations

Reporting a

change to the

equity

method.

Reporting

investee

losses.

Reporting investee

income from sources

other than

continuing

operations.

Reporting the sale of

an equity investment.

1-9

1-10

LO 4

Excess of Cost Over Book Value

of Acquired Investment

When Cost > Book Value of an investment

acquired, the difference must be identified.

Assets may be undervalued because:

1.Fair values (FV) of some assets and liabilities on

investee’s books are different than book values (BV).

2.Investor is willing to pay extra expecting future

benefits to accrue from the investment.

3.Additional amount paid in excess of book value not

allocated to undervalued assets is attributed to an

intangible future value and recorded as Goodwill.

1-10

LO 5

Reporting Sale of Equity Investment

If part of an investment is sold during the period:

The equity method continues to be applied up to

the date of the transaction.

At the transaction date, the Investment account

balance is reduced by the percentage of shares sold.

If significant influence is lost, NO RETROACTIVE

ADJUSTMENT is recorded, but the equity method

is no longer applied.

1-11

1-12

LO 6

Unrealized Profits in Inventory

Sometimes affiliated companies sell or buy

inventory from each other in intra-entity

transactions that necessitate special

accounting procedures.

INVESTOR

Downstream

Sale

INVESTEE

INVESTOR

Upstream

Sale

INVESTEE

1-12

LO 7

Fair Value Reporting Option

In 2007, FASB introduced a fair-value option

An entity may irrevocably elect fair value as the

initial and subsequent measurement for certain

financial assets and financial liabilities including

investments accounted for under the equity method.

Under the fair-value option, changes in the fair value

of the elected financial items are included in

earnings.

1-13

Fair Value Option

Investment that

can otherwise be

accounted for

under the equity

method

Investment in nonmarketable equity

securities

After 2007, under the Fair-value Option,

changes in the fair value of these assets are

reported in earnings.

1-14