word file - six

MCB Internship Report

Introduction

Muslim Commercial Bank is one of the leading banks of Pakistan with a deposit base of about Rs. 280 billion and total assets of around Rs.300 billion.

Incorporated in 1947, MCB soon earned the reputation of a solid and conservative financial institution managed by expatriate executives. In 1974,

MCB was nationalized along with all other private sector banks. This led to deterioration in the quality of the Bank’s loan portfolio and service quality. Eventually, MCB was privatized in 1991.

During the last fifteen years, the Bank has concentrated on growth through improving service quality, investment in technology and people, utilizing its extensive branch network, developing a large and stable deposit base and managing its non-performing loans via improved risk management processes.

Vision Statement

To be the leading financial services provider, partnering with our customers for a more prosperous and secure future.

Mission Statement

We are a team of committed professionals, providing innovative and efficient financial solutions to create and nurture long-term relationships with our customers. In doing so, we ensure that our shareholders can invest in us with confidence.

Our Values

These are the standards and principles which determine our behavior and how we interact with our customers and each other:

1. Integrity

We are the trustees of public funds and serve our community with integrity.

We believe in being the best at always doing the right thing. We deliver on our responsibilities and commitments to our customers as well as our colleagues.

2. Respect

We respect our customer’s values, beliefs, culture and history. We value the equality of gender and diversity of experience and education that our employees bring with them. We create an environment where each individual is enabled to succeed.

3. Excellence

We take personal responsibility for our role as leaders in the pursuit of excellence. We are a performance driven, result oriented organization where merit is the only criterion for reward.

4. Customer Centricity

Our customers are at the heart of everything we do. We thrive on the challenge of understanding their needs and aspirations, both realized and unrealized. We make every effort to exceed customer expectations through superior services and solutions.

5. Innovation

We encourage and reward people who challenge the status quo and think beyond the boundaries of the conventional. Our teams work together for the smooth and efficient implementation of ideas and initiatives.

Departments of MCB

I did internship in Gulshan market branch which had the following departments. There was staff shortage hence a few persons were performing all duties. Therefore, there was overlapping of duties.

Organizational Structure of the MCB Branch

However there were following departments.

Ø Current Saving Department

Ø Accounts Department

Ø Remittance Department

Ø Clearing Department

Ø Cash Department

Ø Advances

Ø Customer Relation Department

Account Opening

Application Form

· The customer would like to open his account is required to meet with the manager or second officer, who will give him an “APPLICATION FORM.

Specimen Card

As I have already mentioned about “Signature Specimen Card”. This card contains two signatures of an applicant, applicant A/c no, A/c type, branch code, title of A/c, it will be attached with an application form. Banker uses this card at the time when he receives the cheque; he compares customer’s signature with the signature on the cheque for avoiding fraud.

Manager has every right not to accept this contract if he is not satisfied by the details provided by the customer.

Account Opening Register

· The manager records the necessary details into this register and allots an a/c number from this a/c opening register. This register is maintained for each type of account and the a/c numbers are allotted serially. After opening a saving and current accou nt every applicant’s data is entered into the computer to maintain a safe record and application form is properly filled so that it can be available when necessary.

Cheque Book

· Cheque book is issued to the customer when. the bank accepts the A/C opening application form and letter of thanks is received.

Types Of Customers

Individual

· Only one person can operate this a/c. We can call it a personnel or individual a/c.

· Followings are required to open it.

Ø Signature of customer on back of AOF.

Ø N.I.C photocopy attached

Ø Mention next of kin (nominee)

·

Joint

· In case of joint A/c, applicant mentions that how much person will operate the A/c. Instruction are given for joint A/c such that the account shall be operated by

Any one of us or survivor

· In first case if one of the a/c holders died then the other can operate the a/c individually.

Any two/All of us jointly

· In second case if one of the a/c holders died then the other partner can’t operate this a/c individually without having permission from the court.

· Requirements

Ø Sign of both customers on back of AOF

Ø Sign on joint A/C # mandate

Ø Name and A/C # of introducer

Ø NIC copies of both members.

Ø Mode of operation.

Partnership A/C

· For partnership a/c, along with the application form signature card.Other documents are also needed such as

Ø Partnership deed certified copy

Ø NIC photocopies of all partners.

Ø Partnership mandate for account signed by all the partners

Ø A letter duly signed by all the partners containing the operating instructions of the account also has to be taken.

· In case of addition or withdrawal of any partner a new agreement will be required.

Company Account

For company accounts following documents are required: -

Ø Copy of certificate of incorporation

Ø Memorandum of Association

Ø List of Director’s

Ø Copy of board resolution

Ø Certificate of Commencement of Business

Ø Copies of NIC of Director’s

Ø Company’s Balance Sheet

Letter of Thanks

Bank prepares ‘Letter Of Thanks’ for the new customer. This act promotes good will among the customer.

Pay

–In Slip

This slip is used for depositing the additional amount. The bank will accept the

Pakistanis notes. All cheques and other instruments should be crossed before they are deposited for credit into the account. There shall be no restriction on number of withdrawals in current account. An account holder wishing to close his account must surrender the unused cheques to the bank. The current account is computerized, thus it generate the statement of account for all account holders periodically. Incidental charges of Rs.50 are beard by the account holder if its credit balance is less than Rs.10000.

Closing of an Account

There are no. of reasons of closing an account. Some are listed below:

Ø If customer desires to close his account

Ø In case of death of one account holder

Ø Bankruptcy of the account holder

Ø If an account contain nil balance or not up to the requirement of rules.

Before closing any account, bank send letter to the account hold for informing him that his account is going to be closed. There is need an approval form higher authority to close any account.

Payment of Cheques

The first work that was assigned to me was Scrutiny of cheques. It is considered, as the simplest work in consumer banking operations, but actually it is not that simple. The cheques that are presented for either payment or for deposit are the main points where most of the frauds occur. There are few points to be noted while scrutinizing a cheque for payment or deposit,

Ø Date of the cheque

Ø Signatures of drawer

Ø Signature of Presenter

Ø Amount in figures and words

Ø Branch stamp

Ø Account number of the drawer

Ø Crossing in favor of any other person

The cheques which are presented for deposit in accounts of customers for them a pay-in-slip is to be filled in and the cheque is presented along with that slip. As the cheques are taken for deposit in customer’s account, a Cheques

Receipt Summary is prepared in which cheques are entered according to their category, i.e., Transfer Delivery, Clearance or Collection.

Call Deposit Receipts are also issued to the customers especially before the holy month of Ramzan. The reason is that customers convert their savings from saving account to the PLS account. The reason for this activity is that the customers want to take out there money from the accounts in order to skip the deduction of Zakat. For this purpose, CDR’s were issued having both applicant and beneficiary the same person.

CDRs are issued to the contractors favoring building departments in order to get tenders for various buildings.

Types of Accounts

Current Account

The current account is the most common account and the most preferred amongst business concerns. The theoretical explanation for this would be that they can function more efficiently but since in reality there are no restrictions on any with drawl the only reason we could think of is that current account facilitates online banking which saves time (which in this ultra competitive business world the most precious resource) to a considerable extent. In case of a current account the client does not earn any interest. Current account enables the client to do cash transactions in a more efficient manner.

Features

A sum of Rs. 10000/= in cash as initial deposit is required for opening a current account and the same may be maintained as minimum average running credit balance. No profit is paid on credit balances held in current accounts. The bank reserves the right to allow opening of current a/c at its description. All deposits and withdrawal from a current a/c takes place only at the branch where the account is being maintained. Current a/c cannot be overdrawn, except by prior agreed agreements with the bank. The correspondence relating to current A/Cs should be addressed to manager of the branch where the account is being maintained.

The account holder can draw sums from his account by means of cheque supplied to him by the bank for that particular account. Account holder should

take well care of the chequebooks issued to them.

Saving Account

Individuals who wish to earn profit/interest on their investment normally maintain the profit and loss sharing account but in order to earn interest the client is required to keep his/her deposits with the bank for some time. In theory there are some restrictions on withdrawal of money from a Profit and

Loss Sharing account but in general banking practice there is no restriction on any with drawl from a Profit and Loss Sharing account. The interest/profit is paid half yearly.

Profit and Loss Sharing Account

PLS saving account having a running minimum credit balance of RS.10000.

The bank would be within its rights to make investment of credit balances in the PLS saving accounts in any manner at its sole discretion and to make use of the fund to the best of its judgment in the banking business under the PLS system.

Profit/Loss

The profit/loss will be credited/debited on the basis of its net working results at the end of each half-year. Calculation of products on PLS saving A/c will be made for each calendar month on the lowest credit balance of an account between the close of business on the 6 th day and the last day of the month.

Rules for PLS

Ø Account holder can only withdraw sums from his account by means of cheques supplied to him by the bank for that particular account.

Ø Post dated and stale cheques willl not be paid.

Ø The bank reserve to itself the rights to close any account without previous notice any account which has not satisfactory account credit balance.

Ø If the account holder withdrawals the money under 7 days notice, the profit loss earning products will be computed on the monthly minimum balance.

Zakat is deducted every year on non-exempted accounts.

Saving 365 Gold

This account is newly developed of MCB and it provides flexibility of saving account to business people. Profit on deposits will be payable on daily product basis on balance of RS. 500,000/- and above. However, if balance in the account falls below RS. 500,000/- on any day, the product will be ignored.

There will be no restriction on withdrawal from the account. Zakat and withholding Tax is also applicable on the account opened under this scheme.

Ø Minimum balance is Rs.500,000/=

Ø Below minimum balance, profit calculation ignored

Ø Profit calculated on daily basis

Ø Profit paid on annually basis

Ø Zakat deducted on @ 2.5%

Ø The higher the balance, higher the rate is offered.

Ø Profit calculated on daily basis.

Ø Profit paid into your account every month

Term Deposits

Term deposits are fixation of certain amount of money for a specific span of time. The instrument term deposit is like a slip containing issuing bank name, a/c # to operate on computer, deal #, customer name, reference #, date of issue, amount, rate maturity date etc.

Accounts Department

Every transaction which takes place recorded in the computer so all transactions in different departments are forwarded to account department.

Since all vouchers from different departments are forwarded to accounts department so this department tallies all such transactions with current department after maintaining the ledger of each department. The branch where I worked Mr Azeem-ud-din Bukhari was performing these activities. I was not allowed to use software but I observed all the fuctions performed by him. Following are different functions performed by this department:

Ø Preparation of Financial Statements for different time span

Ø Maintain all accounts of different departments

Ø Calculation of profit on different schemes

Ø Calculation of markup on different advances

Ø Preparation Different types of reports for State Bank

Ø Daily position of cash & every accounts

Ø Matching daily summaries of all departments with ledger

As swift software is used therefore all these tasks have become quite simple just it requires posting and then all tasks can be performed by giving computer commands.

Remittances

The need of remittance is commonly felt in commercial life particularly and in every day life general. A major function of any banking system is the transfer of funds from one client or one place to another. By providing this service to the customer the bank earns a lot of income in the form of service charges.

This department deals with local currency remittance i.e. remittance from one city to another without actually carrying the currency. MCB uses following instrument for transferring of money:

Ø Demand Drafts (DD)

Ø Pay Order (PO)

Ø Telegraphic Transfer (TT)

Ø Mail Transfer (MT)

Demand Drafts (DD )

DD is a written order given by the branch of the bank on behalf of the customer to other branch of the same bank to pay the certain amount to the customer. DD are issued for the particular place other than place of issuance.

A drafts is a Cheque drawn by a bank on its own branch or any other branch of another bank at a different place requesting it to pay on demand a specified amount of money which is already received to the person named on it. DD is of following two types:

Ø DD payable

Ø DD Paid Suspense a/c

In the first type as advice reaches for payment the immediately pay to the customer while in later as DD presented by the customer, it is paid and the

suspense account is debited.

Documentation

A printed application form is provided for filling in completely and signing by the applicant. After depositing an amount of draft and commission of the bank, duly completed and signed by two authorized officers, then it is handed over the applicant and credit order is dispatched to drawer branch. Following are the pre-requisites for the processing of DD:

Ø Bank Serial No

Ø No. of DD

Ø Central No

Ø Test Key

Pay Order

For this kind of remittance the payer must have the account in the issuing bank. Pay order are more liquid as compared to cheques because cheques may be dishonored while PO can’t be. It is written order issued by the bank drawn and payable on itself. It is used for local transfer of money from one person to another person. It is also used by the public for depositing money with Government or Semi Government department.

DOCUMENTATION

The party who requires a pay order will get a printed application from the bank. He will fill it and deposits the amount and commission. The bank charges are same as on demand draft.

Ø Bank Serial No.

Ø No. of PO

Telegraphic Transfer (TT)

In this case the authority is given from one bank to other on the behalf of the customer through telecommunication to debit their inter office account through them and credit their parties account mentioned in TT. It is an inter bank transaction. Telegraphic transfer is an instant transfer of funds. Through this method applicant can transfer money from one place to another place. There are two types of TT, Both types of TT are maintained in separate registers, test is applied by the manager of every amount of TT.

Ø Incoming TT

Ø Outgoing TT

Applicant has to fill a form along with depositing amount to be transferred and bank commission. MCB charges the commission at the same rate as in the case of demand drafts.

Documentation

Ø Issuing Branch Name & Code

Ø Beneficiary Branch Name & Code

Ø No. of TT

Ø Amount in words & Figur

Ø Test key

Mail Transfer (Mt)

As the name shows, it is transfer of money in the shape of document through mail. Procedure is like TT. The transfer of funds from one place to another by mail is called Mail Transfer (MT). The MT can be foreign or domestic. The applicant who is desiring to remit the funds by way of Mail Transfer can either deposit cash or ask the bank to debit his/her account with the cost of MT including the bank charges. These all measures are for safe transfer of funds.

Documentation

Ø Issuing Branch Name & Code

Ø Beneficiary Branch Name & Code

Ø Number of MT

Ø Amount in words & Figure

Ø Test key

Clearing

All the external functions of clearing are carried by NIFT (National Institute of

Facilitation Technology) while the internal operations are performed by clearing department. It is just like any courier service which takes the cheques of other banks and delivers the cheques of that branch to it.

Clearing is a system by which banks exchange cheques and other negotiable instruments drawn on each other within a specified area and thereby securing the payment for its clients through the clearing house. A clearing house is a general organization of the banks at a given place, Its main purpose is offsetting the cross obligation in the form of cheques. When there are many banks in the country each will receive a number of cheques drawn on other banks, deposited within for collection. A clearing house is an organization where these cheques are brought and the mutual claims of each bank on the other are offset and a settlement is made by the payment of differences. The representatives off all the banks in Pakistan attend office of the bank which is performing these duties of clearing house, on each business day at a fixed time. They deliver cheques that their bank may have negotiated and receive in exchange cheques drawn on their bank negotiated by other bank. The responsibility of smooth cooperation of the clearing function lies with the State

Bank of Pakistan.

The operation of clearing refers to the collection of cheques drawn on other banks. These cheques may be drawn on UBL, HBL, NBP, or any other bank of Pakistan. The respective officer collects all cheques and enter them in clearing Register. Then he affix a stamps on these cheques and sorts out cheques of different banks and prepares schedule for them. These cheques are sent to clearing house. Exchange of cheques takes place through NIFT.

Further they settle their account. State Bank of Pakistan representative will work out the balances and will settle their account from their balances with

State Bank of Pakistan.

Advances

It is another major department of the branch. Bank provides this facility to the people who need advance money to meet their requirements. For getting the advances, the first step is the preparation of credit proposal. Some principles of lending are considered whenever financing being is made. These principles are:

Ø Character

Ø Capacity

Ø Collateral

Ø Capital

Ø Condition

Required Information

Ø An assessment of his business abilities

Ø Accurate & up-to-date financial statements

Ø Market reports about the borrower

Ø Party dealing with other banks

Ø Nature and structure of borrower business

Ø Names of proprietors, partners or Directors

Ø Detail of companies associated with borrower business

Ø Financial condition of borrower business

Preparation Of Credit Proposal

At first, a formal application for credit approval is obtained from the party along with complete group position. The parties credibility report is also obtained from the banks from which the party has been doing the business.

The party creditability report is also taken from the head office of Trade information Division.

For obtaining credit, party has to submit the last two years Balance Sheet and

Profit & Loss Statement duly attested but authorized auditors. If the party also involve in export or import business then the bank also consider the data of three years about imports and exports.

The Current and Debt equity ratio is also calculated by the bank.

Then recommendations are made the type of data required to prepare the credit proposal is to be gathered from different departments. Some data is obtained from the foreign exchange department. Some data is obtained from current account department and some data is available in Advance

Department. The purpose for which the financing is required should be explained very clearly. The securities offered by the party to the bank is also evaluated. In case of pledging of the property in shape of land or building the complete evaluation of the property should also be attached.

After all the requirements and necessary documents for applying for advances is fulfilled by the party then, the case is sent to the Chief Manager for approval. If the manager find any discrepancies, he may write on these documents. If the credit limit is in his range, he may approve the party for credit. If the amount is exceeding the Chief Manager send the case is forward to the Circle Office for approval and here the same procedure is repeated and if the credit amount is in the range of GM, he can approve and if the credit amount is very large from Circle Office, the case is then sent to Head Office and if it is a real big then is to be decided by Board of Director. MCB provides advances which are two types. These are two types of advances:

Ø Secured Advances

Ø Unsecured Advances

In secured advances, the bank takes any security against the loans while in case of unsecured advance no security is taken by the bank.

MCB divided the advances in to two major types:

Ø Fund Based

Ø Non Fund Based

In the fond base advances, the funds of MCB is involved and in Non Fund based only guarantee is given by the bank.

Fund Base Advance

MCB have following Fund base facilities of advance in its corporate branches.

The details of these types would be later. These are as follows:

Ø Demand Finance (DF)

Ø Cash Finance (CF)

Ø Running Finance (RF)

Demand Finance

This is a type of secured loan and demand loan never allowed without security. It is a type of long term financing. MCB also gives loan under the head of demand finance to individuals, industrial units commercial business etc.

Cash Finance

In this, the borrower gives a specific reason for the need of cash. MCB gives the facility of cash credit to business. The amount is passed through voucher and credit to the party account. Normally 0.60 paisa per thousand is charged on daily basis to customer.

Running Finance

These finances as evident by the name are given to the business to meet their daily needs. The mark up is charged on daily balances. This type of advances are given to trade, commerce and manufacturing for general purpose. Normally 0.60 paisa per thousand is charged is charged on daily basis. It is drawn through Cheque.

Letter of Credit

A letter of credit is a written instrument issued by a bank authorizing the seller to draw in accordance with certain terms and stipulating legal forms, that all such bills will be honored.

How a letter of credit is opened?

Ø Application for a letter of credit

Ø Line of credit

Ø Opening of the letter of credit

Ø Handling of the documents

Ø Payment by the importer to the bank

Ø Liability of the issuing bank

Application for a letter of credit

An importer prepares an application on the prescribed form available from the bank. The information which are supplied in the application are based on the contract of sale and include only the importer feature of contract such as the value of the merchandise, port of shipment, port of unloading, expiry date of the papers and brief description of the goods. If the bank is satisfied with the

applications, it will signed and acceptance agreement with the importer.

Line of credit

Before issuing a letter of credit, bank takes all necessary precautions for securing its credit. The bank first examines the customers credit standing, the type of goods to be imported, the market demand for the goods, the collateral offered to cover the credit. Then it establishes the amount i.e. the line of credit.

Opening of letter of credit

The letter of credit can be opened by mail or by cable. When it is opened by mail, the issuing bank sends letter of credit and to carbon copies to the importer. The importer then dispatches the letter of credit to the exporter in foreign country by mail. One carbon copy is kept for the record. The second carbon copy after signing is sent to the bank by the importer. If an importer directs the bank to open letter o f credit by cable, the importer’s bank sends a cable to the corresponding bank in the foreign country with a request to notify the exporter.

Handling of the documents

When the exporter receives a letter of credit, he presents the required documents and the draft to the bank in his own country after shipping of documents. If the bank is satisfied with the documents in the importing country and pays the exporter at official ratein the currency of his own country.

Payment by importer to the bank

When a bank approves the application of a customer for opening letter of credit, it does not lend money to the importer. The bank only lends the importer to use the credit standing of the bank to the exporter in the foreign country. The bank makes a contract with the importer that when the draft if send by the negotiating bank for payment the importer will make the payment to the bank not later then the day only the bank is to honour the obligation. In case of a sight letter of credit the payment to the corresponding bank is to be made on the day the draft and documents are received. When the time of letter of credit is used the importer is to arrange the payment not later than the day on which the draft is to mature.

Opening of Letter Of Credit In MCB

Ø Before opening of L/C certain requirements are necessary that are

Ø The applicant must has import registration number

Ø He must has account in that bank

Ø He must pledges his security against the L/C amount

Cash Department

In cash department both deposits and withdrawals go side by side. This department works under the accounts department and deals with cash deposits and payments. This department maintains the following sheets, books, ledger of account:

Ø Cash received voucher sheet.

Ø Cash paid voucher sheet.

Ø Paying-in-slip

Ø Cheque Book

Ø Cash balance book

Cash Paid Sheet

The only instrument that can be used to withdraw an amount from an account is the Cheque book. No payments are made by another instrument. Cheques can be of two types, they may be presented at the counter and encashed and the others are clearing or transfer cheques.

Cashier manually inspect the Cheque for following:

Ø Signature & date

Ø Cross cutting

Ø Drawee’s a/c title

Ø Amounts in words & figures

Ø Two signatures at the back

The cheques should not be stated as post dated. If in the Cheque there may discrepancy regarding any of the aspects described above the cheque is returned to the customer for rectification. On other hand if the cheque is valid in all respects, the cashier enters the necessary inputs in the computer and post the entry so that account balance is updated.

When cashier posts these entries, computer automatically display the balance before posting the transaction amount, balance after posting. The cashier easily and quickly see whether the amount being withdrawn so exceed the balance or within the balance. If the amount does exceed the balance then it is upon the discretion of the manager to allow an overdraft and not depending upon the customer’s reputation. If he does not allow an over draft, the procedure is repeated again as described for the mismatch of the signature

Cheque is return.

The detail of notes (currency) is written on the back side of the Cheque. The cashier at the same time maintain the “Cash Voucher Received Record

Sheet”. Then once again inspect the signature of the customer cancellation mark of checking officer and stamp of “POSTED” is placed on cheque before hand over the cash to customer.

Cash Received

For depositing the cash into customer’s accounts, there is need to fill in the paying-in-slip giving the related details of the transaction. This paying-in-slip contains the date, a/c/no, a/c title, particulars, amount being deposited and details of the cash. There are two portion of the paying-in-slip. The depositor signs the one part of the paying-in-slip one is retained by the bank to show an acceptance of the entries made in the slip.

The different colored paying-in-slip are used for all the types of deposits. Only the slips related to a particular type of a/c is acceptable by the bank. For example current paying-in-slip for current a/c and saving paying-in-slips for saving a/c etc. The paying-in-slip serves as a voucher to update to computerized transaction ledger. The transaction ledger is only updated by paying-in-slip and Cheque. The cashier responsible to receive both the paying-in-slip and cash from the depositor. The cashier check the necessary details provided I the paying-in-slip and accounts the cash and tallies with the

amount declared in the slip. If the amount does not tally with the cash given, the deposit is not entertained until the customer remove the discrepancy.

On the other hand if the two amounts tally, the cashier fills in the “Cash voucher received Record Sheet” and assigns a voucher no. to both the transaction being made in the sheet and the slip. This voucher no. starts with one and continue by serial increments of one for each day till the closing of the sheet, the cashier fills the voucher no, an account, cash day till the closing of the sheet. The cashier fills in the voucher no, an account of, cash entry in the related type of a/c and he post his initials on both part of the voucher.

Then the cashier send both to the accountant who verifies all the entries in the two documents, if the entries in the two documents, if the entries in the two documents tally with one another, the accountant authenticates the two by singing on the two documents and posting stamps on the slip. One part of the slip is then returned to the customer and other is given to the computer operator. A very important check is that the dates mentioned into the two documents must be the same.

The cashier posts the transaction entries in computer ledger. This ledger contains the a/c no, a/c title, voucher no, voucher date, transaction code, transaction amount. After posting these entries, computer display before posting balance and after posting. On every transaction computer generates an output of transaction ledger. He assigns the stamp

“ POSTED” on the voucher to show voucher transaction entries are posted. Checking officer receive this voucher and the compute output transaction ledge, he manually inspects the entries of ledger and voucher. If both are tallied, he then signs the ledger and put a mark of cancellation on the voucher. After the verifications from the checking officer, cashier receives the voucher.

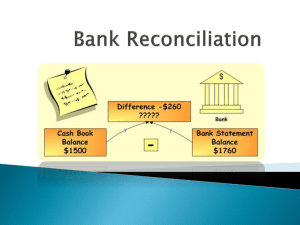

Cash Book Balance

At the end of the working day cashier is responsible to maintain the cash balance book. The cash book contain the date, opening balance, detail of cash payment and received in figures, closing balance, denomination of government notes (Currency). It s checked by manager. The consolidated figure of receipt and payment of cash is entered in the cash book and the closing balance of cash is drawn from that i.e.

Opening Balance of Cash + Receipts - Payments = Balance

The closing balance of today will be the opening balance of tomorrow. This department is one of the most important department of the bank. All the books maintained in this department are checked by office

Financial Results MCB

Title

EPS

Cash Dividend

Stock Dividend

(Bonus)

Right Issue

Book Value Per

Share

Growth

6%

Annual Annual

Annual

Dec-07

24.3

12.50

0%

88

Dec-06

22.2

7.5

15%

75

Dec-05

20.9

4.25

20%

55

Deposits per share

BalanceSheet

Advances

Investments

Total Assets

Deposits

Share Capital

Reserves &

Unapp. Profit

Equity

Surplus on revaluation -

Total

Profit & Loss

Mark-up / return / interest earned

Mark-up / return / interest expensed

Net mark-up / interest income

Provision against non-performing loans & adv.

Other

Provision/(reversal

)

Fee, commission 9%

Dividend income

Capital Gains

Administration expenses etc

Profit before taxation

Taxation

Profit after taxation

Ratios

Spread

Advances to

Deposits Ratio

ROE

ROA

23%

10%

20%

13%

74%

13%

-

15%

26%

39,131

45,414

9,706

55,120

31,787

465

218,961

113,089

410,486

292,098

6,283

7,866

23,921

2,960

106

3,879

632

1,500

5,559

-

21,308

6,042

15,265

12%

75%

38%

4.1%

471

198,239

63,486

342,108

257,462

5,463

30,193

35,657

5,188

40,844

25,778

4,525

21,253

1,015

168

3,574

812

606

6,561

351

18,501

6,358

12,142

12%

77%

45%

3.8%

538

180,323

69,481

298,777

229,345

4,265

13,618

17,883

5,424

23,307

17,756

2,781

14,975

(98)

480

867

6,566

13,018

4,096

8,922

10%

79%

65%

3.2%

Tax Rate

Assets

Deposits

Equity

Financial Analysis of MCB for 2007 results

28%

20%

13%

27%

MCB posted an after tax profit of Rs15.26b with earnings per share of Rs

24.30 in FY07 as compared to profit after tax of Rs12.14b with earnings per share of Rs 19.33 in FY06, depicting a significant growth of 26.0% in FY07.

Net interest income increased by 13% to Rs23.9b from Rs21.2b in FY06. The gross interest income grew by 23%, while the interest expense grew by 74%, depicting an increase in the cost of raising funds. The non-mark-up income increased by 20% to Rs 6 billion. The major contribution came from a 148% increase from the capital gained on sale of securities.

The asset base increased by 20% from 342 billion to 420 billion in 2007 as compared to 2006.Deposits showed a steady increase of 13% to bring the figure to Rs 292 billion as compared to Rs 257.4 billion in FY06. Advances increased by 10% to Rs218b, while the investments increased by 78% to Rs

113 billion.

Recent Results

34%

15%

12%

99%

MCB Bank Limited posted profit after tax of Rs4.1b with an earnings per share of Rs 6.55 in 1Q'08 vis-a-vis of Rs 3.7 billion with an earnings per share of Rs

5.93 in 1Q'07, depicting a growth of 10.3% during the period despite dismal performance of banking sector during 1Q'08.

Net interest income of the bank grew by just 2.5% during the period to Rs 6.1 billion as compared to Rs 6.0 billion in the corresponding period of last year.

High cost of deposits was the main reason behind.

Swot Analysis

STRENGTHS

The strengths of MCB are as:

Ø MCB is the first Pakistani privatized bank and because of its quality management, marketing, innovation in products and services is performing well in financial market.

Ø Has established a good reputation in the banking market

Ø Strict adherence with the banking procedures requirements, SBP’s prudential regulation requirements and its SROs and international banking requirement as well as to its own set policies

Ø Strong and its attractive products

Ø Better focus on customer services and customization

Ø Flexibility with the changing environment

Ø Induction of the highly qualified professionals to change overall set up

Weaknesses

Ø The noted weaknesses of MCB are as:

Ø The majority of people are not well aware about the products of MCB.

31%

15%

4%

90%

Ø Therefore it should advertise extensively especially RTC and Master Cards.

Ø A behavior has been noted that bank tries to feel at ease with good looking, rich and educated people and the poor looking customers feel some bit strange in the environment of the bank. The bank employees should try to accommodate behaviorally all type of customers.

Ø In MCB there is lack of specialized skill because of job rotation policy of human resource department. The bank should concentrate upon increasing its abilities on individual service basis.

Ø Mismanagement of time is another big mistake in MCB branches, the bank official time of closing is 5:30pm but due mismanaging of time allocation and work the staff is normally on their seats till 7:00 or 8:00 clock.

Ø Process of development is bit slow due to its conservative approach

Ø Never prefer to be a leader and prefer to be a follower of others

Ø Slow improvement and acceptance of technological changes

Ø More emphasis on deposit accumulation and less on their mobilization

Opportunities

Ø Greater potential and opportunities for Credit Division if Liberal Policies being adopted.

Ø Can grab more market share for its RTCs, remittances and forex department through effective promotional and liberal policies.

Ø Inclusion of highly qualified professional can change the whole scenario and position of the bank if they have given the due liberty in performing their duties.

Ø Adoption of information technology will improve the customer services.

Ø More mobilization of accumulated deposit is possible through innovative financing to

· Agro Based Sector

· Leasing

· Personalized Financing

Threats

Ø Change in government policies has affected the banking business. Still banks have to wait to get permission of state bank. The freezing of foreign currency accounts is a vital example of letting people not to trust on banks.

Ø The Competition has become severe by the entrants of so many banks, So to exist one will have to prove himself in its services through excellent management and will have to satisfy its shareholders. Otherwise he will be out the market.

Ø Employees unions have been allowed if not managed properly can affect performance.

Ø The decrease purchasing power of consumer in the current economic situation of the country affecting the business activity speed too much and the result is the low investment from the investors in new projects can create problem for the bank because it is working a lot in trade.

Ø Introduction of credit marketing by local and foreign banks is badly affecting the mobilization of the MCB’s deposits due to the non presence of such department in it.

Ø Introduction and adoption of information technology as well as promotion of the computer culture by the local as well as foreign banks will definitely affect the services and business of the MCB.

Pest Analysis

Poitical

§ Employment practices are expected to change.

§ Unions, Associations are being allowed to work effectively which can affect the performance of the company both positively or negatively.

§ Political interference regarding policies is expected to increase as current government is in race of power gain.

§ Due to lack of confidence on government investor is reluctant so mobilization of funds is going to decrease.

Economic

§ Inflation is very high which will decrease the demand as purchasing power is decreasing.

§ Staff cost is increasing as basic wage rate has increased and inflation has compelled to will compel to increase salaries.

§ Operating costs are increasing due to inflation.

§ Interest rate is increasing so loan taking has decrerased.

§ Value of rupee is decreasing which is pressurizing the economy.

Social And Cultural

§ Lack of experts is in our country regarding management hence innovative activities are slow and conventional methods are adopted.

§ Cultural strain to savings is the reason due to which investment remains low

.

§ Declining work ethics is also our problem which is mainly due to poverty, lack of training.

§ Inadequate Accountability ,lack of good governance and lack of good infrastructure helps creditor to cheat and heavy bad debts occur. Same situation is hoped to prevail.

§ Inadequate Empowerment is also a usual problem in our organization as every person want to get more power hence there is less delegation of authority and decision making.

Technical

§ MCB has computerized its most of the branches but still some are manual there is need to computerized otherwise customers will get bad image.

§ Now a days computerized system is used by banks whis is very effective.

But MCB will have to improve its computerized technology as some fake transactions occur by ATM.

§ Shortage of electricity is a big problem,

§ Employees of each organization need IT training and organization has this trend. MCB will have to follow it.

Recommendations and Suggestion

From the quantum of the profit and its financial data it can easily judged the after privatization Muslim Commercial Bank is performing well. Its deposits

are growing day-by-day and so its profitability. The controlling body is responsible for the productive performance of the bank.Following are my observations and suggestion to improve the efficiency for the development of the bank.

Increase In Profits

People can be motivated to save money by offering the deposit through various investment schemes. The rate of profit should increase 1% or 2 % it would be profitable step for bank.

Increase Salaries

MCB is making good profits but giving less pay to their employees as compared to their competitors. So their salaries should be increased.

Change The Nature Of Work

Most of the bank employees are sticking to one seat only with the result that they become master of one particular job and loose their grip on other banking operation. In my opinion all the employees should have regular job experience all out-look towards banking. Their promotion policy should be adjusted accordingly.

Training

Every year some of the employees should be sent for training to other countries and employees from other branches should be brought here. Some more reading material should be provided the purpose should be to educate the employees with the advance studies in their field. The employee should be provided the opportunities to attend and participate in seminars and lectures on banking.

Incentive To Employees

Bank should give some more incentive to its employees in order to remove the conflict between lower and higher officers and should try to improve the working condition of the bank. Such system should be designed that every employee who has some problems with his officers can communicate to the higher management and some steps must be taken to improve that.

Performance And Reward

Smart, educated, skilled, well spoken and well versed staff personals should be rewarded and appreciated, while on the other hand lazy, lethargic, heard, rough-dealers and ill mannered must be warned and penalized but this all should be on merit and considering the policy of honesty is the best policy and not due to some personal liking, disliking prejudice and patrimonial. It is therefore suggested certain schemes and checks may be introduced in banks to increase efficiency through reward and punishment system.

Over Employed

During my internship period I felt that at some place the Muslim Commercial

Bank Limited is over employed which is causing in expenditure. I think that the best way out for this problem is to pen new branches.

Promotion And Advertising

Bank must let potential customers know that all attractions for banking exist.

This is done by advertising on television and obtaining press coverage, in conjunction with direct mail, window displays, leaflet in branches and in appropriate other locations (such as hotels, shops, etc.) and including leaflets in statement of accounts sent to existing customers in the hope that they will tell potential customers about the services provided by our bank.

More Focus on Salary Accounts

A logic leads to promotional campaign through employers who are customers of the banks and their employees are paid in cash. Such business accounts should be encouraged to open the accounts of their employees with the banks. It might be worth offering free banking for a specific period to new accounts or simply publicizing the services available by means of posters at the employer’s premises.

Internship Facilities

The period of internship should be divided in to the number of department of the Muslim Commercial Bank Ltd. The internee should be given timetable mentioning the number of days he has to work at different places in the bank.

On the first 4 days in each department internee should be given a lecture the officer of the department concerned about working of the department.

What Were My Duties and What I Learned

§ In first weak I assisted Mr Mahboob in Scrutiny of cheques. It is considered, as the simplest work in consumer banking operations, but actually it is not that simple. The cheques that are presented for either payment or for deposit are the main points where most of the frauds occur.

§ I learned whole process of account opening of individuals practically. I remained involved very much in practical activities of account opening as Miss

Uzma whose duty was account opening would remain very busy as number of customers coming for account opening and getting information was high. So I assisted her.

§ I haven’t issued any cheque book personally, but the procedure is very simple for issuance. I observed the process.

§ I filled many applications form for remittances. I prepared remittance slips and learned to apply tests on TT and MT.

§ I processed the Inward cheques for collection and clearance, and have also prepared vouchers.

§ Every transaction which takes place recorded in the computer so all transactions in different departments are forwarded to account department.

The branch where I worked Mr Azeem-ud-din Bukhari was performing these activities. I was not allowed to use software but I observed all the fuctions performed by him.

§ Miss Maria was credit officer who explained me the procedure of advances.

Mostly work is done through computer. I was not able to perform activities by myself as access to software is not allowed. I observed how the application is processed. I think it sufficient to know the procedure.

§ In cash department I observed the process of deposits, filled deposit slips, and learned how the cash registers are maintained. In this department I did little work practically as it was not allowed.

§ During my internship I dealt with many customers and employees, this was a great experience to learn

- how to deal with customers

- how to work under pressure i.e in rush hours.

- how to manage an office.

- My communication skills were improved.

- I observed some signs of mismanagement which I think can be removed if branch manager take more responsibility.

- I observed the practical application of many accounting concepts.