Training

advertisement

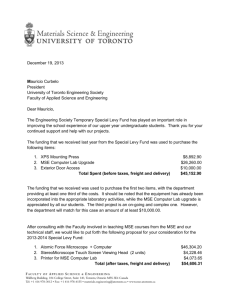

Building up capacities for successful lending to Micro, Small and Medium-sized Businesses Workshop on SME Financing Dar es Salaam - June 26, 2007 Project locations Shareholder Structure of ProCredit Holding ProCredit Holding aims to expand the “frontier of finance”, i.e. to extend downward the range of market segments served by formal and commercial financial institutions. Capital base: Voting capital EUR 152 million Non-voting capital EUR 28 million Share premium EUR 36 million Retained earnings / other reserves EUR 12 million Total EUR 228 million 84 % 16 % Shareholder structure of voting capital: 21 % 18 % 5% 14 % 18 % 7% 3% 7% 1% 3% 1% Omidyar Tufts 2% TIAA-CREF and the Omidyar Tufts Microfinance Fund have invested EUR 40 mln in non-voting preference shares. Overview of performance, all PCH group institutions April 2007 Outstanding loan portfolio: Breakdown into loan size categories 2000-2007 Number of loans in `000 Volume in EUR million Medium loans: Small loans: Micro loans: Micro micro loans: Medium loans: Small loans: Micro loans: Micro micro loans: Return on equity: the PCH group worldwide ProCredit Bank Examples in Africa: Loan portfolio outstanding Volume in USD million ProCredit Bank Examples in Africa: Number of loans outstanding (Business and housing improvement) Number of loans ProCredit Bank Examples in Africa: Number of loans disbursed per loan officer Number of loans Support for MSE lending to commercial bank Project design (“Downscaling”) International Financial Institution Provision of long term credit lines for on lending to MSE Donor (USAID/EU) funded technical assistance, co-financed by partner banks Technical assistance provider Consulting, training and implementation -> Capacity building for MSE lending -> Active support to achieve tangible results Partner Bank (sample) Micro Loans Small Loans Medium Loans Agricultural Loans Typical terms of reference / project objectives • Modular and on-the-job training of MSE loan officers, supervisors, trainers, managers and back officers • Ongoing supervision of MSE lending activities on a branch level assuming an active and operational management approach, • Implementation of a MSE loan processing system including MIS, • Building up a MSE lending head office unit, • Designing and implementing internal control procedures, • Training of auditors, • Managing interfaces within the bank with the aim to embed MSE lending smoothly into the bank’s operations, • Exiting (“Graduating”) the partner banks (branch, than region, than bank altogether) ensuring that the bank conducts and expands sustainable MSE lending without the Consultant’s input. • Represent EBRD/KfW (Apex) interest as creditor IPC business support IPC Consultants do not limit their input to training and advise. In fact, IPC takes active participation in all steps of loan processing and interferes where necessary. Partner Banks therefore beyond pure consultancy receive active business support. We believe that only in this way, and by entering into a constructive dialogue with the partner bank’s management, change can be firmly implemented and tangible results be achieved . Involved: Measures: Involved: In case of timely repayment: - Loan Officers - Contact clients; - Back Office retain clients Measures: - Senior Loan Officers - Head Office + Branch Management - Marketing Dept. In case of delayed repayment additionally: - Analyse client needs and feedback - Exchange experience with other projects and banks - Branch Management - Visit clients - Legal + other depts. - Possible legal action Repayment / Recovery Involved: - Loan Officers Back Office Senior LOs Branch Mgmt. Involved: Measures: - Regular visits - Check repayment information Involved: - Back Office - Front Office Product design Measures: - Prepare contracts Check documents Advise clients Witness signatures Monitoring Client Acquisition Involved: Disbursement / Internal Control Decision Application Involved: Measures: Measures: - Direct promotion - Advertising in local mass media Measures: - Loan Officers - Advise - other bank staff clients Analysis Involved: - Credit Committee - Assess plausibility of - Loan Officers information and debt capacity - Take loan decision - Set terms + conditions - Loan Officers - Marketing Dept. - other bank staff Measures: - Loan Officers - Visit client’s premises - Assess real creditworthiness - Prepare case for Credit Committee Credit Policy and Technology • Lending policy adapted to local market conditions for micro and small enterprises • Goal to make partner bank the client’s core bank with majority share in the companies banking business • Main principles of lending activities: – profitability, liquidity, independence of political, religious and other non-economic factors – Risk diversification – Only financially sound companies with trustworthy management – Clients need to fulfil a set of ethical and environmental criteria – Portfolio mix: maintain diversified portfolio • Credit decision based on the ability and willingness of borrower to repay, i.e. cashflow is of greater importance than asset value • Combination of qualitative and quantitative analysis by the credit officer is of great importance • Final decision is always made by unanimous vote of the credit committee MSE lending staff: recruitment and training Recruitment: • • • • Selection of staff conducted jointly by the consultants and the partner bank Staff is recruited both internally and externally according to the same process and procedures Staff selection process consists of several phases, including pre-selection based on applications and CV, group sessions, written tests and individual interviews MSE full-time credit staff consist of: – Branch level: loan officers, back office staff, MSE credit supervisors – Head Office Level: MSE credit management, regional managers, back office staff Training in MSE credit operations is ongoing and provided both in classroom sessions and on-the-job to support partner banks to build up in-house training capacities for: • Loan officers, senior loan officers • Lower management: MSE credit supervisors, Regional Managers • Middle management: MSE credit management, branch managers, other ancillary departments (Marketing, HR, Internal Audit) • Senior management Development of MSE loan portfolios IPC supported commercial banks typically manage to develop their MSE loan portfolios dynamically, achieving significant growth. Average monthly net growth 2004: USD 20 Mio. 2005: USD 40 Mio. 2006: USD 70 Mio. With 14,000 to 20,000 new additional MSE loans (net, by number) every quarter, IPC managed advisory projects significantly impact on the client structure of partner banks. This induces significant changes in the way these banks develop their business, formulate strategies and position themselves. Other Key Achievements • Arrears (>30 days) are at all times low (<2%), across all partner banks and project countries • More than 10,000 loan officers have been trained; roughly 4,600 currently process MSE loans in the partner banks • Significant regional outreach: MSE credit departments for over 40 partner banks have been created in 950 branches in 470 towns and cities across the region • Close to 70% of all loans outstanding are for an amount below USD 10,000 • Only 16-20% of the portfolio is financed by IFI funds. The majority of the funding has been mobilized by domestic banks on their markets (exception: Kyrgyzstan and Armenia) Downscaling: The China Example China Development Bank Microfinance Project (CMFP) Framework: • Technical assistance and credit funds provided to the China Development Bank by the World Bank and Kreditanstalt fuer Wiederaufbau (KfW) • China Development Bank provides credit lines and finances technical assistance to selected partner banks (PB) • IPC provides technical assistance to partner banks: capacity building, institution building, and training • Partner banks develop sustainable MSE credit operations Objectives • Provide ongoing access to finance for micro and small enterprises (MSE) • Implement sustainable micro credit activities at participating partner banks • Strengthen the financial sector • Achieve wide regional coverage Financing MSE The Target Group: – Micro and small enterprises cannot supply formal financial data, or only unreliable data – Need for alternative forms of collateral – Need for quick and simple loan processing – Demand for permanent access to credit – Need to establish relationships between an informal sector and formal commercial banks Technology to provide financial services to MSE: – Providing accessible products, attractive to the target group – Low transaction costs, efficient procedures, cost covering interest rates – Analysis of whole economic unit – Strict monitoring ensures low arrears rates – Sanctions, moral hazard, prospect of ongoing access to finance Phases of Institution Building at a Partner Bank Monitoring Graduation Expansion Implemention Preparation Project month 1-3 3-6 - Select and begin training of initial MSE credit staff - Establish MSE credit department at selected pilot branches - Conduct market survey: clients, competition - Product design - Draft MSE credit policy and procedures - Draft organisational structures for MSE lending – Head office and branch level - Establish credit committee - Begin lending operations 6-9 - Build up in-house training capacities - Streamline efficient procedures and operations - Develop MSE credit management staff for head office - Delegate credit approval authority to branch level - Expand marketing activities - Establish additional MSE credit departments - increase lending activities 9-12 … - Ensure appropriate internal control - Ensure quality training and HR development - Ensure continuous development of high quality MSE credit portfolio - Establish internal capacity for MSE internal audit - Ensure effective MSE credit management - Fully handover management and further development of MSE credit operations to PB - Monitor sound development of MSE credit operations Institution Building at Partner Banks Support PB to establish MSE finance as new business line within existing structures: – Train and develop MSE credit staff (on-the-job, classroom) – Implement MSE credit technology and procedures – Establish pilot micro credit departments – Delegate credit approval authority to lower management level – Develop and ensure adequate internal control on the branch level – Ensure strong, effective coordination, support and monitoring by Head Office – Ensure effective cooperation and integration with ancillary departments (e.g. HR, Marketing, Audit) – Change the “mindset” of the PFI (HR/Credit policy, internal control, marketing…) Standardised MSE Loan Products Loan Product Express Loan Micro Loan Small Loan Type of Business Sole proprietors Sole proprietors Legal entities, sole proprietors Business sector Trade and services Trade, services, production Production, services, trade Loan amount (equiv.) Up to EUR 5,000 EUR 5,000 – 10,000 EUR 10,000 – 50,000 Term Max. 18 months Max. 24 months Max. 36 months Security Only personal guarantor Limited: equipment, goods, personal property Some: any commercial /private assets Loan purpose Working capital Working capital, small investments Fixed assets, working capital for production Pricing Market rate Market rate Market rate Loan Processing time Within 24 hours 1-3 days 3-5 days Building HR capacities for MSE credit operations Development of MSE Credit Staff CMFP Regional Outreach CMFP Monthly Loan Disbursements Vol. (EUR ‘000) No. CMFP Monthly Portfolio Development Vol. (EUR ‘000) No. CMFP Portfolio Development Outstanding Number of Loans: By Loan Size (EUR) No. Outstanding Volume of Loans: By Loan Size (EUR) Vol. (EUR ‘000) Achievements of CMFP Pilot Phase (May 2007) Credit technology adapted to Chinese environment and standardised PB willingness to accept the target group and the proposed credit technology High quality MSE credit portfolio development Pilot PB have achieved profitability PB implement required institution building measures PB recognize and gradually develop MSE lending as a key strategic priority MSE credit staff trained; key focus on training and building up managers and “trainers” Base of consultants trained: initial implementation at PB at faster pace Outlook for CMFP in 2007 Graduation of pilot PB: – – – – – Full handover of responsibilities to HO MSE credit management department Handover of basic training activities for MSE credit staff Ensure continued development of quality credit decisions/portfolio/credit staff Improve audit system for MSE credit activities Establish effective monitoring mechanism Continuous standardisation of procedures and documentation increase efficiency of CMFP implementation at PB by use institution building measures at existing PB as basis for new PB: – – – – Organisational structures Procedures, guidelines and manuals Training capacities for LO, HO MSE credit staff, senior management Marketing methods Increase number of PB and regions covered to 12 Ongoing training of all CMFP PB staff Monitoring PB graduated from TA Launching activities at additional 6 new PB Prepare for roll-out phase: reach out to 130,000 MSE in China by implementing project cooperation at 69 partner financial institutions