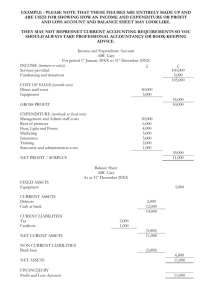

explanatory foreword - Brecon Beacons National Park Authority

advertisement