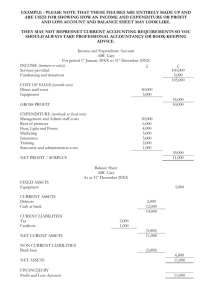

Statement of Accounts 2012/13

advertisement