Define economics

advertisement

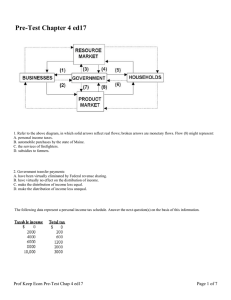

Define economics The study of how people seek to satisfy their needs and wants by making choices Explain how scarcity relates to economics Scarcity is that there are limited quantities of resources to meet unlimited wants What is opportunity costs? The most desirable alternative given up as the result of a decision What are trade offs An alternative that is sacrificed when a decision is made Define factors of production Resources that are used to make all goods and services What are the three factors of production? Land, labor, & capital Define consumer sovereignty Is the power of consumers to decide what gets produced What is self interest? Means that buyers and sellers are focused on personal gain What is competition? The struggle among producers for the dollars of consumers What is incentive? For consumers is the hope of reward or the fear of punishment that encourages people to behave in a certain way; incentives for business is selling more goods for more profit What is laissez faire? The doctrine that states the government generally should not intervene in the marketplace What is consumer sovereignty? Is that consumers decide what gets produced because businesses want to meet the consumers desires What are the five features of a market economy? (capitalism) 1. Self interest 2. Competition 3. Incentive 4. Laissez faire 5. Consumer sovereignty What are the benefits of a market economy? Incentives to produce, Greater efficiency Private ownership & innovation What are the costs of a market economy? More varied income, Unemployment Poverty/homelessness, wealth gap Describe Adam Smith Believed that in each transaction, the buyer and seller consider their self interest or personal gain Describe Karl Marx Believed that human labor was the source of all added value but keeps it as profit or exploiting the workers Describe John Maynard Keynes Believed that government intervention may be needed in crisis situations to pull the economy out of depression (pump money into the economy) What is sole proprietorship? A business owned and managed by a singled individual What is a partnership? Owned by two or more persons who agree on specific responsibilities What is a corporation? Owned by individual stockholders and run by a board of directors What is the role of stockholders in financing corporations? Stockholders must invest money to buy shares to finance and to part of the corporation. They are considered the owners What is the role of government in regulation corporations? To make sure the corporations follow the regulations they set such as filing quarterly and annual reports to the SEC and taxation Define the law of demand Consumers buy more of a good when its price decreases and less when it increases Define the law of supply The tendency of suppliers to offer more of a good at a higher price Describe perfect competition Is when a large number of firms all produce the same product Describe monopoly A system that is dominated by a single seller Describe monopolistic competition When many companies sell products that are similar but not identical Describe oligopoly Is when a fes large firms dominate a market Define elasticity of demand Is a measure of how consumers react to a change in price Define elastic demand Very sensitive to change in price Ex: the demand for a particular brand Define inelastic demand Not sensitive to change in price Ex: goods with no substituteswater, gas, utilities Define unitary demand Is a demand whose elasticity is equal to 1 Ex: equilibrium Define price floor A government- or group-imposed limit on how low a price can be charged for a product. For a price floor to be effective, it must be greater than the equilibrium price What is price ceiling? It’s a government-imposed limit on the price charged for a product What is total cost? Fixed costs plus variable costs Ex: materials and labor Define fixed cost Is a cost that does not change Ex: rent mortgage Define variable cost May rise of fall depending on the quantity produced Ex: raw materials Define marginal cost It is the cost of producing one more unity of a good Ex: hiring a new worker What is the golden rule of profit maximization? Occurs at a point where marginal costs equals marginal revenue. Thus, the optimal level of production occurs where marginal revenue equals marginal costs, the point of maximum profit as dictated by the golden rule