Chapter 8

RECORDING ADJUSTING AND

CLOSING ENTRIES FOR A SERVICE BUSINESS

Key terms

• accounting cycle: the series of accounting activities included in

recording financial information for a fiscal period

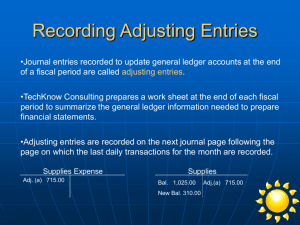

• adjusting entries: journal entries recorded to update general

ledger accounts at the end of a fiscal period

• closing entries: journal entries used to prepare temporary

accounts for a new fiscal period

Key terms

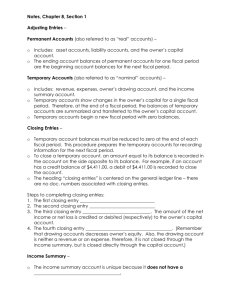

• permanent accounts: accounts used to accumulate information

from one fiscal period to the next

• post-closing trial balance: a trial balance prepared after the

closing entries are posted

• temporary accounts: accounts used to accumulate information

until it is transferred to the owner’s capital account

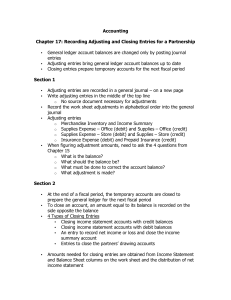

Identifying Financial Statement Procedures:

• Income summary is a temporary account.

• Temporary accounts begin each new fiscal period with a zero

balance.

• The journal entry to close Income Summary when there is a net

income is debit Income Summary; credit owner’s capital.

• Accounts used to accumulate information from one fiscal period to

the next are permanent accounts.

Identifying Financial Statement Procedures:

• The journal entry to adjust Supplies is debit Supplies Expense;

credit Supplies.

• When the total expenses are greater then the total revenue, the

income summary account has a debit balance.

• Accounting Period Cycle concept applies when a work sheet is

prepared at the end of each fiscal cycle to summarize the general

ledger information needed to prepare financial statements.

• After the closing entries are posted, the owner’s capital account

balance should be the same as shown on the balance sheet for

the fiscal period.

Identifying Accounting Concepts

and Procedures:

• A source document is prepared for adjusting entries FALSE

• The income summary account has a normal debit balance

FALSE

• The drawing account is a permanent account FALSE (temp)

• Temporary accounts must start each fiscal period with a zero

balance TRUE

Identifying Accounting Concepts

and Procedures:

• A post-closing trial balance verifies the equality of debits and

credits in a general ledger after the closing entries are posted

TRUE

• Journal entries used to prepare temporary accounts for a new

fiscal period are closing entries TRUE

• The balances of the expense accounts must be reduced to zero to

prepare the accounts for the next fiscal period TRUE

• To close a temporary account, an amount equal to its balance is

recorded in the amount on the side opposite to its balance TRUE

0

0