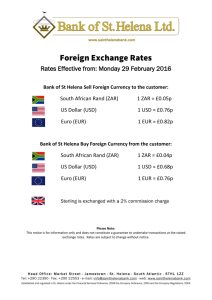

Exchange rates

advertisement

Convergence in Interest and Exchange Rates Oxana Babetskaia-Kukharchuk Sekce měnová a statistiky ČNB Odbor vnějších ekonomických vztahů Seminář odboru 31 – Finanční politiky, MF Aktuální Otázky Makroekonomického Vývoje ČR- Zkušenosti Po Vstupu Do EU 6. Prosince 2005 Outline • Motivation • Convergence in exchange rates • Interest rates convergence Data and methodology Results • Conclusion 2 Motivation • How narrow are CE-4 interest rate differential with Euro area? • How close are CE-4 currencies de facto to Euro? 3 Interest rates Data • 1 year: Bloomberg, Dec.1998-Sep.2005, daily Euro Area Interbank Offered Rate (EURIBOR), the Prague Interbank Offered Rate (PRIBOR), the Budapest Interbank Offered Rate (BUBOR), the Warsaw Interbank Offer/Bid Rate (WIBO) and the Bratislava Interbank Offered Rate (BRIBOR) • 5 years: Bloomberg, Dec.1998-Sep.2005, daily Government bonds • 10 years: Eurostat. Jan.1990-Aug.2005, monthly EMU convergence criterion bond yields 4 Differences in interest rates vis-à-vis the euro area 1998–2005 (percentage points) One-year rates Five-year rates 14 14 12 12 10 10 8 8 6 6 4 4 2 2 0 0 -2 1998 1999 2000 CZ 2001 HU 2002 2003 PL 2004 SK Sources: Bloomberg, CNB calculation. -2 1998 1999 CZ 2000 2001 HU 2002 2003 PL 2004 SK 5 EMU convergence criterion bond yields 18 AT GR 14 PT CZ 12 HU PL 10 SK 16 8 6 4 2 0 -2 -4 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 Sources: Eurostat, CNB calculation. 6 Exchange rates Stylized facts: Euro and Dollar exchange rates in CE-4 (weekly, 1st week 2003=100) 130 110 120 100 110 100 90 90 80 70 1/08/03 CZK/EUR PLN/EUR SKK/EUR HUF/EUR EUR/USD 80 12/24/03 12/08/04 70 1/08/03 CZK/USD PLN/USD SKK/USD HUF/USD EUR/USD 12/24/03 12/08/04 7 Formal analysis of exchange rate co-movements • Data: Bloomberg, 01/01/1994 – 30/08/2005, Daily • Methodology: time varying correlation coefficient (estimated as bi-variate GARCH) corr cov NC / USD, EUR / USDt var NC / USDt * var EUR / USDt where NC = national currency • Possible outcomes: 0 <= |corr| <= 1 corr = 0: NC is not related to Euro at all corr = 1: NC = Euro 8 Results: Dynamic correlations Sources: Bloomberg, CNB calculation. 2002 2003 2004 2005 2002 2003 2004 2005 2001 2000 1998 1999 2001 2000 1999 -0.4 1998 -0.4 1997 -0.2 1996 -0.2 2005 0 2004 0 2003 0.2 2002 0.2 2001 0.4 2000 0.4 1999 0.6 1998 0.6 1997 0.8 1996 0.8 1995 1 1994 1 1995 SKK/USD and EUR/USD 1994 PLZ/USD and EUR/USD 1997 -0.4 1996 -0.4 1994 -0.2 2005 -0.2 2004 0 2003 0 2002 0.2 2001 0.2 2000 0.4 1999 0.4 1998 0.6 1997 0.6 1996 0.8 1995 0.8 1994 1 1995 HUF/USD and EUR/USD CZK/USD and EUR/USD 1 9 Conclusions Interest Rates • Czech Republic and Slovak Republic have the lowest interest rates differential • Current average level in CE-4 is comparable to the timecorresponding level in Portugal Exchange Rates • Czech and Slovak koruna have a higher and less volatile correlation with the euro • CE-4 currencies tend to be perceived close to Euro and similar among themselves • Factors which may explain converge: - Euro as the mean of trade invoicing - implicit role of Euro as the reference currency - intraregional trade <Europe: 70-80%> 10 Thank you for your attention ! 11