File

advertisement

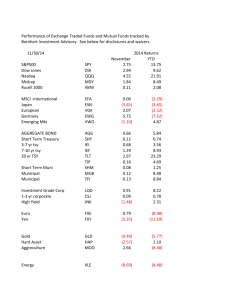

Lazard Ltd (NYSE: LAZ) Closing Price on 12/7: 25.31 DCF Upside: 24.9% Lazard Ltd • • • • Founded in 1848 Initial Public Offering: May 2005 2,452 employees Offices located in 26 countries, 41 cities Lazard Ltd • Financial Advisory and Asset Management Firm – Asset Management revenue is stable fee-based revenue – Mergers and Acquisitions revenue for volatile with changes economic activity • Leads Industry in Strategic Restructuring • Assets under management total: 135.8B – Increase of 20% in 2010 • Financial Advising to corporations, banks, and high net-worth individuals Financial Strength • Favorable low-risk balance sheet: – $1 Billion cash & cash equivalents on hand – No scheduled long term debt maturities before may of 2015 • Quick Ratio: 1.3 • Long term debt – Equity: 1.76 Revenue • 2 main streams of Revenue • Financial Advisory Services & Asset Management • Strong network of clients (70 countries) Revenue Advisory Asset Management Financial Advisory Revenue Revenue ($bn) $1.80 $1.60 $1.40 $1.20 $1.00 $0.80 $0.60 $0.40 $0.20 $- JP Morgan Morgan Stanley Bank of America Lazard UBS Citigroup Duetsche Bank Restructuring Business 100% $1,241 $1,024 $990 $1,121 $1,083 90% 80% 70% 60% 50% Restructuring 40% Advisory 30% 20% 10% 0% 2007 2008 2009 2010 LTM Key Financial Ratios vs Competitors Ratio LAZ GS EVR Industry Sector S&P 500 P/E 12.84 16.49 70.37 27.10 21.02 15.59 1 yr Revenue Growth 22% -11% 19.07% 19% 19% --- ROA (5-year AVG) 3.83% NA .86% .37% 1.35% 6.54% ROE (5-year AVG) 44% NA 4.01% .11% 9.50% 21.24% Total Debt/Equity 139.25 NA NA 391.42 182.14 137.97 5-Year Price Chart Dividend LAZ Quarterly Dividend 0.70% 0.60% 0.58% 0.50% 0.40% 0.34% 0.32% 0.30% 0.20% Dividend % 0.32% 0.19% 0.10% 0.00% Nov '07 Nov '08 Nov '09 Nov '10 Nov '11 Analyst Coverage 1-5 Scale Current 1 Month ago 1 – Buy 5 4 2 – Outperform 3 4 3 - Hold 6 6 4 – Underperform 0 0 5 - Sell 0 0 Mean Rating 2.07 2.14 Competitive Advantages • Financial Advisory and asset management well positioned for revenue growth globally • Focused on realizing operating leverage • Higher return on equity than competitors • Strong financial and liquidity position • Low risk balance sheet • Able to weather macroeconomic uncertainty • Substantial free cash flow-$403 Million • From 2000 to 2007 Lazard saw revenue growth of 56%, – Outperformed global M&A volume which was only 7% • Well positioned domestically and internationally for growth across all business lines • Revenue dipped from 1.958 Billion in 2007 before recession to 1.586 Billion in 2009 • Revenue back up to 1.956 Billion in 2010 Financial Advisory Advantages • Largest global independent financial advisory firm • Deep reservoir of senior bankers globally – Highly prestigious and well-respected bank • Geographical coverage comparable to much larger firms • Market leading Restructuring practice • Financial Advisory consists of 54% overall revenue • Involved with important government and sovereign assignments – Done consulting work for German government on Sovereign Debt Crisis • Asset Management and Restructuring reduces earnings volatility through market cycles • Financial advisory growth at Lazard in 2009 was 23%, up 24% in Q3 2011 • Goldman Sachs only 12%, Bank of America 8%, JPM 5%, Citi Group -3% Diverse Advisory • Transactions in over 40 countries in 2010 • Over 350 transactions advised on , top 10 clients only made up 17% of revenue • Industry and geographic coverage continue to expand • 27% Industrials, 18% TMT, 16% consumer, 13% power and energy, 11% healthcare, 8% FIG, 5% Real Estate, 2% Government Restructuring Practice • Market leader, most experienced global team • Over 500 restructuring deals over past decade • Largest company focused on restructuring, nearly 120 professionals globally • Advised on all 12 of the largest bankruptcies in 2009 • Advised on 19 of 25 largest bankruptcies since 2009 Asset Management Advantages • World class global institution for asset management • 52% United States, 48% International • 135.8 Billion assets under management • 9.3 Billion net inflow in 2010, 0.8 billion net outflow year to date 2011 • Asset management accounts for 46% overall revenue Future Asset Management Growth • First 3 quarters of 2011 has highest operating revenue through asset management • Look to win new mandates across broad spectrum of investment strategies around the globe – Introducing more funds to clients increasing fee revenue • Provide wider range of investment solutions • Expand geographic client base • Currently 52% North America, 15% UK, 11% France, 8% Germany, 10% Australia, 3% Japan, 1% Korea Opportunities for Growth • Capital shifts in from developed to developing markets driving growth in advisory and asset management • Increase in global demand for expert financial advice • Lazard is broadening strategic advisory services, adding more senior level talent – Leveraging reputation to expand market share in M&A space Expense/Capital Management • Focused to grow annual compensation expense at a lower rate than revenue growth • Balance sheet optimization • Share repurchasing • 2010 compensation expense at lowest level since going public Risks and Opportunities • Financial Advisory Business dependent upon macroeconomic conditions • Economic uncertainty effects M&A deal flow which hinders revenue growth – Asset Management and Restructuring act as net income stabilizers • Pipeline of deals will continue to increase over next five years as global economy grows • Lazard is invested in multiple geographic regions, perfectly positioned to benefit from continual globalization of economy • Restructuring/bankruptcy revenue steam acts as hedge against economy, increases during poor economic times Lazard Outlook • Overall financial sector experiencing recovery if profitability • Price driven down by European and global economic uncertainty • Eventually, European debt issues will be resolved, Italy has new Prime Minister with very strong economic background • Current conditions optimal for purchase of Lazard • Perfectly positioned for both domestic and international growth • 52 week high $46.54