STRATEGIC MARKETING PROBLEMS BY KERIN AND PETERSON

advertisement

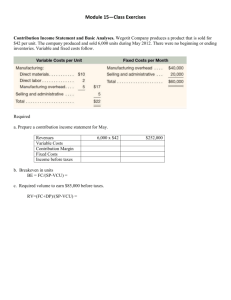

STRATEGIC MARKETING PROBLEMS BY KERIN AND PETERSON (12TH ED.) LECTURE NOTES Presented by: Teoman Duman Chapter 2. Financial Aspects of Marketing Manamagement This chapter covers concepts from accounting and finance that are useful for marketing managers. These concepts are: 1. Variable and fixed costs 2. Relevant and sunk costs 3. Margins 4. Contribution analysis 5. Liquidity 6. Operating leverage 7. Discounted cash flow 8. Customer lifetime value Variable and fixed costs Variable costs: These are expenses that are uniform per unit of output within a relevant time period; yet total variable costs fluctuate in direct proportion to the output volume units produced. In other words, as volume increases total variable costs increase. The more you produce, the more variable costs you have. Two categories; Costs of goods sold: such as materials and labor Expenses that are not directly tied to production but that nevertheless vary directly with volume: Such as sales commission, discounts and delivery expenses. Fixed costs: These are expenses that do not fluctuate with output volume within a relevant time period but become progressively smaller per unit of output as volume increases (as a percentage of output). No matter how large volume becomes, the absolute size of fixed costs remains unchanged. Two categories: Programmed costs: such as marketing expenditures – advertising, sales promotion, sales salaries. Commited costs: such as rent, administrative and clerical salaries. Relevant and sunk costs Relevant costs are future expenditures unique to the decision alternatives. Sunk costs are past expenditures for a given activity and are typically irrelevant in whole or in part to future decisions. Margins Margin refers to the difference between the selling price and the cost of a product or service. Margins can be expressed on a total volume basis or an individual unit bases, in dollar terms or as percentages. Three categories: Gross margin or gross profit is the difference between total sales revenue and total costof goods sold, or on a per unit basis, the difference between unit selling price an unit cost of goods sold. Trade margin is the difference between unit sales price and unit cost at each level of a marketing channel (for example, manufacturer wholesaler retailer ). Retailer margin as a percentage of selling price (buys a unit for $10 and sells for $20), then (10/20)*100=%50 Example on retailer margin: Two middlemen purchase and sell a product to final customers. The distribution channel, unit cost of goods sold, unit selling price and gross margin as a percentage of selling price is given in the following table; Unit cost of goods sold Unit selling price Gross Margin as a % of selling price Manufacturer $2.00 $2.88 30.6% Wholesaler 2.88 3.60 20.0 Retailer 3.60 6.00 40.0 Consumer 6.00 What are the retailer and wholesaler margin in dollar terms? 1. Retailer margin ($) = Retailer selling price *retailer margin (%) = 6.00 * 0.40 = $2.40 Retailer purchase price = Unit selling price – wholesaler margin ($) = 6-2.40= $3.60 2. Wholesaler margin ($) = Wholesaler selling price * wholesaler margin (%) = 3.60 * 0.20 = $0.72 Wholesaler purchase price = Unit selling price – wholesaler margin ($) = 3.60 – 0.72 = $2.88 1 Net profit margin is the remainder after cost of goods sold, other variable costs, and fixed costs have been subtracted from sales revenue. Important to see cash flow position. Contribution analysis Contribution is the difference between total sales revenue and total variable costs, or, on a per unit basis, the difference between unit selling price and unit variable cost. Break even analysis – the formula for unit break-even volume: Unit break even volume= total dollar fixed costs/(unit selling price-unit variable costs) Example: Fixed costs=$30,000, unit selling price $5 and unit variable costs are $2. Unit break even volume= 30,000/(5-2)=10,000 units Break-even in dollars 10,000 *$5= $50,000. Break-even analysis – the formula for dollar break-even point: First contribution margin needs to be calculated Contribution margin=(unit selling price-unit variable cost)/unit selling price Contribution margin=($5-$2)/$5= 60% Break-even dollar volume= total fixed costs/contribution margin=$30,000/0.60= $50,000 Illustration of break-even analysis is on page 38. Sensitivity analysis shows differing levels of break-even points by modified cost and contribution levels. Contribution analysis and profit impact – A modified break-even analysis can be done to incorporate a profit goal. Unit volume to achieve dollar profit goal= (total dollar fixed costs+dollar profit goal)/contribution per unit Example: Fixed costs=$200,000 Dollar profit goal=$20,000 Unit selling price=$25 Unit variable costs=$10 Therefore, Unit volume to achieve dollar profit goal= 200,000+20,000/25-10=14,667 units Multiple product break even analysis considers product mixes and identify break-even point for different types of products. Contribution analysis to market size – break-even volume should be a reasonable portion of market size so that it can be reached by the marketing efforts. Assesment of cannibalization – cannibalization is the process by which one product or service sold by a firm gains a portion of its revenue by diverting sales from another product or service also sold by the firm. This analysis calculates the contribution of cannibalization process to financial performance. It doesn’t consider fixed costs. Liquidity Refers to an organization’s ability to meet short term (usually within a budget year) financial obligations. A key measure of an organization’s liquidity position is its working capital which referes to the dollar value of an organization’s current assests (i.e. cash) and minus the dollar value of current liabilities (i.e. accounts payable). Operating Leverage Refers to the extent to which fixed costs and variable costs are used in the production and marketing of products and services. Firms that have high total fixed costs relative to total variable costs are defined as having high operating leverage. Airlines and heavy equipment manufacturers have high operating leverage. Sales increase results high profit increases for high leverage firms. Reverse is true for low leverage firms. Similarly sales decrease results high profit decreases for high leverage firms because they spend high fixed costs despite low sales. Reverse is true for low leverage firms. Discounted cash flows Customer lifetime value These are future cash flows expressed in terms of their present value. is the present value of future cash flows arising from a customer relationship. Prepapring a pro forma income statement A pro forma income statement displays projected revenues, budgeted expenses, and estimated net profit for an organization, product, or service during a specific planning period, usually a year. An example is on page 48 (Exhibit 2.4.). 2