A-133 Audit

advertisement

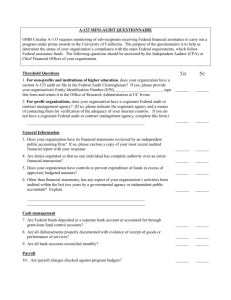

A-133 Audit Lynette Arias Director, Sponsored Projects Administration (SPA) Introduction A-133 Audit “The Annual Review” This course examines the A-133 audit cycle and explores the distribution of responsibilities and oversight within the Sponsored Projects Administration (SPA) office Audience This course is intended for “department administrative staff”—including department administrators, division managers, department fiscal managers, department effort coordinators, etc. Summary What exactly is the A-133 audit? Why is it important to understand the scope of the A-133 audit? When is the A-133 audit performed? What happens during A-133 audit? Annual FY Audit The A-133 audit is a subset of the annual fiscal year audit FY audit process begins in April/May with preliminary audit FY audit includes grant revenue testing What is the A-133 Audit? OMB Circular A-133: Audits of States, Local Governments and Non-Profit Organizations Single Audit Act of 1984, P.L. 98-502, and the Single Audit Act Amendments of 1996, P.L. 104-156. Sets forth standards for obtaining consistency and uniformity among Federal agencies for the audit of States, local governments, and nonprofit organizations expending Federal awards. One annual audit, as opposed to each agency conducting their own individual audits Why is it important to understand the scope? The A-133 is submitted to the Department of Health and Human Services (DHHS), OHSU’s cognizant agency Most of OHSU’s sponsored project dollars come from DHHS DHHS is expected to scrutinize OHSU business procedures most closely When is the A-133 performed? Annually Starts with planning in the Spring Actually commences during the FY financial audit July/August Continues into Fall--timing varies slightly each year Performed by external auditors Currently KPMG What happens during the A-133 Audit? Auditors provide list of “control overview documents” Provide auditors “The Schedule” Provide auditors set of reports Provide auditors policies and procedures Undergo general testing Undergo grant testing Review student financial aid Follow filing process Control overview documents These documents are provided by independent audit firm, KPMG International, at the beginning of each audit to be reviewed and updated by OHSU Control overview documents include: C-AB Activities Allowed C-C Cash Management C-F Equipment and Real Property C-G Matching C-H Period of Availability C-I Procurement C-J Program Income C-L Reporting C-M Subrecipient Monitoring What happens during the A-133 Audit? Provide auditors “The Schedule,” a listing by project of all federal sponsored project expenditures Direct – received directly from a federal agency Pass-through – received from an agency that received federal funding and is passing that funding through to OHSU Subrecipient – “subout” expenditures What happens during the A-133 Audit? Provide auditors (Cont.) All projects listed by Catalog of Federal Domestic Assistance (CFDA) Program & Number Grouped by “clusters”: • Research & Development (R&D) • Student Financial Aid • Other Report Schedules See attached sample page from report “schedules” FY06 A-133 Audit Report on SPA website: http://www.ohsu.edu/research/rda/spa/doc s/ohsu_a133_06.pdf Provide Reports Provide auditors set of reports Vendors paid over $100,000 in FY Listing of all active projects in FY-period of availability Listing of personnel paid over the cap Listing of federally funded construction projects OGA/GL revenue and expenditure reconciliation Federal cash transaction reports Fixed Assets disposition reports Provide Updated Policies and Procedures General OHSU Affirmative Action Purchasing and Contracting Sponsored Projects Fixed Assets F&A Rate and Cost Accounting Standards (CAS) DS-2 Services Centers and Recharging General Testing Service Centers Fixed Assets Federal Agency Audits during FY Cash Transactions Specific Award Testing Generally 10-20 projects are selected for detailed grant testing. Total dollar amount must cover a certain scope of overall federal funding to OHSU. Judgmental sample selected by auditors. Relates to major programs – by CFDA #. Grant Testing Award Documents and Reports, including cost sharing Expenditures – Overall and Program Income Expenditures – Payroll / Effort Certification Subrecipients Cost Transfers F&A Reconciliations Earmarking / Restrictions Fixed Assets Grant Testing: Award Documents and Reports Award Notice or Contract Award Proposed Project Questionnaire (PPQ), indicating Program Income and Cost Sharing Financial Status Report (FSR) and reconciling Oracle Award or Project Status Report Award Technical Progress Report Other reports required by terms and conditions of the award Grant Testing: Expenditures – Overall OGA Award Status Report OGA Project Status Report OGA Project Expenditure Details Report Program Income OGA Award Status Report Program Income OGA Project Status Report Program Income OGA Project Expenditures Detail Report Expenditure backup on selected non-payroll expenditures (AP detail) Grant Testing: Expenditures – Payroll/Effort Reconciliation between OGA and Payroll OGA Project Expenditures Details Report for payroll expenditures Detail Payroll Expenditures Report (DEPR) Manual JE’s for Payroll Payroll expenditure backup HR File Review Effort Certification Statements (ECS) Grant Testing: Subrecipients OGA Project Expenditure Details Report Summary listing of all subrecipients under test projects Subrecipient contract document and amendments Subrecipient invoice(s) Subrecipient A-133 (if applicable) Grant Testing: Cost Transfers Copies of all cost transfers on test projects Grant Testing: F&A Reconciliations F&A reconciliation summary F&A exclusions OGA screen shots of F&A rate in system Reconciliation of F&A on test projects Grant Testing: Earmarking/Restrictions Summary listing of all test projects and indication of if restrictions exist Restriction supporting documentation on test projects Grant Testing: Fixed Assets Asset inventory supporting documentation Student Financial Aid Annual Schedule of Federal Financial Assistance Expenditures US DoEd Funding Authorization Letters and Institutional Worksheets Program Participation Agreement & US DoEd Approval Letter Status of Accreditation Letter There are also test year procedures undergone every three years For example, SFA procedures, Direct Loan Draw History, or Perkins Cancellations Filing Process Rep Letter Final Financials Final SEFA Data Collection Form – online submission to clearinghouse Online submission to clearinghouse Hard copy submission packet to clearinghouse EZ Audit submission with final pdf of full A-133 report How can Departments help with the A-133 Audit? Adhere to all terms and conditions Adhere to all Federal regulations, policies, and procedures Adhere to OHSU policies and procedures Doing this as you go along helps streamline the A-133 process And ensures a clean audit and compliance with all policies and procedures FY06 Audit FY06 A-133 Audit recently filed No findings No questioned costs Complete A-133 audit reports are posted on the SPA webpage: http://www.ohsu.edu/research/rda/spa/spa a133.shtml Questions?