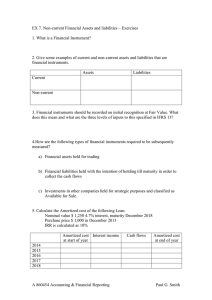

Financial Instruments

advertisement

Financial Instruments Future Changes in Standards? Exposure Draft 2010 Financial Instruments NOW • Some financial instruments are currently reported at fair value on a routine basis: – Those included in trading and available for sale investment portfolios – Those for which the fair value option has been adopted at acquisition date • Most liabilities are carried at amortized cost with fair values disclosed in the notes What is a Financial Instrument Financial Instrument Cash, evidence of an ownership interest in an entity, or a contract that both: • a. Imposes on one entity a contractual obligation either: – 1. To deliver cash or another financial instrument to a second entity – 2. To exchange other financial instruments on potentially unfavorable terms with the second entity. • b. Conveys to that second entity a contractual right either: – 1. To receive cash or another financial instrument from the first entity – 2. To exchange other financial instruments on potentially favorable terms with the first entity. FASB Exposure Draft • Under the proposal, almost all financial instruments would be reported at fair value on the balance sheet. • This would include many liabilities currently carried at amortized cost – Exception: long-term debt related to long-lived assets like a mortgage on a building • In some cases, the gain/loss would be in other comprehensive income rather than net income Exposure Draft • If this ED becomes a standard (as written) – We would be getting rid of the 3-categories of investments we have from SFAS115 (trading, available for sale, and held-to-maturity) – In effect, we could still have HTM but we would have fair value on the balance sheet and the gain/loss would be reported in “other comprehensive income” rather like what we currently do for available-for-sale securities Amortized Cost is Also Important • The FASB doesn’t want to lose valuable information so the proposal calls for reporting BOTH fair value and amortized cost on the face of the balance sheet • Complications: – Credit-worthiness affects borrowing rate – a lower credit rating = higher interest rate – Higher interest rate = lower present value (when using level 2 measurements) Balance Sheet Display – Investment Side * ** *Amortization of discount/premium is charged to credit impairment allowance **To bring carrying value to fair value of the financial instrument Exposure Draft • Proposal includes disclosure of the portion of the gain/loss that is related to the change in credit score separately from the gain/loss related to general changes in interest rates • Choice of equity method for investments will be limited to situations where the investee is closely related to the investor’s business strategy. Otherwise, will be reported at fair value