The Facts on Credit

advertisement

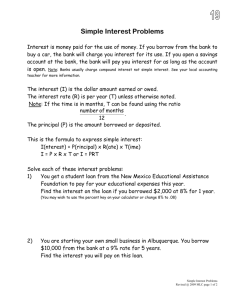

The Facts on Credit Those who are wise never pay interest… they earn it! What is Credit? Another word for credit is loan… 3 Main types of credit: Sales Credit you receive when you make a purchase and promise to pay later. Cash Credit you receive when you borrow cash and promise to pay it back later. Service Credit given for a service one receives (utilities, dentist, hospital, etc.) that will be payed for later. How much credit can I use? The total amount of credit should not exceed 20% of one years NET income… How much can a person borrow that makes $36,000 net? Answer: $7200 (This includes your car loan…) $7200/12 months= $600 a month!!! (not including interest) The Cost of Credit Principal Interest (rate) Years Payment Total Interest Total Cost $1,000.00 12% 2 $47.07 $129.79 $1,129.79 $1,000.00 21% 2 $51.39 $233.21 $1.233.21 $5,000.00 12% 8 $70.68 $1,785.71 $6,785.71 $5,000.00 21% 30 $87.67 $26,561.28 $31,561.28 $150,000.00 7% 30 $997.00 $209,266.00 $359,266 $150,000.00 7% 15 $1,348.24 $92,683.00 $242,683.00 $350,000.00 7% 30 $2,328.56 $488,279.00 $838,279.00 HIDDEN COST OF LOW INTEREST CREDIT CARDS Balance transfers usually charge 3% on principal $30 late fees with no grace period (Considered late one day after due date) If late, interest rate bumps up to 21% $30 over balance fees Convenience checks have transaction fees Advantages of Credit Stimulates the economy Helps us take care of emergencies Convenient – ordering over the phone Establishes a credit rating Advance notice of sales and cask back on purchases Easier to exchange and return items Detailed monthly bill Disadvantages of Credit It always costs money Risky to spend future income Encourages careless buying (Needs vs. wants) Facilitates over-buying which increases sacrifice that must be made eventually Often increases family conflict May lead to Bankruptcy Increases the cost of doing business Payday Loans *The borrower requests a loan for a short period of time, usually one to four weeks. *“Payday loan fee” - Up to 360% interest. *If the borrower continues to have a financial problems and cannot pay the loan as promised, the interest keeps building on the debt. Other Options…. Try a small loan from a credit union Ask for pay in advance from your employer Consider a loan from family or friends, (be sure to have the terms of the loan in writing) Use a credit card cash advance Request additional time to pay the bill from your creditors. Pawn Brokers Or… just don’t borrow money!!! Credit Rating/ FICO Score A credit rating assesses the credit worthiness of an individual. Credit ratings are calculated from financial history and current assets and liabilities. A credit rating tells a lender or investor the probability of the person being able to pay back a loan. In recent years, credit ratings have also been used to adjust insurance premiums, determine employment eligibility, and establish the amount of a utility or leasing deposit. A poor credit rating indicates a high risk of defaulting on a loan, and thus leads to high interest rates, or the refusal of a loan by the creditor. Establishing Credit Have checking and savings accounts and manage them responsibly. (These are not reported to the credit agencies, but help individuals develop a pattern of budgeting.) Use layaway plans at stores Save for large down payments on cars and other purchases. Ask someone to be a cosigner for the loan. Always make payments for bills ON TIME!!! (cell phone, utilities, credit cards, house payment etc.) If you are REJECTED… Obtain a copy of your credit report to determine what the problem is. If something is incorrect, notify the credit bureau in writing. Fixing credit problems may take up to six months. Let’s talk interest rates… Bad Credit vs. Good Credit Bad Credit $3000 on credit card 18% interest rate If minimum payment of 2 ½% is only made… It takes 22 years and $4100 dollars in interest to pay of the debt. Total: $7100 to borrow $3000 Good Credit $3000 on credit card 4% interest rate If minimum payment of 2 ½% is only made… It takes 11 years and $400 in interest to pay off the debt. Total: $3400 to borrow $3000 Scary Statistics The average American household has $9200 in credit card debt. In 2005, 21,476 people declared bankruptcy in Utah. At the end of 2005, Utah was ranked 3rd in the U.S. In Utah, bankruptcies are filed at the rate of one in every 37 homes! The national average is one in every 73 homes! Moral of the Story… Don’t spend more than you earn!!! Use credit wisely!!! Don’t get into debt!!! References http://en.wikipedia.org/wiki/Credit http://www.bankhs.com/teachers/utah_ba nkruptcy.html http://www.utah.freebankruptcyevaluation .com/bankruptcy-statistics.html www.Suzeorman.com UEN Data Base