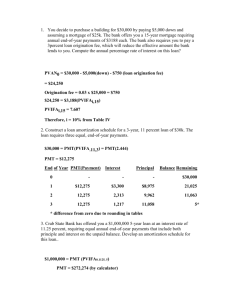

tutorial pack one answers

Tutorial One/Two

1.

From the following balance sheet accounts: a. construct a balance sheet for 2010 and 2011 b. list all the working capital accounts c. find the net working capital for the years ending 2010 and 2011 d. calculate the change in net working capital for the year 2011

Balance Sheet Accounts of Athens Corporation

Account

Accumulated Depreciation

Accounts Payable

Accounts Receivable

Balance 12/31/2010

$4,234

$2,900

$3,160

Balance 12/31/2011

$4,866

$3,210

$3,644

Cash

Common Stock

Inventory

$1,210

$4,347

$1,490

$4,778

$5,166

$7,278

Long-Term Debt

Plant, Property & Equipment

Retained Earnings

$3,600

$8,675

$1,880

$2,430

$9,840

$2,356

ANSWER a. The Balance Sheets for the two years are:

Assets:

Current Assets

Cash

Accounts Receivable

Inventory

Total Current Assets

Long-Term Assets

Plant, Prop. & Equip

Minus Acc. Depreciation

Net P P & E

TOTAL Assets

Liabilities

Current Liabilities

Accounts Payable

Long-Term Liabilities

Long-term Debt

Total Liabilities

Owner’s Equity

Common Stock

Retained Earnings

Total Owner’s Equity

TOTAL Liab. & O.E.

2010

$1,210

$3,160

$4,347

$8,717

$8,675

($4,234)

$4,441

$13,158

$2,900

$3,600

$6,500

$4,778

$1,880

$6,658

$13,158 b. The Working Capital Accounts are:

2011

$1,490

$3,644

$5,166

$10,300

$9,840

($4,866)

$4,974

$15,274

$3,210

$2,430

$5,640

$7,278

$2,356

$9,634

$15,274

Cash, Accounts Receivable, Inventory, and Accounts Payable

c. The Net Working Capital for 2010 and 2011:

Net Working Capital = Cash + Accounts Rec. + Inventory – Accounts Pay.

2010 Net Working Capital = $1,210 + $3,160 + $4,347 - $2,900 = $5,817

2011 Net Working Capital = $ $1,490+ $3,644 + $5,166 - $3,210 = $7,090 d. The Change in Net Working Capital for 2011 is, $7,090 - $5,817 = $1,273 or an increase in Net Working Capital of $1,273.

2.

From the following income statement accounts a. produce the income statement for the year b. produce the operating cash flow for the year

Income Statement Accounts for the Year Ending 2011

Cost of Goods Sold

Interest Expense

Taxes

$1,419,000

$ 288,000

$ 318,000

Revenue

SG&A Expenses

Depreciation

$2,984,000

$ 454,000

$ 258,000

ANSWER a. Income Statement

Revenue

Cost of Goods Sold

SG&A Expenses

Depreciation

EBIT

Interest Expense

Taxable Income

Taxes

Net Income

$2,984,000

$1,419,000

$ 454,000

$ 258,000

$ 853,000

$ 288,000

$ 565,000

$ 318,000

$ 247,000 b. Operating Cash Flow

OCF = EBIT – Taxes + Depreciation

OCF = $853,000 - $318,000 + $258,000 = $793,000

3.

Find the operating cash flow for the year for Shore Brothers Inc. if it had sales revenue of

$440,000,000, cost of goods sold of $215,000,000, sales and administrative costs of

$65,000,000, depreciation expense of $45,000,000, and a tax rate of 40%.

ANSWER

Using the income statement format, we have

Revenue $440,000,000

COGS

SG&A Expenses

Depreciation

EBIT

$215,000,000

$65,000,000

$45,000,000

$115,000,000

Taxes (@ 40%)

Net Income

$46,000,000

$69,000,000

Operating Cash Flow

EBIT

Depreciation

Taxes

Operating Cash Flow

$115,000,000

$45,000,000

$46,000,000

$114,000,000

4.

Find the operating cash flow for the year for Stewart and Sons if it had sales revenue of $100,000,000, cost of goods sold of $40,000,000, sales and administrative costs of

$7,200,000, depreciation expense of $8,300,000, and a tax rate of 30%.

ANSWER

Using the income statement format, we have

Revenue $100,000,000

COGS

S & A Costs

Depreciation

EBIT

$40,000,000

$7,200,000

$8,300,000

$44,500,000

Taxes (@ 30%) $13,350,000

Net Income $31,150,000

Operating Cash Flow

EBIT

Depreciation – Taxes

Operating Cash Flow = $44,500,000

$8,300,000

$13,350,000

$39,450,000

Tutorial Three/Four

ANSWER

Holding Property Four Years:

FV

$320,000 X

(1.05)

4

$320,000 X

1.2155

$388,962

Holding Property Eight Years:

FV

$320,000 X

(1.05)

8

$320,000 X

1.4775

$472,785.74

ANSWER

FV

$550 X

(1.045)

4

$550 X

1.1925186

$655.89

ANSWER

FV

$22,500 X

(1.05)

5

$22,500 X

1.27628

$28,716.34

ANSWER

Future Value

$900.00

Interest Rate

5.0%

Number of Periods Present Value

5 $705.17

$80,000.00

$350,000.00

$26,981.75

6.0%

10%

16%

30

20

15

$13,928.81

$52,025.27

$2,912.06

a. With TVM formula (rounding to second decimal only for final answer)

PV = $900.00 × 1/(1.05) 5 = $400.00 × 0.7835 = $705.17

PV = $80,000.00 × 1/(1.06)

30

= $80,000.00 × 0.1741 = $13,928.81

PV = $350,000.00 × 1/(1.10)

20

= $350,000.00 × 0.1486 = $52,025.27

PV = $26,981.75 × 1/(1.16) 15 = $26,981.75 × 0.1079 = $2,912.06 b. Time Value of Money Keys or Spreadsheet

Input 5 5.0 0

Variable

Compute

N I/Y PV

-900

PMT FV

705.17

Input

Variable

Compute

Input

Variable

Compute

Input

Variable

Compute

30

N

20

N

15

N

6.0

I/Y

10.0

I/Y

16.0

I/Y

0

PV

0

PV

-80,000

PMT FV

13,928.81

-350,000

PMT FV

52,025.27

0 -26,981.75

PV PMT FV

2,912.06

5.

Future value: You are a new employee with the Metropolis Daily Planet . The Planet offers three different retirement plans for you to choose from. Plan 1 starts the first day of work and puts $1,000 away in your retirement account at the end of every year for forty years. Plan 2 starts after ten years and puts away $2,000 every year for thirty years. Plan 3

starts after twenty years and puts away $4,000 every year for the last twenty years of employment. All three plans guarantee an annual growth rate of 8%. a. Which plan should you choose if you plan to work at the Planet for forty years? b. Which plan should you choose if you only plan to work at the Planet for the next thirty years? c. Which plan should you choose if you only plan to work at the Planet for the next twenty years? d. Which plan should you choose if you only plan to work at the Planet for the next ten years? e. What do the answers in parts (a) through (d) imply about savings?

ANSWER

Part a: Plan One FV = $1,000 × (1.08

40

-1)/0.08 = $1,000 × 259.0565 = $259,056.51

Part a: Plan Two FV = $2,000 × (1.08

30 -1)/0.08 = $2,000 × 113.2832 = $226,566.42

Part a: Plan Three FV = $4,000 × (1.08

20

-1)/0.08 = $4,000 × 45.7620 = $183,047.86

Chose Plan One

Part b: Plan One FV = $1,000 × (1.08

30 -1)/0.08 = $1,000 × 113.2832 = $113,283.21

Part b: Plan Two FV = $2,000 × (1.08

20

-1)/0.08 = $2,000 × 45.7620 = $91,523.93

Part b: Plan Three FV = $4,000 × (1.08

10

-1)/0.08 = $4,000 × 14.4866 = $57,946.25

Chose Plan One

Part c: Plan One FV = $1,000 × (1.08

20

-1)/0.08 = $1,000 × 45.7620 = $45,761.96

Part c: Plan Two FV = $2,000 × (1.08

10

-1)/0.08 = $2,000 × 14.4866 = $28,973.12

Part c: Plan Three FV = $4,000 × (1.08

0

-1)/0.08 = $4,000 × 0.0000 = $0.00

Chose Plan One

Part d: Plan One FV = $1,000 × (1.08

10

-1)/0.08 = $1,000 × 14.4866 = $14,486.56

Part d: Plan Two FV = $2,000 × (1.08

0

-1)/0.08 = $2,000 × 0.0000 = $0.00

Part d: Plan Three FV = $4,000 × (1.08

0

-1)/0.08 = $4,000 × 0.0000 = $0.00

Chose Plan One

Part e: The sooner you begin to save the better and that increasing the amount of savings in later years may not be sufficient to catch up to an early savings program.

1.

Challenge question II . Tyler wants to buy a beach house as part of his investment portfolio. After searching the coast for a nice home, he finds a house with a great view and a hefty price of $4,500,000. Tyler will need to borrow from the bank to pay for this house. Mortgage rates are based on the length of the loan, and a local bank is advertising fifteen-year loans with monthly payments at 7.125%, twenty-year loans with monthly payments at 7.25%, and thirty-year loans with monthly payments at 7.375%. What is the monthly payment of principal and interest for each loan? Tyler believes the property will be worth $5,500,000 in five years. Ignoring taxes and real estate commissions, if Tyler

sells the house after five years, what will be the difference in the selling price and the remaining principal on the loan for each of the three loans?

ANSWER

Monthly Payments for the 15 year loan:

Payment = PV / (1 – 1/(1+r) n

) / r

Payment = $4,500,000 / (1 – 1/(1+0.07125/12) 15 x 12 ) / (0.07125/12)

Payment = $4,500,000 / 110.3958 = $40,762.40

OR

TVM Keys: Mode P/Y = 12 and C/Y = 12

INPUT 180 7.125 -450,000

KEYS N

OUTPUT

I/Y PV

?

PMT

40,762.40

Amortization P1 = 60 and P2 = 60, Balance = $3,491,314.54

Monthly Payments for the 20 year loan:

Payment = PV / (1 – 1/(1+r) n

) / r

Payment = $4,500,000 / (1 – 1/(1+0.0725/12) 20 x 12 ) / (0.0725/12)

Payment = $4,500,000 / 126.5221 = $35,566.92

OR

0

FV

TVM Keys: Mode P/Y = 12 and C/Y = 12

INPUT 240 7.25 -450,000

KEYS N

OUTPUT

I/Y PV

?

PMT

35,566.92

Amortization P1 = 60 and P2 = 60, Balance = $3,896,195.15

0

FV

Monthly Payments for the 30 year loan:

Payment = PV / (1 – 1/(1+r) n

) / r

Payment = $4,500,000 / (1 – 1/(1+0.07375/12)

15 x 12

) / (0.07375/12)

Payment = $4,500,000 / 144.7859 = $31,080.38

OR

TVM Keys: Mode P/Y = 12 and C/Y = 12

INPUT 360 7.375 -450,000

KEYS N

OUTPUT

I/Y PV

?

PMT

31,080.38

Amortization P1 = 60 and P2 = 60, Balance = $4,252,462.31

0

FV

Difference between selling price and principal remaining on the loan is:

15 Year Loan: $5,500,000 – $3,491,314.54 = $2,008.685.46

20 Year Loan: $5,500,000 – $3,896,195.15 = $1,603,804.85

30 Year Loan: $5,500,000 – $4,252,462.31 = $1,247,537.69