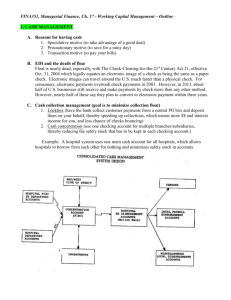

Credit Scores – How they Impact your Financial Success

advertisement

Credit Scores How They Impact Your Financial Success Presented by: Lynne A. Coverdale, MBA Salin Bank & Trust Company 1 The FICO stands for Fair Isaac and Co., a company founded in 1956 by Bill Fair, an engineer, and Earl Isaac, a mathematician The company philosophy was that data can improve business decisions when applied intelligently. In 1957, Conrad Hilton hired FICO to develop and install a billing system for Carte Blanche, one of the first credit card companies. In 1958- Fair Isaac began creating credit score systems FICO sent letters to 50 biggest American credit grantors asking for opportunity to explain a new concept – credit scoring FICO builds its first credit scoring system for American Investments (the only respondent out of the 50 companies) In 1963- FICO builds credit scoring system for Montgomery Ward – beginning of a very long term relationship 2 In 1981 – FICO introduced the first credit bureau risk score By 1991 all three credit bureaus were using the FICO credit bureau scores as their standard procedure The three bureaus: Experian, TransUnion and Equifax Experian score: FICO® (Experian) Transunion score: Classic Score formerly called Emperica Equifax score: Beacon 3 In 1993 – the first insurance bureau score is introduced for the insurance industry Early 90s – mortgage lenders and banks are using credit scores for lending decisions in some cases In 1995 – Fannie Mae and Freddie Mac recommend use of “FICO” scores for evaluating US mortgage loans 4 2001 to today – credit score usage expands into a variety of industries, credit score education is prevalent The range of scores for each of the bureaus is roughly 300 – 850 Equifax: 334 – 818 Experian: 320 – 844 Transunion: 309 - 839 The higher the score - the better Examples: better rate, lower insurance cost, obtain a job offer 5 Identifying information Requestor’s identifying information Your name, and previous names Address history Social security number Date of birth Employment information Name Address Contact Tradelines Current accounts open with or without a balance Closed accounts Paid-off accounts History of tradelines 6 Public records Judgments Bankruptcies Foreclosures Liens such as tax liens Satisfactions Inquiries Typically for the last 90 – 120 days Credit Scores Score from each bureau ordered Key 4 -5 factors that adversely affected the score 7 Specific to Mortgage Credit Reports ID Cross Check Compares social security number provided to social security number on record for each bureau, also compares to SSA issuance date and SSA death master Compares current address provided to address history for each bureau Checks birthdate of record Identity index provided The higher the index, the better – the more the consumer’s identity was verified 8 Consumer Lenders Banks Credit unions Auto finance companies Mortgage Bankers, Mortgage Brokers Commercial and Business Lenders Other Companies Insurance companies Prospective employers Landlords US Government 9 Credit reports and credit scores are accessed and evaluated to aid in decisions such as: Consumer Lenders Auto loans RV loans Personal loans Lines of credit Credit cards Mortgage Bankers, Mortgage Brokers First mortgages Second mortgages Home equity lines of credit 10 Credit reports and credit scores are accessed and evaluated to aid in decisions such as: Commercial and Business Lenders Small business loans Commercial loans Lines of credit Other Companies Insurance companies Insurance for autos, homes, businesses, personal property Prospective employers Possible employment opportunities Landlords Apartment or home rentals US Government – background checks Special projects Employment 11 The number and types of accounts you have Credit cards, auto loans, mortgages, other installment loans Credit payment history Paid on time? Paid late? Not paid? Percentage of available credit you are using versus available credit Age of accounts Derogatory accounts/ history 12 Payment history (35%) Amounts owed (30%) Amount owed versus amount available Length of credit history (15%) The number and types of accounts (10%) Paid on time? Paid late? Not paid? Credit cards, auto loans, mortgages, other installment loans Inquiries/new credit (10%) 13 Source: myFICO 14 Credit score detail A person has a score of 700 which consists of: 35% = 245 points for Payment history 30% = 210 points for Amounts owed $4,000 balance on a $5,000 credit card 15% = 105 points for Length of credit history Had old history but just closed out the oldest accounts 10% = 70 points for Types of credit 10% = 70 points for New credit/ inquiries 15 Credit score detail A person has a score of 740which consists of: 35% = 259 points for Payment history 30% = 222 points for Amounts owed $450 balance on a $5,000 credit card 15% = 111 points for Length of credit history Did not close out any old accounts 10% = 74 points for Types of credit 10% = 74 points for New credit/ inquiries 16 Loan Level Price Adjustment Chart Fannie Mae 17 Mortgage Example 95% LTV (5% down) purchase: Credit score 700 $200,000 loan on 30 year fixed Loan Level Pricing Adjustment (LLPA) 1.0% Rate: 4.50% PMI: .89% ($148.33) Principal and interest and Mortgage Insurance: $1,161.70 Credit score 720 $200,000 loan on 30 year fixed Loan Level Pricing Adjustment (LLPA) .50% Rate: 4.375% PMI: .67% ($111.67) Principal and interest: $1,110.24 Credit score 740 $200,000 loan on 30 year fixed Loan Level Pricing Adjustment (LLPA) .25% Rate: 4.25% PMI: .54% ($90.00) Principal and interest: $1,073.88 18 Mortgage Example 80% LTV (20% down) purchase: Credit score 700 $200,000 loan on 30 year fixed Loan Level Pricing Adjustment (LLPA) 1.0% Rate: 4.50% Principal and interest: $1,013.37 Credit score 720 $200,000 loan on 30 year fixed Loan Level Pricing Adjustment (LLPA) .50% Rate: 4.375% Principal and interest: $998.57 Credit score 740 $200,000 loan on 30 year fixed Loan Level Pricing Adjustment (LLPA) .25% Rate: 4.25% Principal and interest: $983.88 19 20 Fact or Myth: Not having credit is the best strategy for credit scores? Fact or Myth: Credit Scores are fixed for a year? Fact or Myth: Opening a new account does not affect your score? Fact or Myth: Using the majority of your credit line is a great strategy to build your credit? Fact or Myth: Not having revolving credit will insure your credit score is the highest? Fact or Myth: You should always close out accounts that you don’t use? 21 Fact or Myth: Each creditor sends payment information to each of the 3 bureaus? Fact or Myth: Having no more than 30% of your credit lines outstanding is a good strategy to maximize credit scores? Fact or Myth: Opening a credit card is a good idea to establish credit? Fact or Myth: Being added on as an authorized user to a persons credit card is all one needs to do to establish credit? Fact or Myth: Inquiries into your credit make a huge impact on your credit scores? Fact or Myth: Scores are the same for each credit bureau? 22 Shred Shred Shred Opt-out of unwanted mail and solicitations Get on do not call list Don’t give passwords or personal information over the phone Protect your passwords Change them Keep personal information secure and offline If online – make sure it is safe, secure, encrypted, password protected Vacation hold for mail or mail picked up by trustworthy neighbor or family member, friend Trash receptacles back from front of house in timely manner Use the blue box Don’t overshare on social media sites 23 Lock up your laptop Be careful when you use Wi-Fi in public areas Perhaps use your own personal hotspot Avoid phishing emails Example annual credit search 24 What is the difference between a soft credit pull and a hard credit pull? How do I obtain a copy of my credit report? How can I stop the junk mail solicitations How do I dispute inaccurate information on my credit report? Why are my credit scores different? 25 www.annualcreditreport.com www.optoutprescreen.com or 1-888-5-optout www.donotcall.gov www.dmachoice.org http://www.ftc.gov/faq/consumer-protection www.experian.com www.equifax.com www.transunion.com www.myfico.com https://salin.mortgagewebcenter.com/Resources 26 My contact information: Lynne Coverdale Salin Bank and Trust 8455 Keystone Crossing Dr. Indianapolis, IN 46240 317-452-8125 – direct 317-370-0016 – cell l.coverdale@salin.com www.Salin.mortgagewebcenter.com 27