Recognition of Pension Obligation

advertisement

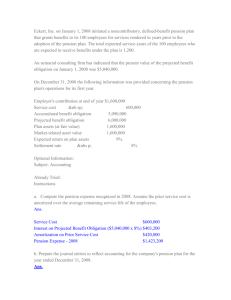

. CHAPTER 4.3.10 GAAP ADJUSTMENTS AND RECLASSIFICATION ENTRIES LIABILITIES: PENSION OBLIGATION 1 GAAP POLICIES AND PROCEDURES University Pension Plan The University, as an agency of the State, contributes to California Public Employees’ Retirement System (CalPERS). The State’s plan with CalPERS is an agent multipleemployer defined-benefit pension plan and CalPERS function as an investment and administrative agent for its members. For the University, the plan acts as a cost-sharing multiple-employer defined-benefit pension plan, which provides a defined-benefit pension and postretirement program for substantially all eligible University employees. The plan also provides survivor, death, and disability benefits. Eligible employees are covered by the Public Employee’s Medical and Hospital Care Act (PEMHCA) for medical benefits. Employee Contribution The University personnel are required to contribute 5.0% of their annual earnings in excess of $513 per month to CalPERS. Effective January 1, 2013, all new employees that are considered “new members” to CalPERS are required to contribute 50% of the normal cost for their category (e.g. State Miscellaneous Member is 6% of their annual earnings per month to CalPERS). Employer Contribution The University is required to contribute at an actuarially determined rate; the current rate for State Miscellaneous is approximately 24.3% of annual covered payroll. The contribution requirements of the plan members are established and may be amended by CalPERS. The contractual maximum contribution required for the University is determined by the annual CalPERS compensation limit(s) which are based on provisions of Assembly Bill (AB) 340 and the Internal Revenue Code (IRC) 401 (a) 17 limits. The employer contribution pertaining to pension is recorded in the legal basis books in FIRMS object code 603005, Retirement, which derives to GAAP account 722002, Benefits. Recognition of Pension Obligation Effective fiscal year 6/30/2015, GAAP requires recognition of a liability equal to the net pension liability, which is measured as the total pension liability, less the amount of the pension plan’s fiduciary net position. The total pension liability is determined based upon discounting projected benefit payments based on the benefit terms and legal agreements existing at the pension plan’s fiscal year end. Projected benefit payments are required to be discounted using a single rate that reflects 4.3.10-1 GAAP Manual | GAAP Adjustments and Reclassification Entries – Liabilities: Pension Obligation | June 30, 2015 . 2 the expected rate of return on investments, to the extent that plan assets are available to pay benefits, and a tax-exempt, high-quality municipal bond rate when plan assets are not available. GAAP requires that most changes in the net pension liability be included in pension expense in the period of the change. RELEVANT ACCOUNTING LITERATURE In June 2012, the GASB issued Statement No. 68, Accounting and Financial Reporting for Pensions, effective for the University’s fiscal year beginning July 1, 2014. This Statement revises existing standards for employer financial statements relating to measuring and reporting pension liabilities for pension plans provided by the University to its employees. 3 OBJECTIVE OF GAAP ADJUSTMENTS In compliance with GAAP, the University should recognize its proportionate share of the following as of and for the year then ended: (a) Net pension obligation (b) Pension expense (c) Deferred outflows of resources related to pension (d) Deferred inflows of resources related to pension 4 GAAP ACCOUNTING TREATMENT AND JOURNAL ENTRIES 4.1 GAAP ACCOUNT(S) 722002 – Benefits 712210 – Pension Obligation 711302 – Deferred Outflows – Net Pension Obligation 712302 – Deferred Inflows – Net Pension Obligation 4.2 RECOGNITION AND MEASUREMENT IN FINANCIAL STATEMENTS 4.2.1 Key Recognition and Measurement Dates 1. Fiscal Year-End 2. Measurement Date – No earlier than end of the prior fiscal year. Total Pension Liability (TPL) and Plan Fiduciary Net Position are calculated as of this date. 3. Actuarial Valuation Date – If not the same as measurement date, as of date should be no more than 30 months +1 day prior to fiscal year end. At least every 2 years, more frequent valuation is encouraged. Actuarial results must be projected forward from the valuation date to the measurement date. It must reflect any source of material impact like legally adopted changes in the benefit terms prior to the measurement date. 4.3.10-2 GAAP Manual | GAAP Adjustments and Reclassification Entries – Liabilities: Pension Obligation | June 30, 2015 . 4.2.2 Recognition and Measurement – Net Pension Liability, Pension Expense, Deferred Outflows/Inflows of Resources The University shall recognize its proportionate share of the collective net pension liability of the cost-sharing employers as of measurement date. The collective net pension liability is actuarially determined by CalPERS annually. CalPERS determines the proportionate share of the State of California (State). The State then determines the proportionate share of the University which is further allocated to the 23 campuses and the Office of the Chancellor. The year-over-year change in net pension liability is usually recognized as pension expense. Pension expense include service cost, interest in TPL, effects of benefit changes, projected earnings on plan investments. There are exceptions to this general concept, they are as follows: Difference between expected and actual experience (TPL)* Changes of assumptions (TPL)* Difference between projected and actual earnings on pension plan investments * Employer contributions** *Pension expense is recognize in current and future periods. Amortization period varies based on the type of difference/change. The portion not recognized as expense are in deferred outflows/inflows of resources related to pensions. ** Employer contributions during the measurement period directly reduce net pension liability (no expense impact). Employee contributions subsequent to measurement date shall be recognized as deferred outflow of resources related to pension and directly reduce NPL in the next reporting period (no expense impact). 4.3.10-3 GAAP Manual | GAAP Adjustments and Reclassification Entries – Liabilities: Pension Obligation | June 30, 2015 . The University should recognize the proportionate share of the pension expense, and collective deferred outflows of resources and collective deferred inflows of resources. The determination of the proportionate share of the University is discussed in the GASB 68 implementation memo from the State, see section 5, Reference Tools, below. The campus allocation will be provided by the CO as a passdown schedule for GAAP reporting, see Chapter 5 of this manual. Below is an example of the journal entry in GAAP which should be reversed in the subsequent year. Manual GAAP Entry (Period 998) Account 722002 711302 712302 712210 Journal Description 5 Account Name Benefits Deferred outflows – Net Pension Obligation Deferred inflows – Net Position Obligation Pension Obligation Fund (Net Position) Program Class (CSU Fund) 881-Unrestricted 20 531 $X,XXX 881-Unrestricted 90 531 $X,XXX 881-Unrestricted 90 531 ($X,XXX) 881-Unrestricted 90 531 ($X,XXX) Amount To record pension obligation as of June 30. REFERENCE TOOLS 5.1 SCO GASB STATEMENT NO. 68 IMPLEMENTATION MEMO (PENDING) 5.2 TABLES OF OBJECT CODE AND CSU FUND DEFINITIONS http://www.calstate.edu/SFSR/standards_and_rules/2014/Tables-of-Object-Code-andCSU-Fund-Definitions-Updated-10-30-14.xls 5.3 GASB STATEMENT NO. 68 IMPLEMENTATION GUIDE WITH Q&A http://gasb.org/jsp/GASB/Page/GASBSectionPage&cid=1176163026371 4.3.10-4 GAAP Manual | GAAP Adjustments and Reclassification Entries – Liabilities: Pension Obligation | June 30, 2015 . REVISION CONTROL Document Title: CHAPTER 4.3.10 – GAAP ADJUSTMENTS AND RECLASSIFICATION ENTRIES – LIABILITIES: PENSION LIABILITY REVISION AND APPROVAL HISTORY Section(s) Revised General 4.3.10-5 Summary of Revisions Revision Date New addition to the GAAP Manual as a result of GASB Statement April 2015 No. 68, Pension Obligation implementation. GAAP Manual | GAAP Adjustments and Reclassification Entries – Liabilities: Pension Obligation | June 30, 2015