Pension Accounting – Bean

advertisement

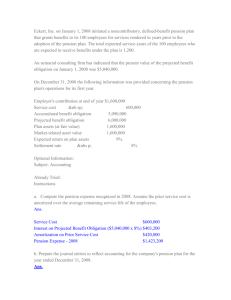

California Society of Municipal Finance Officers Pension Accounting and Financial Reporting: A Work in Progress The views expressed in this presentation are those of Mr. Bean. Official positions of the GASB are determined only after extensive due process and deliberation. What Was the Starting Point? Current standards were issued in 1994 Statement No. 25, Financial Reporting for Defined Benefit Pension Plans and Note Disclosures for Defined Contribution Plans Statement No. 27, Accounting for Pensions by State and Local Governmental Employers GASB’s strategic plan calls for the periodic reexamination of major standards Focus of this session is on employer reporting 2 Where Have We Been? GASB staff research Invitation to Comment Neutral document Issued in March 2009 Preliminary Views Conducted during 2006-2008 Recommended that the Board should place all pension accounting and financial reporting issues on the table Board document Issued June 2010 Exposure Drafts Employers and Plan Issued June 2011 3 Fundamental Approach Balance between a point-in-time measure of the employer’s obligation to employees and the measures over time of the cost to taxpayers of providing governmental services Viewed in the context of an ongoing, career-long employment relationship Accounting-based versus funding-based proposals 4 Measurement Measurement Approach Illustrated 1) Project Benefits 25 40 62 2) Discount 80 Present Value 3) Attribution 6 Actuarial Assumptions Selection of all actuarial assumptions should be made in accordance with Actuarial Standards of Practice (unless specific guidance is provided by the GASB). 7 Projection of Future Benefit Payments The effects of the following projected future changes should be included in the projection of benefits for the purpose of measurement of the pension liability: Automatic cost-of-living adjustments (COLAs) Projected future ad hoc COLAs, referring in this context to COLAs that are dependent upon a decision to grant by a responsible authority, when those adjustments are substantially the same as automatic COLAs – – – The historical pattern of granting the changes The consistency in the amounts of the changes or in the amounts of the changes relative to, for example, a defined cost-of-living or inflation index Whether there is evidence to conclude that changes might not continue to be granted in the future despite what might otherwise be a pattern that would indicate such changes are substantively automatic. Projected future salary increases in circumstances in which the pension benefit formula is based on future compensation levels Projected future service credits, both in determining an employee’s probable eligibility for benefits and in the projection of benefits in circumstances in which the pension benefit formula is based on years of service. 8 Discount Rate Should be a single rate that reflects: – The long-term expected rate of return on plan investments to the extent that current and expected future plan net assets available for pension benefits are projected to be sufficient to make benefit payments – A high-quality municipal bond index rate beyond the point at which plan net assets available for pension benefits are projected to be fully depleted If employer contributions to the plan are expected to be held for a short time such that there would be little or no opportunity to invest the assets (for example, if contributions are made on a pay-as-you-go basis), projected benefit payments that are expected to be paid by those contributions should be discounted at the high-quality municipal bond index rate 9 Crossover Point The projection of future employer contributions for purposes of determining a discount rate should not include contributions intended to fund the service costs of future employees or the contributions of future employees. 10 Projection of Contributions In circumstances in which either (1) contributions are subject to statutory or contractual requirements or (2) a formal, written policy related to employer contributions exists, professional judgment should be applied to project future employer contributions Application of such judgment should consider the employer’s most recent five-year contribution history as a key indicator of future contributions and should reflect all other known events and conditions In the event that no statutory or legal contribution requirement or formal, written contribution policy exists, projected contributions should be limited to an average of contributions over the most recent five-year period, potentially modified based upon the consideration of subsequent events The basis for the average (for example, percentage of pay contributed, or percentage of actuarially determined contributions) will be a matter of professional judgment Attribution Method Single allocation method Based on entry age normal principles The definition will exclude the use of approaches in which measurements of service costs are not individually based. Level percentage of payroll Over periods beginning in first period in which the employee’s services lead to benefits under the plan (without regard to conditional service-related provisions such as vesting) and ending in last period of the employee’s service 12 Measurement of Plan Assets Plan net assets held in trust for pension benefits component of the employer’s net pension liability should be measured in the same way that it is measured in the statement of plan net assets, including measurement of investments at fair value. 13 Recognition To Be Deliberated at March Meeting Statement of Net Position Entire net pension liability reported Deferred inflows or deferred outflows may be reported based on expense recognition Expense Recognition Service cost attributed to the current period should be included in current-period pension expense Interest on the total pension liability should be included in current-period pension expense Interest should be calculated using the discount rate used in calculating the beginning total pension liability Changes in benefit terms on the total pension liability should be included in pension expense in the period of the change 16 Expense Recognition Differences between expected and actual experience with regard to economic or demographic factors (differences between expected and actual experience) and the effects of changes of assumptions about future economic or demographic factors (changes of assumptions) should be recognized as follows: Inactive (including retired) employees—effects should be included in pension expense in the period of the change Active employees—effects should be recognized using a systematic and rational method over a closed period that is representative of employees’ expected remaining service lives as of the beginning of the period in which the change occurred. Length of the period should be an average expected remaining service life of the active employees with which the change is associated, with weighting to approximate the aggregate result that would be obtained if such changes in each active employee’s total pension liability were recognized separately over that employee’s expected remaining service life. Expense Recognition Projected earnings on plan investments should be included in pension expense in the period in which the earnings are projected to occur. Differences between projected and actual earnings on plan investments should be recognized using a systematic and rational method over a closed five-year period, beginning in the period in which the difference occurred. Expense Recognition Differences between expected and actual experience with regard to economic or demographic factors or changes of assumptions about the expected future behavior of economic and demographic factors should be recognized as expense over a period representative of employees’ expected remaining service lives, with the following requirements: To the extent that changes relate to past service of inactive, including retired, employees, the effects of such changes should be recognized as pension expense immediately in the period of change To the extent that such changes relate to past periods of service of active employees, the effects should be recognized using a systematic and rational method over a closed period The period should be an average expected remaining service life of the employees with which the change is associated, with weighting to approximate the result that would be obtained of such changes were recognized over each active employee’s service life 19 Disclosures To Be Deliberated At April Meeting Disclosures • • • General information Assumptions used in measurement Details about changes in the net pension liability, pension expense, and deferred outflows of resources 21 General Information Name of the plan through which benefits are provided Identification of the public employee retirement system or other entity that administers the plan Identification of the plan as: Single-employer Agent multiple-employer Cost-sharing multiple-employer A brief description of the benefit provisions, including Types of benefits, Key elements of the benefit formula(s), and Authority under which benefit provisions are established or may be amended 22 General Information The number of employees covered by the plan, separately identifying numbers of the following: Retired employees and their beneficiaries currently receiving benefits Inactive employees entitled to but not yet receiving benefits Active employees Whether the pension plan issues a stand-alone financial report, or is included in the report of a public employee retirement system or another entity, and, if so, how to obtain the report 23 Assumptions Used In Measurement Assumptions in respect of: Salary, Inflation Postemployment Discount rate benefit increases Different rates, if contemplated for different periods Date(s) of experience studies and tables on which significant assumptions are based 24 Discount Rate Assumptions Assumptions made about contributions of the employer and of employees and about other projected cash flows into and out of the plan Expected rate of return 25 Discount Rate—Expected Rate of Return Expected rate of return on plan investments Description of how the expected rate of return on plan investments was determined, including Assumed asset allocation of the portfolio Best estimate of the long-term expected real rate of return for each major asset class Discount Rate—Municipal Bond Rate If the discount rate incorporates a municipal bond index rate Tax-exempt municipal bond index rate Index selected (20-year maturity) Reasons for selection of that index Periods of projected benefit payments to which the expected rate of return and the municipal bond index rate were applied to determine the discount rate Discount Rate—Sensitivity Analysis The effects on the current-period net pension liability of a 1-percentage-point increase and a 1-percentage-point decrease in the discount rate Changes in Net Pension Liability For the current period, a schedule of changes in the net pension liability that separately discloses (a) the beginning and ending balances of the total pension liability, plan net assets held in trust for pension benefits, and the net pension liability and (b) the effects of the following on those items during the period: Service cost Interest Benefit changes related to past services Experience losses (gains) Changes in assumptions Contributions—employer (direct) Contributions—employer (other entities on behalf of the employer) Contributions—employees Net investment income Refunds of contributions Benefits paid Other changes, separately identified if individually significant 29 Changes in Net Pension Liability Brief description of changes of assumptions that affect measurement of the total pension liability Brief description of changes of plan terms that affect the amount of benefits associated with employee services in past periods Basis for determination of actual employer contributions to the plan (the employer’s contribution policy), including identification of the authority under which employer contribution requirements are established or may be amended. If employer contributions to the plan include more than one contributor, disclosure of contributions by the employer from its own sources and contributions made on behalf of the employer by another entity Basis for determination of employee contributions to the plan, including identification of the authority under which employee contribution requirements are established or may be modified 30 Pension Expense Separate identification of the following components: Service cost Interest on beginning total pension liability Current-period benefit changes Current-period experience losses (gains) Current-period changes in assumptions Employee contributions Expected earnings on plan investments Differences between actual and expected investment returns not qualified for deferral Amortization of beginning deferred pension inflows Amortization of beginning deferred pension outflows Other, with separate display by type of changes if significant The amortization period or periods for different types of changes in the net pension liability that occurred in the current period 31 Deferred Inflows and Deferred Outflows Separate reconciliations of beginning and ending balances of (a) deferred pension outflows and (b) deferred pension inflows, each with separate identification of the following categories of changes: Current-period benefit changes Current-period experience gains (losses) Current-period changes of assumptions Earnings on plan investments above (below) expectation Amortization of beginning deferred pension inflows (outflows) 32 Required Supplementary Information To Be Deliberated At April Meeting Required Supplementary Information 10-year schedules for all governments, regardless of type of plan (plus notes): Changes in the net pension liability by source Collective level for cost-sharing employers Components of the net pension liability and ratios: plan net position ÷ total pension liability; net pension liability ÷ covered-employee payroll Collective and individual level for cost-sharing Contribution information, if a government has an actuarially determined contribution: actuarially calculated contribution – actual contributions; contributions ÷ payroll 34 Illustration: Changes in NPL Note: Only 5 years are presented here; 10 years of information would be required 35 Illustration: NPL Components/Ratios Note: Only 5 years are presented here; 10 years of information would be required 36 Illustration: Contribution-related Information Note: Only 5 years are presented here; 10 years of information would be required 37 Questions? Web site—www.gasb.org 38