Preparing a JV

advertisement

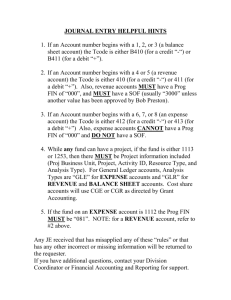

GENERAL ACCOUNTING CONTROLLER’S OFFICE http://controller.unlv.edu/general_accounting.html WHAT IS A JV? • JV stands for “Journal Voucher” • A journal voucher is an accounting record that provides written authorization for a financial transaction. • Used to record any financial transaction that cannot be processed on another document type (IDR’s, Payment Vouchers, Cash Receipts, Purchase Orders). • Some common examples of when a JV would be used: • Reassignment of expenses/revenues • Corrections of posting errors • Posting wire disbursements/receipts from the bank • Revenue or expense distributions BASICS OF ACCOUNT NUMBERS There are 3 components of an account number: 1. Fund • The basic accounting entity used for budgeting, revenue & expenditure control. • UNLV uses four digit fund numbers that always begin with the number “2” to denote our institutional code. (Ex: 2221) 2. Agency (AGCY) • Code used to denote organizational groupings and associated budget responsibilities. • Example: All accounts associated with the College of Engineering have an agency code of 254. 3. Organization (ORG) • Code that represents a sub-division of an agency. • Example: The account for the department of Civil & Environmental Engineering has an organization code of 49FB. When the three parts of the account number are put together, it will look like this: 2221254-49FB. An account number cannot be used on its own. In financial transactions, it must be paired with an Object/Sub-object code (for expenses), a Revenue/Subrevenue code, or a Balance Sheet Account. BASICS OF ACCOUNT NUMBERS Object/Sub-Object Codes • Object codes represent the different classifications of expenses (Ex: 30 – General Operations) • Sub-Object codes represent a specific type of expense within the Object Code (Ex: 75 – Printing Expense) Revenue/Sub-Revenue Codes • Revenue codes represent the different classifications of revenues (Ex: 78 – Sales/Service of Educational Activities) • Sub-Revenue codes represent a specific type of revenue within the Revenue Code (Ex: 14 – Facility Use Fees Revenue) Balance Sheet Accounts • These are accounts that are not a revenue or expense. For example, Cash is a balance sheet account. Other examples include: • Accounts Receivable • Accounts Payable • Accrued Liabilities • NOTE: A balance sheet account cannot be used in conjunction with an Object/Sub-Object code or a Revenue/Sub-Revenue code. For a complete listing of Object, Sub-Object, Revenue, and Sub-Revenue codes, please refer to the General Accounting website. TYPES OF JV’s There are several different types of JV’s: 2FA • The most common type of JV. This code is used for all JV’s that do not fall into one of the below categories. Things such as expense reassignments, bank wire claims, revenue distributions, etc. will use this type of JV. 2GC • These are prepared by Grants & Contracts and generally involve a transaction using a grant account (Funds 2300-2399). 2IC • These are used to distribute the revenues from Indirect Cost Recovery across multiple accounts. 2PYC/2PYT • These come from the Payroll system and are used to post monthly salaries/wages/fringe benefits. 2PC • These are used to post monthly Pcard transactions. 2TMC/2TMCBC/2TMCCHBK • These are used by the Thomas & Mack Center to post transactions. JV NUMBERING The basic format of a JV number is as follows: 2 FA 00012345 (Institutional code) (JV type) (Number) • • • UNLV’s institutional code is 2 The document type is an FA The number is 0012345 When the transaction posts to an account, the JV number will be shown as 2FA00012345. There are 11 characters in a JV number. This is a standard in Advantage. As a result, the amount of characters in the Number section will change based on the length of the JV type. Unlike IDR’s, there is no fiscal year distinction in the JV document number. Some examples of JV Numbers: • 2FA00057590 • 2PC10070560 • 2PYC0015248 • 2GC00009960 • 2TMCBC00102 NOTE: All JV numbers are automatically assigned by the Controller’s Office when the document is entered into Advantage PREPARING THE JV STEP 1: Download the JV Template file from the General Accounting website located at: http://controller.unlv.edu/general_accounting.html STEP 2: Determine the Fund/Agency/Org of the accounts will be used (ex: 2101-213-1210) STEP 3: Determine which Objects/Sub-Objects or Revenues/Sub-Revenues to use. STEP 4: Determine which Account Type to use based on your selection of Object/Revenue code. STEP 5: Complete the JV template (example on next slide) STEP 6: Have an authorized signer for your area sign the JV to indicate approval STEP 7: Submit the JV to General Accounting for processing PREPARING THE JV FIELDS TO BE COMPLETED ON THE JV (explanations on following slides) PREPARING THE JV SECTION 1 - HEADER 1. JV Date • 2. Agency • 3. This is the fiscal month & fiscal year in which the JV is to be processed. Fiscal month 01 is July, 02 is August, 03 is September, and so on. This field is formatted as FM/FY. • For example, a JV to be processed in December 2014 would have an accounting period of 06/15. Budget FY • 7. Use this section to give a brief summary of what type of transaction is occurring. Example: Reassign Expenses Acct. Period • • • 6. This section will stay blank because the number will be auto-assigned by the Controller’s Office during processing. Comments • 5. The agency code for the account credited (this can be found in the AGCY column on line 2 – see #14 below) Document ID • 4. The date the JV is being prepared. The fiscal year in which the document is being processed. Action • The action will always be the letter “E”. This stands for the “execute” command in Advantage. PREPARING THE JV SECTION 2 - BODY 8. Account Type (Debit Account) • • 9. This is a two-digit code that is determined by what type of account is being used (revenue/expense/balance sheet) • Account Type 01 – Balance Sheet Accounts beginning with “0” • Account Type 02 – Balance Sheet Accounts beginning with “1” • Account Type 22 – Expenses (Object code is 52 or under) • Account Type 31 – Revenues (Object code is 53 or over) For example, if you are using the 30 object code for one of the accounts, the Account Type would be 22. FUND—AGCY—ORGN (Debit Account) • In this section, you will enter the Fund/Agency/Organization of your account number 10. OBJ/RSRC—SOBJ/SREV (Debit Account) • • In this section, you will enter the Object/Sub-object or Revenue/Sub-Revenue for your account. These codes are used to represent expenses and revenues NOTE: If you use an OBJ/SOBJ or RSRC/SREV, you cannot use a balance sheet account in Step 11. 11. BACC (Debit Account) • • This section is used if you are debiting a four digit Balance Sheet account instead of a revenue/expense. NOTE: If you use a balance sheet account, you cannot use an OBJ/REV and SOBJ/SREV code in Step 10. 12. Description (Debit Account) • A short description of the transaction. When possible, include a reference document number when reassigning expenses. • Example: “Reassign Office Supplies – 2PC10070560” • There is a limit of 30 spaces to enter the description in Advantage, so please abbreviate when possible. 13. Debit • Enter the dollar amount of the debit to this account. PREPARING THE JV SECTION 2 – BODY (cont.) 14. Account Type (Credit Account) • • This is a two-digit code that is determined by what type of account is being used (revenue/expense/balance sheet) • Account Type 01 – Balance Sheet Accounts beginning with “0” • Account Type 02 – Balance Sheet Accounts beginning with “1” • Account Type 22 – Expenses (Object code is 52 or under) • Account Type 31 – Revenues (Object code is 53 or over) For example, if you are using the 30 object code for one of the accounts, the Account Type would be 22. 15. FUND—AGCY—ORGN (Credit Account) • In this section, you will enter the Fund/Agency/Organization of your account number. 16. OBJ/RSRC—SOBJ/SREV (Credit Account) • • In this section, you will enter the Object/Sub-object or Revenue/Sub-Revenue for your account. These codes are used to represent expenses and revenues NOTE: If you use an OBJ/SOBJ or RSRC/SREV, you cannot use a balance sheet account in Step 11. 17. BACC (Credit Account) • • This section is used if you are crediting a four digit Balance Sheet account instead of a revenue/expense. NOTE: If you use a balance sheet account, you cannot use an OBJ/REV and SOBJ/SREV code in Step 16. 18. Description (Credit Account) • You can use the same description here that you used in Step 12 19. Credit • Enter the dollar amount of the credit to this account. NOTE: Repeat Steps 8-19 if you have more than one debit and one credit for the transaction. PREPARING THE JV SECTION 3 – FOOTER 20. Explanation • In this section, please provide a detailed description of the transaction and why it is occuring. 21. Prepared By • Sign the preparer’s name and enter the date prepared in this section. 22. Approval • Have an account manager from your area sign the JV and enter the date approved in this section. 23. Copies To • • List the names of employees that should receive a copy of the JV in this section. NOTE: This section is not required. Please continue to the next few slides to see some examples of completed JV’s as well as some helpful reminders. COMPLETED JV EXAMPLE EXAMPLE: Reassigning an expense to another account. EXPLANATION: In this example, the Pcard charge was originally posted to account 2101-213-1210-30-26. Since it posted to an expense line (30), account 2101-213-1210-30-26 will be credited in order to zero out this charge. Debits posted to expense lines represent an increase to the expense, so in this transaction a credit is used to reduce the expense. COMPLETED JV EXAMPLE EXAMPLE: Reversing an IDR that posted incorrectly and reassigning to proper account. EXPLANATION: In this example, the IDR document 25TV00205 was incorrectly processed using VT lines (transfer of cash) instead of using the 30 expense line. To correct, we debit account 2221213-1205-VT since it is a revenue account. Increases in revenue accounts are posted as credits so we would use a debit to reverse the posting. Likewise, we credit the expense on line 2 to show the reversal. We then repost the correct entry on lines 3 and 4. When reversing documents, show the full document reversal followed by the correct posting. This helps to create an audit trail. COMPLETED JV EXAMPLE EXAMPLE: Claiming a wire that posted to UNLV’s Bank of America account. EXPLANATION: In this example, the JV is recording the receipt of cash (in the form of a wire (ACH) payment) that has posted to UNLV’s bank account. The debit for this transaction would be to Balance Sheet account 0001, which is the account used to record receipts of cash. The credit for this transaction is to the 81 revenue line of account 2221-213-1210. The 0001 Cash account is an asset on the balance sheet, and debits increase asset accounts. The 81 line is a revenue, and credits increase revenue accounts. Therefore, we show the transaction as an increase (debit) to cash and an increase (credit) to revenue. REMINDERS FOR JV’s • REMEMBER: For all JV’s, the amount in the Debits column must equal the amount in the Credits column so that the transaction is balanced. • Please make sure that all lines contain a full account number including: • Fund – Agency – Organization – Object/Revenue – Sub-object/Sub Revenue or Balance Sheet Account • Example: 2101-213-1210-30-13 2101-213-1210 BS Acct 1001 • Check the budgets for all accounts to ensure that: • Enough funds are available • The accounts have a budget line established for the Object/Revenue codes being used in the transaction. • Negative Amounts: • You cannot enter a negative amount in the debit or credit column of a JV. Example -500.00. • If there is a negative amount in an expense line that is being transferred, it means that the balance is actually a credit. In order to clear the credit, you will need to debit the expense. • If there is a negative amount in a revenue line that is being transferred, it means that the balance is actually a debit, so you will need to credit the revenue account to clear the negative. CHECKING THE STATUS OF A JV In Data Warehouse, you can use the Balance and Activity report (located under “Reports” “Business Reports”) • In the box circled below, enter the Fund-Agency-Org of the account number that was to be debited/credited on the JV and press Continue CHECKING THE STATUS OF A JV Click on the underlined number in Expenditures Year-to-Date column for the Object that is being charged. For revenue accounts, see the next slide. This will show a listing of all expenses that have posted to that Object code for the year. If the JV has been processed, you will see it on this report. CHECKING THE STATUS OF A JV Click on the underlined number in Revenues Year-to-Date column for the Revenue that is being charged. This will show a listing of all revenues that have posted to that Revenue code for the year. If the JV has been processed, you will see it on this report. QUESTIONS If you have any questions on JV preparation, please feel free to contact General Accounting at extension 53957 and we will be happy to assist you. Please refer to our website at http://controller.unlv.edu/general_accounting.html for more informational presentations that may be of assistance.