Chapter 19 Reporting and Analyzing Cash Flows

advertisement

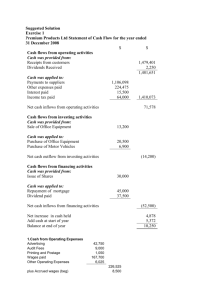

Chapter 19 Reporting and Analyzing Cash Flows True / False Questions The purpose of the statement of cash flows is to report the major items comprising cash receipts and cash payments during a period. TRUE The statement of cash flows only measures outflows of cash during a period. FALSE Investments must be within 6 months of their maturity dates to be classified as cash equivalents. FALSE The statement of cash flows explains the difference between the beginning and ending balances of cash and cash equivalents. TRUE Internal users of the statement of cash flows use cash flow information to plan day-today operating activities and make long-term investments. TRUE Many business decisions are based on cash flow evaluations. TRUE The statement of cash flows helps financial statement users evaluate a company's earnings performance at a point in time. FALSE Decisions on whether a company can pay its existing debts as they mature can be evaluated by looking at the company's statement of cash flows. TRUE On the statement of cash flows, business operations are classified as operating, investing, or financing activities. TRUE Cash outflows to repurchase shares is an example of a cash flow from a financing activity. TRUE 19-1 Financing activities include (a) the purchase and sale of long-term assets, (b) the purchase and sale of trading investments, and (c) lending and collecting on loans. FALSE Cash dividends and interest received can only be considered cash inflows from investing activities. FALSE The full disclosure principle requires that noncash investing and financing activities be disclosed in a separate schedule attached to the statement of cash flows or in the accompanying notes. TRUE A noncash investing transaction should be disclosed as a note to the statement of cash flows. TRUE A purchase of land in exchange for shares is disclosed in a separate schedule attached to the statement of cash flows or in a note to the statement. TRUE Accounting standards require companies to include a statement of cash flows in a complete set of financial statements. TRUE The statement of cash flows explains how transactions and events impact the end-ofperiod cash balance to produce the end-of-period cash balance. FALSE The increase or decrease in cash equals the current period's cash balance minus the prior period's cash balance. TRUE The direct method of preparing the statement of cash flows separately lists each major item of operating cash receipts and each major item of operating cash payments. TRUE Information to prepare the statement of cash flows usually comes from (a) comparative balance sheets, (b) current income statements, and (c) additional information. TRUE The indirect method for preparation of the statement of cash flows calculates the net cash inflows (outflows) from operating activities by adjusting accrual net income to a cash basis. TRUE Firms have the option of using either the direct or indirect method to prepare the statement of cash flows. TRUE 19-2 Bad debts expense is an item that does not provide or use cash. TRUE Decreases in non-cash current assets are added to net income. TRUE Most acquisitions of property, plant and equipment are reported on the statement of cash flows as cash used by investing activities. TRUE Both the direct and indirect methods yield the same net cash flow provided (used) by investing activities. TRUE Noncash operating expenses are added back to net income when preparing the investing section of the statement of cash flows using the indirect method. FALSE The sale of equipment increases investing cash flows. TRUE Reporting of financing activities is the same under the direct and indirect methods. TRUE Investing activities include: (a) the purchase and sale of long-term assets, (b) lending and collecting on notes receivable, (c) the purchase and sale of investments other than cash equivalents. TRUE A change in the amount of retained earnings can be due to payment of cash dividends. TRUE Multiple Choice Questions The statement of cash flows reports: A. Assets, liabilities, and owners' equity. B. Revenues, gains, expenses, and losses. C. Cash inflows and outflows for an accounting period. D. Owners' equity, net income, and dividends. E. Cash inflows and outflows for an accounting period and owners' equity, net income, and dividends. 19-3 The statement of cash flows reports: A. Operating activities. B. Financing activities. C. Investing activities. D. Noncash financing and investing activities. E. All of these answers are correct. A cash equivalent is an investment that: A. Is readily convertible to a known amount of cash. B. Is subject to an insignificant risk of changes in value. C. Is within 3 months of its maturity date. D. Is highly liquid. E. All of these answers are correct. The statement of cash flows is: A. Another name for the statement of financial position. B. A financial statement that presents information about what happened to equity during a period. C. A financial statement that reports the cash inflows and outflows for an accounting period. D. A financial statement that lists the types and amounts of assets, liabilities, and equity of a business on a specific date. E. A financial statement that lists the types and amounts of the revenues and expenses of a business. Managers use cash flow predictions to: A. Make decisions about acquiring new property, plant and equipment. B. Insource or outsource production of a product. C. Keep or eliminate a product line. D. Maintain or downsize a department. E. All of these answers are correct. Cash flows from selling long term investments are reported in the statement of cash flows as: A. Operating activities. B. Financing activities. C. Investing activities. D. Noncash activities. E. Not reported. 19-4 Cash flows from cash dividends and interest received are reported in the statement of cash flows as: A. Operating activities. B. Financing activities. C. Investing activities. D. Noncash activities. E. Not reported. The purchase of long-term assets by issuing a note payable is reported on the statement of cash flows in the: A. Operating section. B. Financing section. C. Investing section. D. Notes to the statement of cash flows. E. Both financing and investing sections. Noncash investing and financing activities may be disclosed: A. In a note to the statement of cash flows. B. In a separate schedule attached to the bottom of the statement of cash flows. C. In the investing section of the statement of cash flows. D. In the financing section of the statement of cash flows. E. In a note to the statement of cash flows or in a separate schedule attached to the bottom of the statement of cash flows. The appropriate statement of cash flow activity category for the purchase of equipment for cash is: A. Operating. B. Financing. C. Investing. D. Schedule of noncash investing or financing activity. E. Not reported on the statement of cash flows. The appropriate statement of cash flow activity category for the payment of wages is: A. Operating. B. Financing. C. Investing. D. Schedule of noncash investing or financing activity. E. Not reported on the statement of cash flows. 19-5 The appropriate statement of cash flow activity category for the issuance of common shares for cash is: A. Operating. B. Financing. C. Investing. D. Schedule of noncash investing or financing activity. E. Not reported on the statement of cash flows. Preparation of the statement of cash flows involves: A. Calculation of the net increase or decrease in cash. B. Calculation and reporting of net cash provided or used by operating activities. C. Calculation and reporting of net cash provided or used by investing activities. D. Calculation and reporting of net cash provided or used by financing activities. E. All of these answers are correct. A statement of cash flows should reconcile the differences between the beginning and ending balances of: A. Cash. B. Cash equivalents. C. Cash and cash equivalents. D. Working capital. E. Cash, cash equivalents, and long term investments. If a company borrows money from a bank, the interest paid should be reported on the statement of cash flows as a(n): A. Operating activity. B. Investing activity. C. Financing activity. D. Noncash investing and financing activity. E. Cannot determine from information given. Investing activities include: A. Purchase of long-term assets. B. Lending and collecting on notes receivable. C. Sale of equity investments. D. Sale of long-term assets. E. All of these answers are correct. 19-6 Which of the following items is reported in the body of the statement of cash flows? A. Declaration of a cash dividend. B. Payment of a cash dividend. C. Declaration of a share dividend. D. Payment of a share dividend. E. Share split. Acquisitions of long-term assets: A. Have no impact on cash flows. B. Are investing activities. C. Can involve cash outflows. D. Are investing activities and can involve cash outflows. E. Have no impact on cash flows and are investing activities. Changes in notes payable, non-current liabilities, and equity accounts are usually used in calculating and reporting: A. Cash flows from investing activities. B. Cash flows from financing activities. C. Cash flows from operating activities. D. Non-cash financing activities. E. Non-cash balance sheet accounts. Using the indirect method to calculate the net cash provided (or used) by operating activities, net income is adjusted for: A. Gains and losses from investing and financing activities. B. Revenues and expenses that did not provide or use cash. C. Changes in noncash current assets and current liabilities related to operating activities. D. All of these answers are correct. E. Gains and losses from investing and financing activities and revenues and expenses that did not provide or use cash. Using the indirect method to calculate net cash provided (or used) by operating activities, which of the following is subtracted from net income? A. Decrease in income taxes payable. B. Depreciation expense. C. Amortization of intangible assets. D. Bad debts expense. E. None of these answers is correct. 19-7 The indirect method for preparation of the operating activities section of the statement of cash flows involves adjustments: A. For income statement items involving operating activities that do not affect cash inflows or outflows. B. To eliminate gains and losses resulting from investing and financing activities. C. For changes in noncash current assets and current liabilities. D. For income statement items involving operating activities that do not affect cash inflows or outflows and for changes in noncash current assets and current liabilities. E. All of these answers are correct. Use the indirect method to calculate the net cash provided (or used) by operating activities based on the following information: A. $(500). B. $-0-. C. $17,100. D. $(7,500). E. $15,500. The first item in the operating activities section for a statement of cash flows prepared according to the indirect method is: A. Cash. B. Cash received from customers. C. Increase (decrease) in accounts receivable. D. Net income. E. Adjustments to net income. 19-8 Essay Questions For each of the following items, indicate whether it would be classified as an (O) operating activity, as an (I) investing activity, as a (F) financing activity, or as a (N) noncash financing and investing activity. _______ (1) Received dividends from shares owned in another company. _______ (2) Collected accounts receivable from customers. _______ (3) Issued bonds payable. _______ (4) Paid wages to employees. _______ (5) Purchased treasury shares. _______ (6) Sold equipment. _______ (7) Purchased land in exchange for a note payable. _______ (8) Paid dividends. _______ (9) Received interest. _______ (10) Sold shares in another company. (1) O (2) O (3) F (4) O (5) F (6) I (7) N (8) F (9) O (10) I For each of the following items, indicate whether it would be classified as either an (O) operating activity, an (I) investing activity, a (F) financing activity, or a (N) noncash financing and investing activity. _______ (1) Cash sales. _______ (2) Sale of shares of another company. _______ (3) Signed a note payable. _______ (4) Purchased supplies. _______ (5) Paid an account payable. _______ (6) Purchased a warehouse in exchange for company shares. _______ (7) Paid interest on a note payable. _______ (8) Sold treasury shares. _______ (9) Purchased equipment. _______ (10) Purchased shares in another company in exchange for a building. (1) O (2) I (3) F (4) O (5) O (6) N (7) O (8) F (9) I (10) N 19-9