Financial Institutions and Markets

advertisement

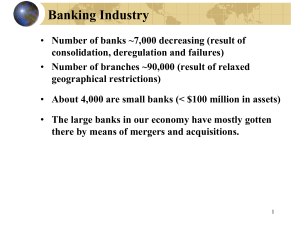

Nut Khorn Term II Financial Institutions and Markets (1) Securities firms provide a wide variety of functions in financial markets. o Broker function Execute securities transactions between two parties Charge a fee in the form of a bid-ask spread o Investment banking function Underwrite newly issued securities o Dealer function Securities firms make a market in specific securities by adjusting their inventory (4) Mutual funds financial institutions that pool financial resources of individuals and companies and invest those resources in diversified portfolios of asset. o Sell shares to surplus units o Use funds to purchase a portfolio of securities Some focus on capital market securities (e.g., stocks or bonds) Money market mutual funds concentrate on money market securities A mutual fund is a professionally managed type of collective investment scheme that pools money from many investors to buy stocks, bonds, short-term money market instruments, and/or other securities. In the United States, a mutual fund is registered with the Securities and Exchange Commission (SEC) and is overseen by a board of directors (if organized as a corporation) or board of trustees (if organized as a trust). The board is charged with ensuring that the fund is managed in the best interests of the fund's investors and with hiring the fund manager and other service providers to the fund. The fund manager, also known as the fund sponsor or fund management company, trades (buys and sells) the fund's investments in accordance with the fund's investment objective. A fund manager must be a registered investment advisor. Funds that are managed by the same fund manager and that have the same brand name are known as a "fund family" or "fund complex". The Investment Company Act of 1940 (the 1940 Act) established three types of registered investment companies or RICs in the United States: open-end funds, unit investment trusts (UITs); and closed-end funds. Recently, exchange-traded funds (ETFs), which are open-end funds or unit investment trusts that trade on an exchange, have gained in popularity. While the term "mutual fund" may refer to all three types of registered investment companies, it is more commonly used to refer exclusively to the open-end type. Hedge funds are not considered a type of mutual fund. While they are another type of commingled investment scheme, they are not governed by the Investment Company Act of Compiled By Nut khorn Page 1 1940 and are not required to register with the Securities and Exchange Commission (though many hedge fund managers now must register as investment advisors). Mutual funds are not taxed on their income as long as they comply with certain requirements established in the Internal Revenue Code. Specifically, they must diversify their investments, limit ownership of voting securities, distribute most of their income to their investors annually, and earn most of the income by investing in securities and currencies.[2] Mutual funds pass taxable income on to their investors. The type of income they earn is unchanged as it passes through to the shareholders. For example, mutual fund distributions of dividend income are reported as dividend income by the investor. There is an exception: net losses incurred by a mutual fund are not distributed or passed through to fund investors. Outside of the United States, mutual fund is used as a generic term for various types of collective investment vehicles available to the general public, such as unit trusts, open-ended investment companies, unitized insurance funds, Undertakings for Collective Investment in Transferable Securities, and SICAVs. Advantages of mutual funds Mutual funds have advantages compared to direct investing in individual securities.[3] These include: Increased diversification Daily liquidity Professional investment management Ability to participate in investments that may be available only to larger investors Service and convenience Government oversight Ease of comparison Disadvantages of mutual funds Mutual funds have disadvantages as well, which include [4]: Fees Less control over timing of recognition of gains Less predictable income No opportunity to customize (6) Role of nondepository financial institutions o Nondepository institutions generate funds from sources other than deposits o Finance companies Obtain funds by issuing securities Compiled By Nut khorn Page 2 Lend funds to individuals and small businesses Government or private organization (such as building society, insurance company, investment trust, or mutual fund or unit trust) that serves as an intermediary between savers and borrowers, but does not accept time deposits. Such institutions fund their lending activities either by selling securities (bonds, notes, stock/shares) or insurance policies to the public. Their liabilities (depending on the liquidity of the liability) may fall under one or more money supply definitions, or may be classified as near money. The economy works best when there is money and credit available to finance business or consumer purchases or investments. When money is limited, such as during the 2007 – 2009 credit crisis, businesses can't finance their operations nor invest in new projects, so unemployment rises, which causes people to curtail their spending which further contracts business. Tax receipts fall, so governments cut back on their spending, adding to the recession. Most of the money and credit readily available to the economy comes from financial intermediaries. Depository institutions—banks that accept deposits—contribute to the economy by lending much of the money saved by depositors. However, deposits do not provide all of an economy's funding, since only the wealthy save a significant amount of money and most of it is not in low-interest paying deposits which are taxable as ordinary income. The wealthy put most of their money into assets such as stocks, real estate, and municipal bonds, which not only offer greater returns, but the returns are often taxed less than ordinary income. People who are not wealthy do not save very much, at least in the United States, because they need the money for everyday wants and needs. Although wealthy individuals have a lot more money than lower-income individuals, there are many more people in the lower-income classes; hence, the aggregate of the money held by the lower-income classes is greater than the aggregate held by the wealthy. This greater aggregate wealth of the lower-income people is made available to the economy through financial nondepository institutions, which are financial intermediaries that do not accept deposits but do pool the Compiled By Nut khorn Page 3 payments of many people in the form of premiums or contributions and either invest it or provide credit to others. Hence, nondepository institutions form an important part of the economy. These institutions receive the public's money because they offer other services than just the payment of interest. They can spread the financial risk of individuals over a large group, or provide investment services for greater returns or for a future income. Nondepository institutions include insurance companies, pension funds, securities firms, government-sponsored enterprises, and finance companies. There are also smaller nondepository institutions, such as pawnshops and venture capital firms, but they constitute a much smaller portion of sources of funds for the economy. Insurance Companies Insurance companies protect their customers from the financial distress that can be caused by unforeseen events, such as accidents or premature death. They pool the small premiums of the insured to pay the larger claims to those who have losses. The premium payments are regular while the losses are irregular, both in timing and amount. An insurance company can profit because it can accurately estimate the payment of claims over a large group by using statistics and it can invest its surplus for greater returns, which helps to lower premiums to be competitive. Like banks, insurance companies are confronted with the informational asymmetry problems of adverse selection and moral hazard. An insurance company solves the problem of adverse selection by screening applicants—verifying information in the application, checking the applicant's history, and by applying restrictive covenants in the insurance contract, such as not covering a pre-existing condition. Adverse selection is also reduced by grouping— placing the insurance applicant into specific classes where there is a difference in claims history for the group, then Compiled By Nut khorn Page 4 charging the appropriate premium. One controversial example is the use of credit scores for determining insurance premiums, since several studies have shown that people with lower credit scores file more claims than those with higher scores. The solution to moral hazard differs, depending on the type of insurance offered. There are 2 major types of insurance: property and casualty insurance and life insurance. How the premiums are invested depends on what type of insurance the company offers, which determines the amount of liquidity it needs. Property And Casualty Insurance Property and casualty insurance offers financial protection against damage or loss to property or people caused by accidents, natural disasters, or from the action of others. The most common type of this insurance isauto insurance, since it is legally required by every driver in every state. Although losses can be estimated by using statistics over a large group, there is a larger standard deviation of risk because property and casualty insurance covers many more types of events, so claims can vary greatly in amount. Hence, these insurance companies must maintain liquidity by investing the premiums in short-term securities, most of which are money market securities that can be sold quickly at little cost and are very safe. Although there are several methods to reducing moral hazard, property and casualty insurers use the principle of indemnity, which is to pay for financial losses suffered by the insured— but no more. After all, if people could profit from insurance, that would motivate them to cause losses for profits. For this same reason, insurance companies will not pay for losses that are covered by other insurance or other forms of compensation. Life Insurance Compiled By Nut khorn Page 5 While the death of a single individual is an uncertain event, the number of deaths in a large group is very predictable. Furthermore, the amount of the claim for any single death is certain since it is specified in the contract. There isn't much of a moral hazard problem in life insurance because most people want to live and would not be able to benefit directly from the proceeds unless it is a whole life policy that also has a savings portion. However, this living benefit is limited by what the insured has paid in. The only real moral hazard to life insurance is the possibility that the insurance applicant is buying insurance to provide for his beneficiaries after he commits suicide. This moral hazard is reduced by a suicide clause—not paying for suicides within the 1st 2 years of the policy, or 1 year in some policies. The reasoning behind this is that most people who commit suicide are mentally ill, which is an affliction that should be covered, while the waiting period prevents someone who is suicidal from taking out a policy just before committing suicide. Because claim payments are more predictable, life insurance companies invest mostly in long-term bonds, which pay a higher yield, and some stocks. Their portfolios have a smaller stock portion because the reduction in liquidity caused by a stock market decline can last for years. Pension Funds Pension funds receive contributions from individuals and/or employers during their employment to provide a retirement income for the individuals. Most pension funds are provided by employers for employees. The employer may also pay part or all of the contribution, but an employee must work a minimum number of years to be vested—qualified to receive the benefits of the pension. Self-employed people can also set up a pension fund for themselves through individual retirement accounts (IRAs) or other types of programs sanctioned by the federal government. Compiled By Nut khorn Page 6 While an individual has many options to save for retirement, the main benefit of government-sanctioned pension plans is tax savings. Pension plans allow either contributions or withdrawals that are tax-free. For instance, for regular IRAs, contributions are tax-free, but withdrawals are taxed, while for Roth IRAs, contributions are taxed, but withdrawals are tax-free. As a consequence of the regular contributions and the tax savings, pension funds have enormous amounts of money to invest. And because their payments are predictable, pension funds invest in long-term bonds and stocks, with more emphasis on stocks for greater profits. Securities Firms Securities firms are companies that provide institutional support for the buying and selling of securities. Investment companies, brokerages, and investment banks are the major types of securities firms. Investment companies pool the investments of many people into a single portfolio that is managed by professional managers. Investment companies, such as mutual funds, provide expertise and economies of scale that small individual investors would not be able to afford otherwise. Brokerages provide an institutional framework that allows retail investors to invest in stocks, bonds, options, futures, and other financial instruments directly. Brokers provide trading software that allows traders to select their trades, and settlement and clearing services to effect the transactions. Investment banks help businesses and other organizations to sell their own stocks and bonds to the investing public. Investment banks offer advice to the issuer, register the securities with the Securities and Exchange Commission, and sell the securities to their customers. Federal Government-Sponsored Enterprises (GSEs) There are a number of government agencies or private corporations chartered by the federal government that also Compiled By Nut khorn Page 7 act as financial intermediaries. These agencies were created ad hoc by Congress to provide credit to specific constituencies that Congress has argued were not being addressed adequately by the free market. The largest of these include the Government National Mortgage Corporation (Ginnie Mae), the Federal National Mortgage Association (Fannie Mae), the Federal Home Loan Mortgage Corporation (Freddie Mac), the Student Loan Marketing Association (Sallie Mae), and the Farm Credit System. These agencies are all involved in providing credit to buy homes or farms, except for Sallie Mae, which provides student loans. Most of these agencies buy loans from private lenders, then they securitize the loans into asset-backed securities and sell them to the public. These agency securities are exempt from state and local taxes, and they were considered very safe, at least before 2008, since most investors believed that they had the implicit backing of the federal government, which has been demonstrated in September, 2008, when the federal government placed Fannie Mae and Freddie Mac under conservatorship, ousting its executives and turning over their loan portfolios to the Federal Housing Finance Agency. Finance Companies Finance companies provide loans to people or businesses using the issuance of short-term securities, especially commercial paper, as a source of funds. Consumer finance companies provide consumer loans and sometimes mortgages. They also provide the instant credit offered by so many retail stores, where the customer receives the item but doesn't have to pay for a stipulated amount of time. Business finance companies provide loans to businesses but are especially prominent in the equipment leasing business, where the finance company will buy equipment that a particular business wants, and lease it to the business. This saves the business the upfront purchase cost, and allows it to treat the equipment as a current deduction for taxes rather Compiled By Nut khorn Page 8 than as a capital expense that has to be depreciated over a number of years. Business finance companies also provide businesses with short-term liquidity by financing inventory until it is sold and with accounts receivable loans, which are short-term loans backed by accounts receivable. Sales finance companies finance specific types of major purchases or finance the purchases of a specific retailer. For instance, most of the financing provided by automobile dealers is provided by these companies, so that the potential buyer can buy right away. (10) Role of depository institutions o Depository institutions accept deposits from o surplus units and provide credit to deficit units Depository institutions are popular because: Deposits are liquid They customize loans They accept the risk of loans They have expertise in evaluating creditworthiness They diversify their loans Depository institutions (for simplicity, we refer to these as banks throughout this text) are financial intermediaries that accept deposits from individuals and institutions and make loans. The study of money and banking focuses special attention on this group of financial institutions, because they are involved in the creation of deposits, an important component of the money supply. These institutions include commercial banks and the so-called thrift institutions (thrifts): savings and loan associations, mutual savings banks, and credit unions. Depository institutions, which are usually just called banks, are categorized as such because their primary source of funding is the deposits of savers. Their savings accounts are insured by the Federal Deposit Insurance Corporation (FDIC) up to certain limits. Banks are further subcategorized depending on the markets they serve, their primary sources of funding, type of ownership, how they are regulated, and the geographic extent of their market. These categories of banks arose because they were established to serve different markets at different times. What state and federal regulations governed a particular Compiled By Nut khorn Page 9 bank also depended on its type, and whether it had a state or federal charter. States, especially, restricted the banks' ability to compete and to expand geographically. However, modern technology and deregulation are blurring these traditional distinctions, with categories overlapping even more than in the past. Savings Institutions Savings institutions, sometimes called thrift institutions, are banks that serve a local community. They take the deposits of local residents and lend the money back in the form of consumer loans, mortgages, and small business loans. Savings institutions include savings and loan institutions, savings banks, and credit unions. Most savings institutions are regulated by the Office of Thrift Supervision (OTS), which was created by the Financial Institutions Reform, Recovery and Enforcement Act of 1989 (FIRREA). The FIRREA empowered the OTS to enact rules and regulations for savings institutions, manage the Savings Association Insurance Fund (SAIF), which insures the deposits of savings institutions, and to charter federal savings banks and savings and loans associations. Prior to 1980, savings institutions were mostly limited to the residential mortgage market, but the Depository Institutions Deregulation and Monetary Control Act of 1980 deregulated banking by removing interest rate ceilings and allowing savings institutions to offer more services, including commercial and consumer lending. The Act also eliminated dollar limits on mortgages, allowed second mortgages, and eliminated the territorial restrictions on mortgage lending and permitted savings institutions to offer interest-paying Negotiable Order of Withdrawal (NOW) accounts—basically, checking accounts paying interest. Compiled By Nut khorn Page 10 Savings and Loan Associations (SLAs, S&Ls) first appeared in the 1800s so that factory workers could save money to buy a home. They were loosely regulated until the Great Depression, when Congress passed several major laws to shore up the banking industry and to restore the public's trust in them. Before 1980, SLAs were restricted to mortgages and savings and time deposits, but the Monetary Control Act extended their permitted activities to commercial loans, non-mortgage consumer lending, and trust services. Many S&Ls have been owned by depositors, which was their main source of funding—thus they were calledMutual Savings and Loans Associations or just Mutual Associations. Mutual S&Ls, like credit unions, used their earnings to lower future loan rates, raise deposit rates, or to reinvest while corporate S&Ls either reinvested profits or returned profits to their owners by paying dividends. Nowadays, most S&Ls are corporations, giving them access to additional capital funding to compete more successfully and to facilitate mergers and acquisitions. Savings banks (aka mutual savings banks, MSBs) began as mutual companies first chartered in 16 states, with most in New York and New Jersey, that were owned by the depositors and were restricted to mortgages. They were governed by a local board of trustees. When interest rates were limited by law, mutual savings banks distributed their earnings back to the depositors. The Garn-St. Germain Depository Institutions Act of 1982 gave savings banks the option of a federal charter and allowed them to convert to corporations, which many of them did since it extended their funding options and facilitated mergers and acquisitions. Credit unions are nonprofit depository institutions that are financial cooperatives owned by people belonging to a particular group, such as the employees of a particular company, a union, or a religious group, or who live in a Compiled By Nut khorn Page 11 specific area such as a county, and they are governed by a board of volunteers. Because they are nonprofits and owned by their customers, they charge lower loan rates and pay higher interest rates on savings, and they offer a wide variety of financial services for their owners. All credit unions with federal charters and most with state charters are regulated and insured by the National Credit Union Administration. Deposit insurance is provided by the National Credit Union Share Insurance Fund. Commercial Banks The primary business of commercial banks is to serve businesses, although with banking deregulation they have entered into the consumer business as well. Commercial banks provide the widest variety of banking services. In addition to savings accounts, checking services, consumer loans, commercial and industrial (C&I) loans, and credit cards, commercial banks may also offer trust services, trade financing, investment banking and management for corporations, governments and their agencies, and treasury services. Before 2005, deposits were insured by the Bank Insurance Fund (BIF), but it was merged with the SAIF, the fund used to insure thrifts, into a single fund—the Deposit Insurance Fund (DIF). Commercial banks are the largest banks, both in assets and in geographic extent. Community banks, however, are smaller commercial banks with assets of less than $1 billion that generally serve their immediate community of consumers and small businesses. Community banks are also the most numerous by a large margin. Some commercial banks, often called regional and superregional banks, cover a much wider geographic area and usually have assets in the hundreds of billions of dollars. They have many branches that extend into several states Compiled By Nut khorn Page 12 and many ATM machines at convenient locations throughout their area. Global banks also offer international services, such as letters of credit, and currency exchange. These larger banks use short-term borrowing in the money markets to supplement their deposits and often require loans from the smaller community banks. These correspondent banks have accounts at the larger banks, which facilitates the frequent transfers of funds with the big banks. Some banks— money center banks—borrow for their funding instead of relying on deposits. However, the recent credit crisis has forced money center banks to become depository institutions because they could not sell their commercial paper or bonds in financial markets that have been greatly diminished by investors' fear of defaults. Bank And Financial Holding Companies Many of the largest banks are actually bank holding companies, which is a company that controls 2 or more banks. A holding company is a company whose only purpose is to own a controlling interest in other companies. A bank holding company can more easily expand its market through acquisitions than a bank can. The Bank Holding Company Act of 1956 requires that bank holding companies register with the Board of Governors of the Federal Reserve System. A 1966 amendment to the Act set standards for acquisitions and a 1970 amendment restricted bank holding companies to banking. Another benefit enjoyed by bank holding companies is the removal of the geographic restriction imposed by most state laws on banks that required all branches of a bank to be within a certain geographic location. The advantages of bank holding companies are evidenced by the fact that, in 2000, 76% of banks were owned by bank holding companies. Compiled By Nut khorn Page 13 The Financial Services Modernization Act of 1999 deregulated the financial industry even more by creating the legal entity known as the financial holding company that can control banks, securities firms, and insurance companies. Previous to this Act, banks were restricted to banking by the Glass-Steagall Act of 1933 and the Bank Holding Company Act. The primary purpose of restricting banks to banking is to limit their risk because the federal government insures their customers' deposits and because solvent banks are essential to any modern economy as best evidenced by the 2007-2009 credit crises. Consequently, for a bank holding company to qualify as a financial holding company, its subsidiaries must be well managed and well capitalized. All of its depository institutions must have satisfactory Community Reinvestment Act (CRA) ratings, which requires banks to lend back to the community of its depositors. The bank holding company must register with the Federal Reserve, declaring and certifying that it is qualified as a financial holding company under the Act. The largest financial holding company is J.P. Morgan Chase & Co., with assets totaling $2.1 trillion in 2009. According to the Federal Reserve, at the end of 2007, the top 10 banks held 53% of all assets held by banks, while the top 100 banks held 80%. Conclusion The deregulation of financial institutions caused many to take outsized risks in the hope of earning huge profits. Many took these risks because they considered themselves too big to fail and because they could pass their credit default risks to investors of their securitized loans. Of course, it was deregulation that allowed these companies to become so large, so the government could not allow them to fail since it could cause many other financial institutions to fail through a domino effect caused by credit default swaps. Consequently, many governments Compiled By Nut khorn Page 14 were forced to pump trillions of dollars into their banks and their economy to prevent a death spiral of deflation caused by limited credit. There will probably be more restrictions on banks in the future to limit their risk both to themselves and to the economy. One thing that seems certain is that the different regulatory agencies will be consolidated to prevent banks from shopping around for the most lenient regulator. (15) A financial market is a market in which financial assets (securities) can be purchased or sold Financial markets facilitate financing and investing by households, firms, and government agencies Participants that provide funds are called surplus units (suppliers of funds) e.g., households, investors… Participants that enter markets to obtain funds are deficit units (demanders of funds) e.g., government, companies… A major participant in financial markets is the Fed, because it controls the money supply Compiled By Nut khorn Page 15