Investments in available-for

advertisement

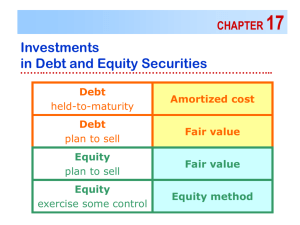

Chapter 15 Investments Intermediate Accounting 11th edition Nikolai Bazley Jones An electronic presentation By Norman Sunderman and Kenneth Buchanan Angelo State University COPYRIGHT © 2010 South-Western/Cengage Learning 2 Objectives 1. Explain the classification and valuation of investments. 2. Account for investments in debt and equity trading securities. 3. Account for investments in available-for-sale debt and equity securities. 4. Account for investments in held-to-maturity debt securities, including amortization of bond premiums and discounts. 3 Objectives 5. Understand transfers and impairments. 6. Understand disclosures of investments. 7. Explain the conceptual issues regarding investments in marketable securities. 8. Account for investments using the equity method. 9. Describe additional issues for investments. 10. Account for derivatives of financial instruments (Appendix). 4 Why Companies Invest in Other Companies 1. Additional revenues from idle cash 2. Control over another company 3. Beneficial relationship with another company 5 Classification of Investments 1. Trading securities 2. Available-for-sale securities 3. Held-to-maturity debt securities 6 Trading Securities Trading securities are investments in debt and equity securities that are purchased and held principally for the purpose of selling them in the near term. 7 Trading Securities These securities are reported at their fair market value on the ending balance sheet, and unrealized holding gains and losses are included in net income of the current period. 8 Available-for-Sale Securities Investments in available-forsale securities are (a) debt securities that are not classified as being held to maturity, and… 9 Available-for-Sale Securities …(b) debt and equity securities that are not classified as trading securities. 10 Available-for-Sale Securities Investments in available-for-sale securities are reported at their fair value on the ending balance sheet date, and the unrealized holding gains or losses are reported as a component of other comprehensive income. 11 Available-for-Sale Securities Therefore, the unrealized holding gains and losses for available-for-sale securities are not included in net income. 12 Held-to-Maturity Debt Securities Investments in held-to-maturity debt securities are debt securities for which the company has the “positive intent and ability to hold those securities to maturity.” 13 Held-to-Maturity Debt Securities Investments in held-to-maturity debt securities are reported at their amortized cost on the balance sheet…not their fair value. 14 Accounting for Investments Investment Categories Investment in Equity Securities 1. No significant influence (less than 20% ownership) a. Trading b. Available for sale 2. Significant influence (20 to 50% ownership) 3. Control (more than 50% ownership) Accounting Method Fair value Fair value Reporting of Unrealized Holding Gains and Losses Equity method Net income Other comprehensive income Not recognized Consolidation Not recognized 15 Accounting for Investments Investment Categories Accounting Method Investment in Debt Securities 1. Trading 2. Available for sale Fair value Fair value 3. Held to maturity Amortized cost Reporting of Unrealized Holding Gains and Losses Net income Other comprehensive income Not recognized 16 Investments in Debt and Equity Trading Securities 1. The investment is initially recorded at cost. 2. It is subsequently reported at fair value on the ending balance sheet(s). 3. Unrealized holding gains and losses are included in net income of the current period. 4. Interest and dividend revenue, as well as realized gains and losses on sales, are included in net income of the current period. 17 Investments in Available-for-Sale Debt and Equity Securities 1. The investment is initially recorded at cost. 2. It is subsequently reported at fair value on the ending balance sheet(s). 3. Unrealized holding gains and losses are reported as a component of other comprehensive income. 4. The cumulative unrealized holding gains and losses are reported in the accumulated other comprehensive income section of stockholders’ equity 5. Interest and dividend revenue, as well as realized gains and losses on sales, are included in net income for the current period. 18 Investments in Available-for-Sale Debt and Equity Securities Kent Company purchases the following securities on May 1, 2009 as an investment in available-forsale securities: • 100 shares of A Company common stock at $50 per share • 300 shares of B Company common stock at $80 per share • 200 shares of C Company preferred stock at $120 per share • $15,000 D Company 10% bonds $ 5,000 24,000 24,000 15,000 Total $68,000 19 Investments in Available-for-Sale Debt and Equity Securities Investment in Available-for-Sale Securities Interest Revenue Cash 68,000 625 68,625 Accrued interest on the D Company bonds from November 30, 2008 to May 31, 2009: May 31, 2009 Cash Interest Revenue 750 750 $15,000 × 0.10 × 6/12 20 Investments in Available-for-Sale Debt and Equity Securities December 31, 2009 Interest Receivable Interest Revenue 125 125 During 2009 Kent Company receives dividends of× 1/12 $15,000 × 0.10 $3,000 from its investment in the stock of A, B, and C Companies. Cash Dividend Revenue 3,000 3,000 21 Investments in Available-for-Sale Debt and Equity Securities The cost and fair value of the available-for-sale securities held by the Kent Company is as follows: Security 100 shares of A Company common stock 300 shares of B Company common stock 200 shares of C Company preferred stock $15,000 face value of D Company 10% bonds Totals Cost $ 5,000 24,000 24,000 15,000 $68,000 Cumulative 12/31/09 Change Fair in Fair Value Value $ 6,000 23,500 26,000 15,500 $71,000 $ 1,000 (500) 2,000 500 $3,000 22 Investments in Available-for-Sale Debt and Equity Securities The cost and fair value of the available-for-sale securities held by the Kent Company is as follows: Allowance for Change in Value of Investment Unrealized Increase/Decrease in Value of Cost Security Available-for-Sale Securities 100 shares of A Company common stock $ 5,000 300 shares of B Company common stock 24,000 200 shares of C Company preferred stock 24,000 $15,000 face value of D Company 10% bonds 15,000 Totals $68,000 Cumulative 12/31/09 Change Fair in Fair 3,000 Value Value 3,000 $ 6,000 $ 1,000 23,500 (500) 26,000 2,000 15,500 500 $71,000 $3,000 23 Investments in Available-for-Sale Debt and Equity Securities The same securities are held on December 31, 2010. Security 100 shares of A Company common stock 300 shares of B Company common stock 200 shares of C Company preferred stock $15,000 face value of D Company 10% bonds Totals Cost $ 5,000 24,000 24,000 15,000 $68,000 Cumulative 12/31/10 Change Fair in Fair Value Value $ 6,100 22,700 23,200 14,000 $66,000 $ 1,100 (1,300) (800) (1,000) $(2,000) 24 Allowance for Change in Value of Investment 12/31/09 3,000 5,000 adjusting entry 2,000 12/31/10 Unrealized Increase/Decrease in Value of Available-for-Sale Securities Allowance for Change in Value of Investment 5,000 5,000 25 Sale of Available-for-Sale Securities On March 1, 2011 the Kent Company sold the 100 shares of A Company stock for $6,000. The stock had a fair value on December 31, 2010 of $6,100. Cash Investment in Available-for-Sale Securities Gain on Sale of Available-for-Sale Securities Unrealized Increase/Decrease in Value of Available-for-Sale Securities Allowance for Change in Value of Investment 6,000 5,000 1,000 1,100 1,100 26 Sale of Available-for-Sale Securities Security 300 shares of B Company common stock 200 shares of C Company preferred stock $15,000 face value of D Company 10% bonds Totals Cost $24,000 24,000 15,000 $63,000 Cumulative 12/31/11 Change Fair in Fair Value Value $23,500 24,200 14,700 $62,300 $(500) 100 (300) $(700) 27 Allowance for Change in Value of Investment 2,400 adjusting entry 2,000 1,100 12/31/10 3/1/11 700 12/31/11 Allowance for Change in Value of Investment Unrealized Increase/Decrease in Value of Available-for-Sale Securities 2,400 2,400 28 Investments in Held-to-Maturity Debt Securities 1. The investment is initially recorded at cost. 2. It is subsequently reported at amortized cost on the ending balance sheet(s). 3. Unrealized holding gains and losses are not recorded. 4. Interest revenue and realized gains and losses on sales (if any) are all included in net income. 29 Investments in Held-to-Maturity Debt Securities A company purchases 9% bonds with a face value of $100,000 on August 1, 2009, at 99 plus accrued $100,000 × 0.99 interest, which is payable semiannually. Investment in Held-to-Maturity Debt Securities Interest Revenue Cash 99,000 1,500 100,500 $100,000 × 0.09 × 2/12 30 Accounting for Bond Premiums On January 1, 2009, the Colburn Company invests in bonds that will be held to maturity, with a face value of $100,000 and paying $102,458.71. The stated interest rate is 13% and the effective interest rate is 12%. Investment in Held-to-Maturity Debt Securities 102,458.71 Cash 102,458.71 31 Accounting for Bond Premiums 32 Accounting for Bond Premiums The Colburn Company records the first interest receipt on June 30, 2009, using the effective interest method. Cash Investment in Held-to-Maturity Debt Securities Interest Revenue 6,500.00 352.48 $100,000 × 0.13 × 1/26,147.52 $102,458.71 × 0.12 × 1/2 33 Accounting for Bond Discounts On January 1, 2009, the Colburn Company invests in bonds that will be held to maturity, with a face value of $100,000 and paying $97,616.71. The stated interest rate is 13% and the effective interest rate is 14%. Investment in Held-to-Maturity Debt Securities 97,616.71 Cash 97,616.71 34 Accounting for Bond Discounts 35 Accounting for Bond Discounts The Colburn Company records the first interest receipt on June 30, 2009, using the effective interest method. Cash Investment in Held-to-Maturity Debt Securities Interest Revenue 6,500.00 333.17 6,833.17 $97,616.71 × 0.14 × 1/2 Amortization of Bonds Acquired Between Interest Dates The Tallen Company purchased 13% bonds with a face value of $200,000 for $204,575.07 on April 3, 2009. Interest on these bonds is payable June 30 and December 31, and the bonds mature on December 31, 2011. Investment in Held-to-Maturity Debt Securities 204,575.07 Interest Revenue 6,500.00 Cash 211,075.07 $200,000 × 0.13 × 3/12 Continued Amortization of Bonds Acquired Between Interest Dates June 30, 2009 Cash Interest Revenue Investment in Held-to-Maturity Debt Securities December 31, 2009 Cash Interest Revenue Investment in Held-to-Maturity Debt Securities ($204,575.07 × 0.12 × 1/4) + $6,500 13,000.00 12,637.25 362.75 ($204,575.07 – $362.75) × 0.12 × 1/2 13,000.00 $13,000 – $12,637.25 12,652.74 747.26 $13,000 – $12,652.74 38 Sale of Investment in Bonds Before Maturity The $100,000 of 13% bonds purchased by the Colburn Company for $97,616.71 were sold on March 31, 2010 for $102,000 plus accrued interest. Investment in Held-to-Maturity Debt Securities Interest Revenue Cash Interest Revenue Investment in Held-to-Maturity Debt Securities Gain on Sale of Debt Securities 198.61 $100,000 ×198.61 0.13 × 1/4 105,250.00 ($2,383.29 ÷ 6) × 1/2 3,250.00 $102,000 + $3,250 98,609.76 3,390.24 $98,411.15 + $198.61 39 Accounting for Investments Classify According to Management Intent as: Recognize Interest and Dividend Revenue in: Recognize Realized Gain or Loss in: Compute Realized Gain or Loss as: Trading Net Income Net Income Selling Price minus Fair Value at Most Recent Balance Sheet Date Available-for-Sale Net Income Net Income Selling price minus (Amortized) Cost Held-to-Maturity Net Income Net Income Selling Price minus (Amortized) Cost 40 Transfers of Investments Between Categories 1. 2. 3. 4. A transfer from the trading category A transfer into the trading category A transfer into the available-for-sale category A transfer of a debt security into the held-tomaturity category from the available-for-sale category 41 Transfer into Trading Category from Available-for-Sale Category In 2010, the Kent Company transfers the Company A securities into the trading category when their fair value is $6,300. Investment in Trading Securities Investment in Available-for-Sale Securities Gain on Transfer of Securities Unrealized Increase/Decrease in Value of Available-for-Sale Securities Allowance for Change in Value of Investment 6,300 5,000 1,300 1,100 1,100 42 Transfer into Available-for-Sale Category from Held-to-Maturity Category The Devon Company has $10,000 in bonds that were purchased at par. When the fair value is $9,500, Devon transfers them into the availablefor-sale category. Investment in Available-for-Sale Securities 10,000 Investment in Held-to-Maturity Debt Securities Unrealized Increase/Decrease in Value of Available-for-Sale Securities Allowance for Change in Value of Investment 10,000 500 500 43 Transfer into Held-to-Maturity Category from Available-for-Sale Category The Devon Company classifies its bond investment as available for sale with a previous fair value of $9,700, and transfers them into the held-tomaturity category when the current market value of the debt securities is $9,500. Investment in Held-to-Maturity Debt Securities Unrealized Increase/Decrease from Transfer of Securities Investment in Available-for-Sale Securities Continued 9,500 500 10,000 44 Transfer into Held-to-Maturity Category from Available-for-Sale Category An entry is needed to eliminate the previous $300 ($9,700 – $10,000) amounts in the Allowance and Unrealized Increase/Decrease accounts. Allowance for Change in Value of Investment Unrealized Increase/Decrease in Value of Available-for-Sale Securities 300 300 45 Impairments Impairments may be an “other than temporary” decline below the amortized cost of an investment in a debt security classified as available for sale or held to maturity. 46 Impairments 1. Determine Whether the Investment is Impaired. An investment is impaired when its fair value (selling price) is less than its cost. 2. Evaluate Whether the Impairment is Other Than Temporary. The company must evaluate whether it will be able to recover the cost of the investment. 3. If the Impairment is Other Than Temporary, the Company Recognizes a Loss Equal to the Difference Between the Cost of the Investment and Its Fair Value. 47 Impairments The Tracy Company has a bond investment categorized as held to maturity, which has an unamortized carrying value of $21,500 and a fair value of $6,500. The investment is considered to be “impaired.” Realized Loss on Decline in Value 15,000 Investment in Held-to-Maturity Debt Securities 15,000 48 Disclosures 1. Trading Securities. A company must disclose the change in the net unrealized holding gain or loss that is included in each income statement. 2. Available-for-Sale Securities. For each balance sheet date, a company must disclose the aggregate fair value, gross unrealized holding gains and gross unrealized holding losses, and (amortized) cost by major security types. 3. Held-to-Maturity Debt Securities. For each balance sheet date, a company must disclose the aggregate fair value, gross unrealized holding gains, gross unrealized holding losses, and amortized cost by major security types. 49 Financial Statement Classification Current Assets Temporary investment in available-for-sale securities (at cost) $29,000 Plus: Allowance for change in value of investment 500 Temporary investment in available-for-sale securities (at fair value) $29,500 Noncurrent Assets Investment in available-for-sale securities (at cost) Plus: Allowance for change in value of investment Investment in available-for-sale securities (at fair value) $39,000 2,500 $41,500 50 A Conceptual Evaluation 1. Fair value is required in the balance sheet for trading securities and available-for-sale securities, but amortized cost is required for held-to-maturity securities. 2. Fair value is not required for certain liabilities. 3. Unrealized holding gains and losses are reported in net income for trading securities but in other comprehensive income for available-for-sale securities. 4. The classification of securities is based on management intent. 51 IFRS vs. U.S. GAAP IFRS also use the trading, available-for-sale, and held-to-maturity categories. The valuation methods are the same for each category as under U.S. GAAP. IFRS also apply these categories to all financial instruments, such as loans and receivables. IFRS allow for the reversal of impairment losses related to held-to-maturity securities and available-for-sale securities. 52 Equity Method When an investor corporation owns a significantly large percentage of common stock, it is able to exert significant influence over the operating and financial policies of the investee corporation. The equity method is used to account for this investment. 53 Equity Method Acknowledges the existence of a material economic relationship between the investor and the investee Is based upon the requirements of accrual accounting Supplies more relevant information for decision makers who rely on financial statements 54 Equity Method In the absence of evidence to the contrary, an investment of 20% or more in the outstanding common stock of the investee leads to the presumption of significant influence. 55 Equity Method According to GAAP, what are the facts and circumstances that indicate that investors with 20% or more in the investee’s stock should not use the equity method? 56 Equity Method Not Used Opposition by the investee which challenges the investor’s ability to exercise significant influence through litigation or complaints to governmental regulatory authorities. The investor and investee sign an agreement that the investor surrenders significant rights as a shareholder. Majority ownership of the investee is concentrated among a small group of shareholders who operate the investee without regard to views of the investor Inability to gather financial information not available to other shareholders Failure to obtain representation on the investee’s board of directors 57 Equity Method Cliborn Company purchases 4,200 shares of the S Company’s outstanding stock (25%) on January 1, 2010 for $125,000 (significant influence). Investment in Stock: S Company Cash 125,000 125,000 S Company pays a $20,000 dividend on August 27, 2010. Cash Investment in Stock: S Company 5,000 5,000 58 Equity Method S Company reported net income for 2010 of $81,000, consisting of ordinary income of $73,000 25% of $73,000 and an extraordinary gain of $8,000. Investment in Stock: S Company 20,250 Investment Income: Ordinary Investment Income: Extraordinary 18,250 2,000 25% of $84,000 25% of $8,000 59 Equity Method Balance Sheet Book Value Fair Value Depreciable assets (remaining life, 10 years) Other nondepreciable assets (e.g., land) Total $400,000 190,000 $590,000 $450,000 246,000 $696,000 Liabilities Common Stock Retained earnings Total $200,000 $220,000 250,000 = $590,000 – $200,000 140,000 $590,000 Investment book value difference × % of investment 50,000 × 25% = 12,500 60 Equity Method When acquired by S Company, the investee’s depreciable assets had a fair value that exceeded book value by $50,000 (10-year life). Cliborn’s share of the depreciable asset value is $12,500 (25%). Additional depreciation is needed on December 31. Investment Income: Ordinary Investment in Stock: S Company 1,250 1,250 Note that this entry results in a deduction from $12,500 ÷ 10 ordinary investment income. 61 Financial Statement Disclosures—Carrying Value Acquisition price January 1, 2010 Add: Share of 2010 reported ordinary income Share of 2010 reported extraordinary income Less: Dividends received August 27, 2010 Depreciation on excess fair value of acquired assets Carrying value $125,000 18,250 2,000 $145,250 (5,000) (1,250) $139,000 62 Financial Statement Disclosures—Equity Income Share of 2010 ordinary income Less: Depreciation on excess fair value of acquired assets Ordinary investment income Plus: Share of investee extraordinary income Net investment income $ 18,250 (1,250) $ 17,000 (2,000) $ 19,000 63 Change to Equity Method When an investor currently using the fair value method acquires enough additional common shares during a year to exercise significant influence over the investee, the investor is required to adopt the equity method of accounting. When the equity method is adopted, the investor restates its investment in the investee by debiting the Investment account and crediting Retained Earnings for its previous percentage of investee income (less dividends) for the period from the original date of acquisition to the date that significant influence was obtained. This is a retrospective restatement (adjustment). 64 Change to Equity Method The company also eliminates any amounts included in the allowance and unrealized increase/decrease amounts that it used to record these shares at fair value. Thereafter, the equity method is applied in the usual manner based on the current percentage of ownership. 65 Change to Equity Method Example Assume that on January 2, 2009, Short Company purchased as its only investment 15% of the outstanding common stock of J Corporation for $150,000 (when the book value of net assets was $1,000,000). At the end of 2009, the J Corporation reported net income of $300,000 and paid dividends of $60,000; at this time, the market value of the shares was $186,000 so the company wrote up the carrying value of the investment (using an allowance account) to fair value. On January 2, 2020, to exert significant influence on J Corporation, Short purchased an additional 25% of the outstanding common stock of the J Corporation for $310,000. 66 Change to Equity Method x 15% = x 15% = x 15% = 67 IFRS vs. U.S. GAAP The application of the equity method is generally the same under IFRS and U. S. GAAP. One major terminology difference is that IFRS use the term “associate” to refer to what would be called an “equity method investee” under U.S. GAAP. In addition, IFRS do not address whether an investor’s interest which is represented by something other than an equity instrument but that is similar in substance to equity instruments (e.g., in-substance common stock) gives rise to significant influence over the investee. U.S. GAAP contains more detailed guidance on such nonequity interests. U.S. GAAP also requires more detailed disclosures than required under IFRS. 68 Stock Dividends Smith Corporation purchased 2,000 shares of Kell Company common stock for $30 per share. Two months later Kell issued a 50% stock dividend. Memo: Received 1,000 shares of Kell Company common stock as a stock dividend. The cost of the shares is now $20 per share, computed as follows: $60,000 ÷ 3,000 (2,000 + 1,000) shares. 69 Stock Dividends Subsequently, Smith Corporation sold 500 of the shares for $25 per share, and the fair value at the most recent balance sheet date was $23 per share. Cash (500 × $25) Investment in Available-for-Sale Securities (500 × $20) Gain on Sale of Investment Unrealized Increase/Decrease in Value of Available-for Sale Securities [500 × ($23 – $20)] Allowance for Change in Value of Investment 12,500 10,000 2,500 1,500 1,500 70 Cash Surrender Value of Life Insurance Mele Corporation pays an annual insurance premium of $5,500 at the beginning of the year to cover the lives of its officers. Prepaid Insurance Cash 5,500 5,500 Continued 71 Cash Surrender Value of Life Insurance According to the terms of the insurance contract, the cash surrender value of the policies increases from $7,200 to $8,300 during the year. Insurance Expense 4,400 Cash Surrender Value of Life Insurance 1,100 Prepaid Insurance $8,300 – $7,200 5,500 72 Appendix: Derivatives Derivatives are financial instruments are relatively new and are becoming increasingly common and it is important for financial statements to show the effects of that risk management. Companies use derivates to reduce the risk of adverse changes in interest rates, commodity prices, and foreign exchange rates. 73 Appendix: Derivatives A derivative financial instrument (or simply derivative) derives its value from an underlying asset or index. Thus, derivatives include futures, forward, swap, and option contract. Derivative contracts can be very complex, and they involve the following concepts: A derivative’s cash flow or fair value must fluctuate and vary based on the changes in one or more underlying variables. The contract must be based on one or more notional amounts or payment provisions or both, even though title to that amount never changes. The underlying and notional amounts determine the amount of the settlement. 74 Appendix: Derivatives A derivative financial instrument (or simply derivative) derives its value from an underlying asset or index. Thus, derivatives include futures, forward, swap, and option contract. Derivative contracts can be very complex, and they involve the following concepts: Many contracts require no initial net investment. The contract can be readily settled by a net cash payment. 75 Appendix: Derivatives A hedge is a means of protecting against a financial loss. For a derivative to be considered a hedge, it must be “highly effective” in offsetting risk exposures because of changes in fair values or cash flows of the hedge. The three types of hedges are: Fair value hedges Cash flow hedges Hedges of foreign currency exposures or net investments in foreign operations 76 Appendix: Derivatives An interest-rate swap is an agreement in which two companies agree to exchange the interest payments on debt over a specified period. The interest payments are based on a principal amount that often is referred to as a notional (i.e., imaginary) amount because the swap does not involve an actual exchange of principal at either inception or maturity. 77 Appendix: Hedges A fair value hedge protects against the risk from changes in value caused by fixed terms, rates, or prices. – For example, a company with debt that has a fixed interest rate that enters into an interest rate swap to pay a variable rate of interest and receive a fixed rate of interest. – This protects the company against paying more interest than necessary if interest rates decline. – Gains or losses on the market value of these hedges flow through net income. 78 Appendix: Fair Value Hedge Suppose that Laki Company has had a $1 million, 6% bank loan (the financial instrument) from MidAmerica Bank outstanding for several years. On January 1, 2010, when the loan has five years remaining, Laki contracts with Jordan Investment Bank (a swaps dealer) for a fiveyear interest-rate swap (the derivative) with a $1 million notional amount. Laki agrees to receive from Jordan a fixed interest rate of 6% and to pay Jordan an interest rate each year that is variable. The variable rate is the LIBOR (London Interank Offer Rate) interest rate at the beginning of each year. 79 Appendix: Fair Value Hedge 80 Appendix: Fair Value Hedge December 31, 2010 Interest paid on original loan to Mid-America Interest Expense Cash 60,000 60,000 Interest-rate swap payment received from Jordan Cash Interest Expense 7,000 7,000 81 Appendix: Fair Value Hedge The fair value method uses market values to recognize the value of derivatives if they are available, such as for future contracts traded on exchanges. The fixed market rate of interest at the end of the year for the remaining life of the loan or derivative (7% for a four-year loan or derivative at December 31, 2010, and we assume it changes to 5.5% for a three-year loan or derivative at December 31, 2011) The difference in the fixed interest rates at the end of 2010 is 1% (6% fixed rate – 7% four-year market rate. Present value of derivative = $10,000 × 3.387211 (n = 4, i = 0.07) = $33,872 82 Appendix: Fair Value Hedge December 31, 2010 Loss due to market rate greater than fixed rate Loss in Value of Derivative Liability from Interest Rate Swap 33,872 33,872 Gain results from the decrease in the present value of the debt due to increase in the market rate Notes Payable Gain in Value of Debt 33,872 33,872 83 Appendix: Fair Value Hedge December 31, 2011 Interest paid on original loan to Mid-America Interest Expense Cash 60,000 60,000 Interest-rate swap payment to Jordan Interest Expense Cash 8,000 8,000 84 Appendix: Fair Value Hedge Laki again determines the gain or loss for 2011 on the derivative by computing the net present value of the future cash flows over the remaining life of the derivative. The fixed market rate of interest at the end of the year for the remaining life of the loan or derivative changes to 5.5% for a three-year loan or derivative at December 31, 2011. The difference in the fixed interest rates at the end of 2011 is 0.5% (6% fixed rate – 5.5% three-year market rate). Present value of derivative = $5,000 × 2.697933 (n = 3, i = 0.55) = $13,940 85 Appendix: Fair Value Hedge December 31, 2011 A swap derivative asset and gain exist because the current 5.5% market rate is less than the 6% fixed rate Laki receives on the derivative. So Laki has moved from a $33,782 liability at the end of 2010 to a $13,490 asset position at the end of 2011, and has a $47,362 ($33,872 + $13,490) gain. Gain due to market rate less than fixed rate Liability from Interest Rate Swap Asset from Interest Rate Swap Gain in Value of Derivative 33,872 13,490 47,362 86 Appendix: Fair Value Hedge December 31, 2011 Loss results from the increase in the present value of the debt due to decrease in the market rate Loss in Value of Debt Note Payable 47,362 47,362 87 Appendix: Hedges A cash flow hedge protects against the risk caused by variable prices, costs, rates, or terms that cause future cash flows to be uncertain. – For example, a company with variable rate debt that enters into an interest rate swap to pay a fixed rate of interest and receive a variable rate. – This protects the company against paying more interest than necessary if interest rates increase. – Gains or losses of cash flow hedges flow through other comprehensive income. 88 Appendix: Cash Flow Hedge Assume that Laki Company has had a $1 million, 5.3% variable rate bank loan that is based on the LIBOR rate (the financial instrument) from MidAmerica Bank outstanding for several years. On January 1, 2010, when the loan has five years remaining, Laki contracts with Jordan Investment Bank (a swaps dealer) for a five-year interest-rate swap (the derivative) with a $1 million notional amount. Laki agrees to receive from Jordan a variable interest rate of 5.3% (for 2010) and to pay Jordan a fixed interest rate each year of 6%. 89 Appendix: Fair Value Hedge 90 Chapter 15 Task Force Image Gallery clip art included in this electronic presentation is used with the permission of NVTech Inc.