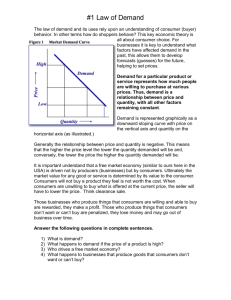

Economics Key Terms

advertisement

1. 2. 3. 4. 5. 6. 7. 8. Economics need want law of scarcity producer consumer factors of production supply 9. demand 10. law of supply 11. law of demand 12. price 13. equilibrium point 14. surplus 15. shortage 16. Economic interdependence 17. Opportunity Cost 18. Recession 19. Depression 20. Gross National Product(GNP) 1. 2. 3. 4. 5. 6. 7. Economics need want law of scarcity producer Consumer Opportunity Cost 8. Command Economy- An economy where interactions between producers and consumers are controlled by gov’t 9. Market- An economy where producers make what consumers want without government interference 10. Traditional-an economy with limited interactions because of agricultural selfsufficiency, which often includes bartering. What is “The Economy” The Economy is all the interactions between Producers and Consumers Producer: Those who make or manufacture goods or services to sell. Consumer A person who buys or rents goods or services. 1. law of scarcity-All things are limited 2. Opportunity Cost-In order to get something, you must give something else up Government Interference in free market How: Why: Taxes Tariff(import) Laws Price Ceiling Price floor Patents Protection of People’s •Health •Environment •jobs •inventions •American Products *Raise money More Less Capitalism (Free Market) Mixed Communism (Command Economy) Reading 5: Three Main Types of Economies pg. 471 What are the 3 economic systems according to the reading? What 2 economies are the most common? What is the difference between a command and a market? What type of economy do you think the U.S. has? Explain. Bellwork Open notebooks and date 12/13 Copy down the following questions in your notes, skipping a line between each. 1. What are the two main types of economies? Command(Communism) and Free Market(Capitalism) 2. What is the difference between them? Economic decisions are made by the government vs. the free interaction between producers and consumers. Reading 4 p. 469 What do we have to work with? What is Land? What is Labor? What is Capital? What is Management? BackEast Printing and Design Factors of Producton Land Labor Capital Management Bellwork: Hardest DQ of the year 1. Edgar rents a kiosk(one of those annoying little stands in the middle of the mall) in the King of Prussia mall at a cost of 2500.00/month to sell miniature remote control helicopters. He has a part time staff of 2 high school kids that each work 20 hrs/week at 8 dollars/hour. If he can sell each helicopter for 50 dollars, how many will he have to sell to break even for the month of December? 2. If he is able to break even is this business a good decision? Why or why not? Supply The amount of a good or service available at a particular price Law of Supply As prices go up, producers are willing to produce more, as prices go down, they produce less Demand The ability and willingness of people to buy something. Law of Demand As prices go up, people demand less. As prices go down, people demand more. Agenda 1. DQ Talk 2. Key Terms 3. Supply/Demand graphs & Equilibrium Point(price) 4. Creating your own graph Supply and Demand Price Quantity Working with Supply/Demand Use the supply/demand schedule to create a graph and plot both the supply and demand curve. Be sure to label both curves as well as the X and Y axis. In addition label the equilibrium point on the graph. The approximate equilibrium price of Little toy helicopters is ______________. Supply/Demand Schedule For Little Toy Helicopters Price $60 $40 $20 $10 $5 Quantity Supplied 150 120 80 20 10 Quantity Demanded 20 40 80 100 200