The Free Enterprise

advertisement

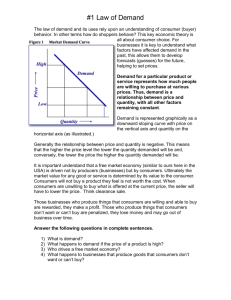

The Free Enterprise Chapter 5.1 2.3 Analyze the Free Enterprise Our Basic Economic Freedoms • Freedom of Ownership – Personal Items, businesses, private property, Intellectual property • Freedom to Compete • Freedom to Take a Risk • Freedom to Make a Profit – Profit is the driving motive in our economy Intellectual Property Rights • Patent: Invention for up to 20 years • Trademark: word, name, symbol or color identifying a business or product – life of business • Copyright: writings, music, artwork for life of author plus 70 years Competition • Struggle between companies for customers • Benefits: – Lower Prices – Better Quality Two Types of Competition PRICE Focuses on the sale price of a product NONPRICE Compete on the basis of factors not related to price - services - location - reputation, etc. Monopoly • There is no competition and one firm controls the market for a given product. • Gives exclusive control over a product or means of production – Microsoft = Technology dominance • NOT LEGAL IN A DEMOCRACY – Exception = utilities Risk = Profit • Risk = The potential for loss or failure. – Money, investments, reputation, – 85% of new product fail in first year! • You must take risk in order to earn profit • Profit is the money earned after all costs and expenses have been paid. – 1-5% of sales • Profit provides the incentive for a person to take risk. How are prices determined in our market place? The interaction of Supply and Demand! 2.6 Evaluate the relationship of cost/profit to supply/demand Law of Demand DEMAND: consumers’ willingness and ability to buy products The lower prices create higher demand; higher prices have a lower demand Exception to the Law: Diminishing Marginal Utility: Consumers will buy just so much of a given product Elasticity of Demand (2 types) • Elastic Demand – Slight change in $ price $ = creates a LARGE change in demand – Products are items of WANT, not in urgent need, substitutes are available • Inelastic Demand – Changes in $price$ = creates very little change in demand – Products are necessities, in urgent need, have no available substitutes Law of Supply SUPPLY: The amount of goods producers are willing to make and sell At higher prices, producers will offer a large quantity of products for sale; at lower prices, producers offer fewer products for sale Supply and Demand Theory Terms to know! • Equilibrium: The point at which Supply and Demand are equal – The goal!! • Surplus: Supply exceeds Demand; Prices will typically lower to reach demand (equilibrium) • Shortage: Demand exceeds Supply; Prices will generally rise until producers can meet the demand (equilibrium)