Chapter 4 Closing Entries Student

advertisement

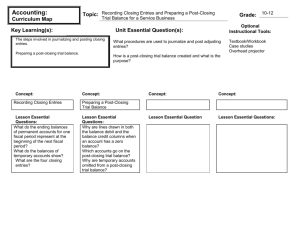

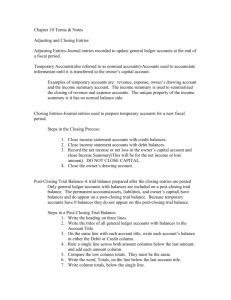

PURPOSE OF CLOSING ENTRIES start over move the company’s net income for a time period to the OE section of the balance sheet Start over measure expenses for a time period Intuitively… if a company has $245 million net income, the equity of the company goes up by $245 million CLOSING ACCOUNTS 1. 2. 3. 4. Updates the owner’s capital account in the ledger by transferring net income (loss) and owner’s drawings to owner’s capital. Prepares the temporary accounts (revenue, expense, drawings) for the next period’s postings by reducing their balances to zero. Accounts are closed every time period (quarterly, annually) Accounting software does this for you!!! ILLUSTRATION 4-2 TEMPORARY VERSUS PERMANENT ACCOUNTS TEMPORARY (NOMINAL) PERMANENT (REAL) These accounts are closed These accounts are not closed ILLUSTRATION 4-3 DIAGRAM OF CLOSING PROCESS (INDIVIDUAL) REVENUES (INDIVIDUAL) EXPENSES Normal Dr. Balance -0- Cr. to close Dr. to close 2 1 OWNER’S CAPITAL Expenses Opening Balance Revenues Normal Cr. Balance -0- ILLUSTRATION 4-3 DIAGRAM OF CLOSING PROCESS OWNER’S CAPITAL Expenses Drawings Opening Balance Revenues Ending Balance 3 OWNER’S DRAWINGS Normal Dr. Balance -0- Cr. to close Example: Journalize the closing entries if Bert’s Pigeon Service had Revenue of $5000, salary expenses of $2000 and supply expenses of $1500; Bert had drawings of $1000 What was the Net income? What was the overall increase in OE? POST-CLOSING TRIAL BALANCE After all closing entries have been journalized and posted, a ___________ ____________ is prepared. The purpose of this trial balance is to prove the equality of the permanent (balance sheet) account balances that are carried forward into the next accounting period. ILLUSTRATION 4-8 POST-CLOSING TRIAL BALANCE Pioneer Advertising Agency Post-Closing Trial Balance October 31, 2002 After Adjustment Debit Credit Cash The post-closing trial$ 15,200 Accounts Receivable 200 balance is prepared Advertising Supplies 1,000 from the permanent Prepaid Insurance 550 Office Equipment 5,000 accounts in the ledger. Accumulated Amortization $ 83 Notes Payable 5,000 The post-closing trial Accounts Payable 2,500 balance provides evidence Unearned Revenue 800 that the journalizing and Salaries Payable 1,200 posting of closing entries Interest Payable 25 has been properly C.R. Byrd, Capital 12,342 $ 21,950 $ 21,950 completed. STEPS IN THE ACCOUNTING CYCLE 9. Prepare post-closing trial balance 1. Analyse transactions 3. Post to ledger accounts 8. Journalize and post closing entries 7. Prepare financial statements 2. Journalize the transactions 4. Prepare a trial balance 6. Prepare adjusted trial balance 5. Journalize and post adjusting entries