Tapping the Full Spectrum of Investors

advertisement

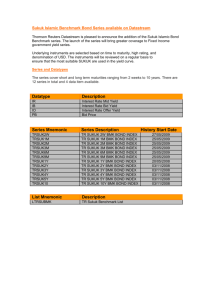

Dr. Turkhan Ali Abdul Manap Senior Economist (IRTI) Prepared for The 2nd Kazan Sukuk Conference, April 9, 2015, Kazan © TAAM 2015 ISLAMIC RESEARCH & TRAINING INSTITUTE (IRTI) (A member of) ISLAMIC DEVELOPMENT BANK GROUP (IDBG) Introduction 2 Capital Market and Economy What makes Islamic finance different? The Five Pillars of Islamic Finance 1) Prohibition of interest 2) Prohibition of speculation 3) Prohibition of the financing of illicit sectors (pork, weapons, alcohol,…) 4) Profit & Loss sharing principle 5) Asset backed principle However: Islamic finance is not restricted to Muslims (the “natural” clients) as some of its principles may attract non-Muslim clients. 4 What is Sukuk ◊ The plural of the Arabic word Sak, literally translated as title deed ◊ Financial certificates structured to comply with Shariah prohibition on the charging or paying interest(Riba) that grants an undivided interest or share in an underlying asset along with the profit, cash flow and risk commensurate with such ownership. ◊ Technically, Sukuk refers to securities, notes, papers or certificates, with features of liquidity and tradability (except for salam and murabahah sukuk) Accounting And Auditing Organization For Islamic Financial Institutions (AAOIFI) ◊ AAOIFI Definition “Investment sukuk are certificates of equal value representing undivided shares in ownership of tangible assets, usufructs and services (in the ownership of) the assets of particular projects or special investment activity” How do Sukuk Differ from Bond ◊ The fundamental of Islamic Finance requires All contract arrangement must be Transparent clear to all parties No any unfair punitive clauses With proper alignment of interest Transaction must not involve excessive risk speculative due to uncertainty Investments should have a social and ethical benefits to the society No involvement of unethical business actives ◊ Which implies that …… How do Sukuk Differ from Bond ◊ Sukuk constitute partial ownership in Receivables (sukuk al Murabaha) A lease (sukuk Al Ijara) A project (Sukuk Al Istisna) A business or partnership (Sukuk Al mudaraba / Musharaka) Investment (sukuk) ◊ So Sukuk represents ownership of a real asset not like conventional bonds own debt. Comparing SUKUK to BONDS Sukuk Bonds 1. Holder owns assets 1. Holder owns cash flow only 2. Use a variety of contracts to create financial obligations between issuer and investors; e.g. Sale, lease, equity partnership, joint-venture etc. 2. Simply use a loan contract to create indebtedness 3. Return linked to profit elements in-built in the sale, lease or partnership 3. Return linked to interest charged out of the loan contract 4. Instrument may be equity or debt depending on underlying contract 4. It is a Debt instrument 5. Tradability of the sukuk depends on the nature of the underlying asset 5. No restriction on the tradability 6. Investment in Shari`ah-compliant activities 6. Proceeds are invested in any business without restrictions How do Sukuk Differ from Bond ◊ sukuk transform bilateral risk-reward sharing between borrowers and lenders into market-based refinancing of shari’ah-compliant lending or trustbased investment in existing or future assets. ◊ sukuk do not pay interest, but generate returns through commoditization of capital gains from actual transactions (i.e., asset transfer), such as: leasing : ijara cost-plus sale : murabahah profit-sharing/”sweat capital”/trust: musharakah or mudarabah shari’ah-compliant assets, usufructs or services ◊ investors own the underlying asset(s) via SPV that funds unsecured payments to investors from direct investment in real, religiously-sanctioned economic activity Sukuk Market At A Glance 11 Development of Sukuk Market ◊ Increasing appeal in non-core markets (UK, Turkey, Maghreb HK. UK and others) ◊ Sukuk issuance soared over the last decades in response to growing demand for alternative investments ◊ Outstanding sukuk globally exceeded US$1.8 trillion at end of 2013 ◊ Total issuance in 2014 equivalent to roughly a quarter o f conventional securitization in EM but only two percent of conventional (local and foreign) bond issuance TOTAL GLOBAL SUKUK ISSUANCES (JAN 2001 – DEC 2014, USD MILLIONS) 137499 140000 116400 111300 120000 100000 92403 80000 60000 52978 50041 40000 33837 ◊ Significant slowdown of Sukuk issuance in 2008 because of market conditions. ◊ Apparent recovery in the recent past ◊ Reportedly healthy pipeline ◊ 2014 Global Sukuk Market bounces back from 2013 low with almost $116.4 billion sukuk issued in the first nine months 37904 24264 20000 7050 13698 9645 1172 1371 0 13 Sukuk Insurance by Structure (2014) Bai' Istijrar Istithmar 1% Bai' Inah 1% 4% Salam 1% Bai' Bithamin Ajil 2% Others 5% Wakala 5% Musharaka 7% Murabaha 59% Ijarah 15% ◊ Murabaha and Ijarah structure are still the preferred choice ◊ By structure, Murabahah and Ijarah remain popular choices among issuers in 2014 with 58% and 15% respective shares for each structure in total sukuk issuances 14 Sukuk Insurance by Region Bahrain Qatar 2% Turkey 3% Indonesia 3% 4% United Arab Emirates 5% Others 6% Malaysia has taken the lead but GCC is still contributing significantly. Suadi Arabia 10% Malaysia 67% 15 Sovereign Sukuk Issuance (2004-2014) Malaysia Brunei Indonesia Qatar Bahrain Pakistan UAE Sudan Gambai Hong Komng South Africa UK Luxembourg Yemen Senagal Singapore Germanay Nigeria 351494 60903 21890 19655 12545 7669 6855 2868 194 1000 500 340 272 250 200 193 123 71 1388 113 65 17 226 17 11 26 401 1 1 2 1 2 1 5 1 1 ◊ issuance still concentrated in parts of Asia and countries of the GCC ◊ Sovereign issuances dominated the global Sukuk market ◊ Government and related entities are driving the growth of the market compared with FI and corporates in the past. ◊ This trend should help the construction of a yield curve against which issuers can benchmark themselves. Sukuk Structure 17 Sukuk Basic Structure Main Sukuk Types Main Type of Sukuk Basic Structure of Ijarah Sukuk Basic Structure of Murabaha Sukuk Basic Structure of Commodity Murabaha Sukuk Basic Structure of Musharaka Sukuk Basic Structure of wakala Sukuk The Way Forward….. 25 Why Russia Needs to Develop Islamic Finance and Sukuk ◊ Islamic finance has become increasingly important in the global financial market, registering exponential growth over the past few years. ◊ Compared with a size of only US$700 billion in 2008, the global Islamic financial industry has expanded remarkably to an estimated US$1.8 trillion by the end of 2013, representing an annual average growth rate of 21%. ◊ According to market estimates, there is a huge potential for further growth, with Islamic financial assets expected to reach US$6.5 trillion by 2020 Why Russia Need to Develop Islamic Finance and Sukuk ◊ Sukuk market is the major growth area for Islamic finance ◊ Ten years ago, new sukuk issuance was only a modest US$5 billion. In just ten years' time, annual sukuk issuance has already surpassed US$100 billion, amounting to US$117 billion in 2013 which was more than 20 times higher than the figure in 2003 ◊ The current account surpluses in the Gulf Cooperation Council (GCC) countries are estimated to be more than US$300 billion ◊ while assets under management by sovereign wealth funds in those countries amounted to as much as US$2 trillion ◊ Islamic investors in the Middle East and other Islamic countries generally have a preference for investing in Shariah-compliant assets. Why Russia Need to Develop Islamic Finance and Sukuk ◊ sukuk are becoming a mainstream asset class in the global financial system. ◊ Financial innovation and tax reform in major international financial centers have made sukuk largely comparable to conventional bonds. ◊ Apart from Islamic investors, sukuk are increasingly appealing to conventional investors as a way to diversify their investment portfolios. What Russian Needs to do ◊ build a conducive platform for sukuk issuance ◊ sukuk are no different from conventional bonds in terms of economic substance, enabling issuers to raise funds while giving investors interest-like return. ◊ However, the more complicated structure of sukuk, which involves the setting up of a special purpose vehicle and multiple transfers of underlying assets, had led to additional tax liability for sukuk issuers. ◊ Tax law amendments need to overcome this obstacle by removing the additional profits tax and stamp duty charges incurred in issuing sukuk as compared with conventional bonds. ◊ Therefore , level the playing field between sukuk and conventional bonds with tax framework changes . What Russian Needs to do ◊ To play a lead-off role for by Issuing Sovereign Sukuk To demonstrate to the global financial markets that the legal, regulatory and taxation frameworks in Russian can well accommodate sukuk issuance. To Encourage and attract more investors. ◊ Government sukuk could play a catalytic role, paving the way for local and international fund-raisers, no matter from the public or private sector, to follow suit. ◊ Make Kazan as a gateway of IFC to Russia’s access to global financial markets Matching the needs of fund raisers and investment demand of investors among Russia, the Middle East, and other parts of the world interested in Islamic financial products The way forward …... ◊ There are at least two ways to kick-off sukuk insurance ◊ 1) Gradual approach: A though legal and tax framework adjustment to cattle the Sukuk insurance but takes long time ◊ 2) Fast track Off shore insurance Location of SPV Withholding tax (20%) – Non residents in Luxembourg and Netherlands VAT tax (18%) – Non-resident leasing out asset such as aircraft to Russian do not need pat VAT Property Tax (2.5) – Basically are exempted if the asset is immovable asset. 32 Contact Dr. Turkhan Ali Abdul Manap Senior Economist Research Division Islamic Research & Training Institute P. O. Box 9201, Jeddah 21413 Kingdom of Saudi Arabia Email: turkhanali@isdb.org website: www.irti.org Tel: + 966 12 646 6329 Fax: + 966 12 637 8927 ISLAMIC RESEARCH & TRAINING INSTITUTE (A member of) ISLAMIC DEVELOPMENT BANK GROUP