CAPITAL BUDGETING

advertisement

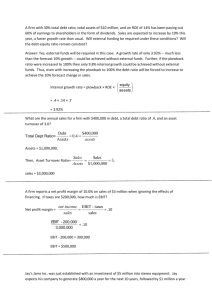

FINANCIAL STATEMENTS Financial Health of Firm Firms produce good and services by using assets Financial condition of firm’s Assets Financing of these assets Shareholder equity = Assets - Liabilities Balance Sheet gives state of Assets & Liabilities Firms sell their goods and services over time Financial performance and profitability Income Statement gives summary of performance over accounting period Statement of Cash Flow tells what has happened to cash Balance Sheet, Current Items Assets and Liabilities Items turning into cash in less than one year current Assets and Liabilities Listed based on liquidity CURRENT ASSETS CURRENT LIABILITIES Cash & Cash Equivalent Taxes Inventory Short term borrowing Accounts Receivables Accounts Payable Prepaid Expenses Accrued Expenses Balance Sheet, Long term Item Long Term Assets Tangible Fixed Assets: Land, Factories, … Intangibles: Goodwill Long Term Liabilities Long term debt Retained Earnings Shareholder equity Current Assets – Current Liabilities = Working Capital Retained earning is an item to ensure Total Assets = Total Liabilities Income Statement Sales Revenue - Cost of Goods Sold Gross Margin or Gross Profit - Operating Expenses Operating Revenue before Depreciation = Earnings Before Interest Tax Depreciation and Amortization = EBITDA - Depreciation Earnings Before Interest and Taxes = EBIT - Interest Expense Earnings before Taxes - Income Tax Expenses Net Income = Profit Statement of Cash Flow Cash is life blood of company Company might be profitable on accrual basis but go bankrupt Capital Investment Stock Borrowings $ Service Debt Investment $ $ Company G&S Inventory Dividend Operating expenses Taxes Statement of Cash Flow Cash Receipts From customers for selling goods & services From borrowing From issuing new capital stocks Cash Disbursements For purchasing inventory that are or will be sold For Interest and principal payment of debt For Income Taxes For Investment in machinery, improvements, .. For dividend payments to stock holders Three statements are interlocked Cash Flow from Operating Activities Net Income Change in Accounts Receivable Change in Inventory Change in Prepaid expenses Change in Accounts payable Change in Accrued expenses Change in Income Tax Operating Cash Flow Before Depreciation Depreciation Cash Flow From Profit-Making Activities Cash Flow from non-Operating Activities Cash Flow From Investing Activities Purchase of Plant, Properties & Equipments Cash Flow From Financing Activities Change in short term debt Long term Borrowings Capital Stock Issue Cash Dividends to Stock Holders Interlocking Nature of Statements Cash Flow From Profit-Making Activities Cash Flow From Investing Activities Cash Flow From Financing Activities Net Change in Cash During Year Profitability Cannot be Measured by Cash Flow Only How to compare Financial Statements of companies of different sizes? Common-Size Income Statement all quantities as a % of Sales Common-Size Balance Sheet all quantities as a % of Total Assets DuPont Model A main metric of performance is ROE = Net Income/Equity To better analyze factors affecting ROE it is decomposed into a series of ratios Each ratio component is meaningful and sheds light on the company and its performance and capital structure This decomposition is called DuPont System ROE = (Net Income/Pretax Profit) * (Pretax Profit/EBIT) *(EBIT/Sales)*(Sales/Assets)*(Assets/Equity) Interpretation of DuPont Model Net Income/Pretax Profit= Tax Burden Ratio Ratio of Net Income after tax to pretax profit and is not affected by capital structure of the company Pretax Profit/EBIT = (EBIT – Interest Expense)/EBIT = Interest Burden Ratio and depends on the capital structure of the company. A closely related ratio is Interest Coverage Ratio or Times Interest Earned = EBIT/Interest Expense EBIT/Sales = Profit Margin = Return on Sale (ROS) = Operating profit per 1$ of sale Interpretation of DuPont Model Sales/Assets = Total Asset Turn Over (ATO) Measures how efficiently management is utilizing assets of the company Assets/Equity = Leverage Ratio = 1+ Debt/Equity (depends on capital structure) ROE = Tax Burden * Interest Burden * Profit Margin * Asset Turn Over * Leverage Operating Cycle Operating Cycle = Inventory Period + Accounts Receivable period = Accounts Payable Period + Cash Cycle Inventory Turnover = Cost of Goods Sold/Average Inventory Inventory Period = 365/ Inventory Turnover Receivable Turnover = Credit Sales/Average Accounts Receivable Receivable Period = 365/ Receivable Turnover Cash Cycle Payables Turnover Cost of Goods Sold/Average Payables Payables Period = 365/ Payables Turnover Cash Cycle = Operating Cycle – Accounts Payable Period Solvency and Liquidity Measures Short Term: Current Ratio = Current Assets/Current Liabilities Quick Ratio = (Current Assets – Inventory)/Current Liabilities Cost of Goods Sold/Average Payables Cash Ratio = Cash/Current Liabilities Long Term: Long-term Debt Ratio = Long-Term Debt/ (Long-Term Debt +Equity ) Solvency and Liquidity Measures Long Term: Long-term Debt Ratio = Long-Term Debt/ (Long-Term Debt +Equity ) Times Interest Earned Ratio = EBIT/Interest Cash Coverage= ( EBIT+ Depreciation)/Interest