Employee Future Benefits

advertisement

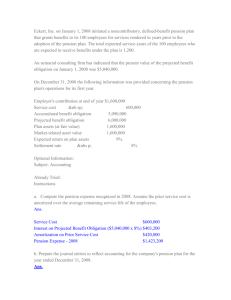

Employee Future Benefits AK/ADMS 4510 M&N – Winter 2004 Nancy Estey, Principal, Accounting Standards Board staff February 23, 2004 4-7 pm; 7-10 pm 1 Employee Future Benefits – February 2004 Discussion Outline Recent headlines Environment driving change Current financial statement impacts Background – – – – – 2 A compensation package Types of employee future benefits Financial statement objectives Deferred compensation Discount rate Employee Future Benefits – February 2004 Discussion Outline 3 Developments in Canada Highlights of Canadian disclosure improvements What’s Ahead Understanding “smoothing” The “Corridor” approach Move to presentation format Employee Future Benefits – February 2004 Recent Headlines 4 Rates, high dollar erase pension gains (G&M, Jan 22/04) Pensions seen as key factor in executive pay (G&M, Jan 7/04) Pension smoothing hides the facts (G&M, Oct 15/03) Pension shortfalls threaten to explode (G&M, May 12/03) Employee Future Benefits – February 2004 Environment Driving Change Significant losses sustained by many pension plans in the last few years + lower market interest rates – – – – Post-Enron era – – – 5 Increased benefit obligation Growing deficit position Drain on cash flow Increased pension costs “Smoothing” results in off-balance sheet debt, which draws attention Poor plan performance increases this debt Need for transparency Employee Future Benefits – February 2004 Current Financial Statement Impacts Average Pension Expense ($ million) $25 $20 $15 $10 $5 $0 2000 2001 2002 Source: Towers Perrin review of financial statements of 90 major Canadian Companies that sponsor defined benefit plans. 6 Employee Future Benefits – February 2004 Current Financial Statement Impacts Average Deferred Pension Cost ($ million) $250 $200 $150 $100 $50 $0 -$50 -$100 -$150 2001 2002 2000 Source: Towers Perrin review of financial statements of 90 major Canadian Companies that sponsor defined benefit plans. 7 Employee Future Benefits – February 2004 A Compensation Package This Year •Salary •Fringe benefits •Bonus Cash Paid When Retired •Pension benefits •Vision Care •Drug Plan •Profit sharing •Life Insurance •Stock options 8 Employee Future Benefits – February 2004 Types of Employee Future Benefits Accounting for future promises – promised pension and other benefits when they retire Eligibility via age and service Pension Benefits – Defined benefit plans now a major cost of doing business Low interest rates Decline in equity markets Post-retirement benefits Life insurance Extended health care – 9 double-digit growth due to Rising drug costs, aging membership Employee Future Benefits – February 2004 F/S Objectives 10 Plan performance affects – Financial Position (B/S) – Operating Results (I/S) – Changes in Financial Position (Cash flows) Employee Future Benefits Accounting – CICA Section 3461 – FAS 87, 88, 106, 112, 132(r) in the US Employee Future Benefits – February 2004 Deferred Compensation Estimate amounts to be paid out in the future (future benefit payments) Discount those future payments to reflect the time value of money Allocate the resulting amount “deferred compensation cost” – 11 Over the periods of service required of the employees in exchange for the promise of those future payments So, cost of future benefits recognized as the employees render service to the company Employee Future Benefits – February 2004 Discount Rate Market-driven rate Controversial – Revalue at each balance sheet date – Volatility in I/S 12 Discount rate Obligation Discount rate Obligation Corridor method (element of smoothing) helps But volatility unwelcome Employee Future Benefits – February 2004 Developments in Canada Long-term – Participate in global project Short-term – – 13 Start over from 1st principles Limited-scope disclosure enhancements Revised disclosure requirements to be issued on or about March 1, 2004 Employee Future Benefits – February 2004 shall recognize ility and an expense for post employment benefits and compensated absences that do not vest or accumulate An entity a liab Highlights of CDN Disclosure Enhancements Disclosures related to the reporting entity’s financial statements – – – – – – 14 when (a) the event obligating the Total cash payments Balance sheet classification of the accrued benefit asset/liability Clarification on the accounting policy disclosures that should be made Components of costs recognized (in addition to the total) Reconciliation of the accrued benefit obligation to the balance sheet asset or liability Effects of a one-percentage-point increase and decrease in the assumed health care cost trend rates Employee Future Benefits – February 2004 shall recognize ility and an expense for post employment benefits and compensated absences that do not vest or accumulate An entity a liab Highlights of CDN Disclosure Enhancements (cont’d) Disclosures related to the benefit plan – – – – – – 15 when (a) the event obligating the Description of the type of plans Actual allocation of plan assets by major asset category Date used to measure the plan assets and the benefit obligations Effective date of the last (as well as the next required) actuarial valuation for funding purposes Significant assumptions Reconciliations - plan obligation and plan assets Employee Future Benefits – February 2004 shall recognize ility and an expense for post employment benefits and compensated absences that do not vest or accumulate An entity a liab Highlights of CDN Disclosure Enhancements (cont’d) Distinction between “public” and non-”public” entity requirements “Public” implies public enterprises, co-operative organizations, deposit-taking institutions or life insurance companies Covers pension benefits, but also postretirement and post-employment plans Interim financial statements – 16 when (a) the event obligating the Total benefit cost Employee Future Benefits – February 2004 What’s Ahead? Developments Around the World UK – FRS 17, mark to market – Aborted; punted to IASB IASB – Plans to issue ED of improvements to IAS 19 in Q2 2004 with final standard Q1 2005 17 the removal of options for the deferred recognition of actuarial gains and losses enhancing disclosure Employee Future Benefits – February 2004 What’s Ahead? Developments Around the World (cont’d) US FASB – – Disclosure ‘quick fix’ Final statement issued with effective date for fiscal years ending after December 15, 2003 18 more complete information about plan assets, obligations, cash flows, and net cost assists users of f/s in assessing the market risk of plan assets, the amount and timing of cash flows, and reported earnings. Employee Future Benefits – February 2004 Understanding “Smoothing” Delayed recognition of events (spread changes over the future) – Amortize to expense over a period of time rather than immediate recognition Treatment of returns on pension plan assets – – 19 Past service costs Actuarial gains/losses [also corridor approach] Expected return, not actual return (difference amortized to expense over time) Market-related value of plan assets deferring recognition of recent investment gains and losses for up to 5 years Employee Future Benefits – February 2004 The “Corridor” approach 20 Employee Future Benefits – February 2004 Move to Presentation format 21 Debate “smoothing” i.e., deferred recognition of events Employee Future Benefits – February 2004