Accrual Method - CSU Department of Business and Financial Services

advertisement

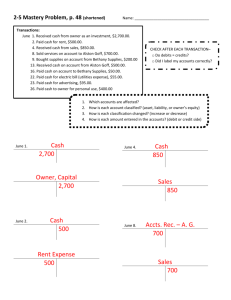

All organizations must choose an accounting method for financial reporting purposes What is an accounting method? The way financial events are recorded Revenue / cash received Expenses / cash paid The way financial position is reported Financial statements There are two basic types of accounting methods: Cash Income is recorded when cash/check is received Expenses are recorded when the vendor is paid Accrual Income is recorded when the sale occurs Expenses are recorded when the goods or services are received (and used) Government entities (including universities) are required to follow GASB standards What is GASB? Government Accounting Standards Board GASB establishes accounting and financial reporting standards for government units GASB Statement No. 34 requires the use of the accrual accounting method Since governments are required to follow GASB standards, CSU is required to use the accrual accounting method Sometimes expenses are purchased in advance and used over future months Service contracts Medical/lab supplies Expenses aren't recorded until the money is actually paid out -- even if the actual expenses were incurred in previous months Revenues are recorded when cash is received Fiscal year end is 6/30/07 (FY07) Cas h Debit $200 (FY 08) Credit Reven u e Debit Credit $200 (FY 08) 1) 4/30/07 Receive order -- test blood sample 2) 5/31/07 Test results completed and invoiced 3) 7/2/07 Customer pays invoice – cash deposit made in following fiscal year (FY08) Fiscal year end is 6/30/07 (FY07) Cas h Debit Credit $50 (FY 08) Ex p en s e Debit Credit $50 (FY 08) 1) 4/30/07 Place order for lab supplies 2) 5/31/07 Receive supplies and use them 3) 7/2/07 Pay the vendor invoice in following the following fiscal year (FY08) The term accrual refers to any individual entry recording revenue or expense in the absence of a cash exchange Accruals are recorded on the transaction date Transaction date is when a financial event occurs whether or not cash is exchanged Services are performed (diagnostic testing) Product is sold (books) Inventory is received Fiscal year end is 6/30/07 (FY07) Cas h Accts Receivable Debit Credit $200 (FY 08) Debit $200 Credit Reven u e Debit $200 (FY 08) Credit $200 1) 4/30/07 Receive order -- test blood sample 2) 5/31/07 Test results completed and invoiced 3) 7/2/07 Customer pays invoice – cash deposit made in following fiscal year (FY08) Fiscal year end is 6/30/07 (FY07) Cas h Accts Payable Debit Credit Debit $50 (FY 08) $50 (FY 08) Credit Ex p en s e Debit $50 Credit $50 1) 4/30/07 Place order for lab supplies 2) 5/31/07 Receive supplies and use them 3) 7/2/07 Pay the vendor invoice in the following fiscal year (FY08) Within this simple difference lies a lot of room for error — or manipulation. Depending on which method is used, financial reporting may be affected at the financial year end Subledger Revenue Expense Subledger $0 $0 Revenue Expense $200 $ 50 General Ledger Cash General Ledger $0 Cash $ 0 Accts Receivable $200 Accts Payable $ 50 Subledger Revenue Expense Subledger $200 $ 50 Revenue Expense $0 $0 General Ledger Cash General Ledger $150 Cash $150 Accts Receivable $ 0 Accts Payable $ 0 Prepaid Expenses Service contracts Paid once per year Should be expensed in 12 equal amounts Example: Service contract $1,800 paid for on 4/1/07 Contract covers 1 year: 4/1/07 – 3/31/08 Fiscal year end is 6/30/07 (FY07) Cas h Debit 1) 4/1/07 Ex p en s e Credit Debit $1,800 $1,800 Credit Pay for 1 year service contract 2) 4/30/07 Use 1 month’s contract expense 3) 5/31/07 Use 1 month’s contract expense 4) 6/30/07 Use 1 month’s contract expense Fiscal year end is 6/30/07 (FY07) Cas h Debit Prepaid Expenses Credit Debit $1,800 $1,800 $150 $150 $150 $150 $150 $150 $1,350 $1,650 $450 $150 1) 4/1/07 Credit Ex p en s e Debit Pay for 1 year service contract 2) 4/30/07 Record 1 month’s contract expense 3) 5/31/07 Record 1 month’s contract expense 4) 6/30/07 Record 1 month’s contract expense Credit Fiscal year end is 6/30/07 (FY07) Cas h Debit Prepaid Expenses Credit Debit $1,800 $1,800 $150 $150 $150 $150 $150 $150 $1,350 $450 1) 4/1/07 Credit Ex p en s e Debit Pay for 1 year service contract 2) 4/30/07 Record 1 month’s contract expense 3) 5/31/07 Record 1 month’s contract expense 4) 6/30/07 Record 1 month’s contract expense Credit FY07: Service Contract Expense $1,800 FY07: Service Contract Expense $ 450 FY08: Service Contract Expense $0 FY08: Service Contract Expense $ 1,350 Service Contracts Service contract expense – FY07 Cash method = $1,800 Accrual method = $450 Service Cash contract expense – FY08 method = $0 Accrual method = $1,350 Deposits CSU Contracts with an outside party who requires a deposit. ½ is often required in advance – may be refundable An expense is not booked until the event takes place Deferred Revenue Sports/youth Revenue camps are paid in advance isn’t earned until the camp takes place Example: 2 week camp costs $500 ($50 per day) Dates of the camp are 6/25/07 – 7/6/07 (M-F) Fiscal year end is 6/30/07 (FY07) Cas h Debit Credit $500 Reven u e Debit Credit $500 $500 1) 5/15/07 Participant signs up for 2 week camp – deposit $500 2) 6/25/07 Camp begins 3) 7/6/07 Camp Ends Fiscal year end is 6/30/07 (FY07) Cas h Debit $500 Credit Deferred Revenue Reven u e Debit Credit Debit Credit $250 $500 $250 $250 $250 1) 5/15/07 Participant signs up for 2 week camp – deposit $500 2) 6/25/07 Camp begins 3) 6/30/07 Record camp revenue earned in FY07 (5 days) FY07: Camp Revenue FY08: Camp Revenue $500 FY07: Camp Revenue $250 $0 FY08: Camp Revenue $250 Deferred Revenue Tuition paid in June for summer semester ending in August Revenue is earned evenly over the entire semester Football This season tickets sold in June hasn’t been earned until the football season begins in September Valerie Monahan 1-3001 Heidi Barclay 1-4148 1-6752 1-7099 Janice Inman Laura Streit http://busfin.colostate.edu/cs.aspx