Title of Chapter

advertisement

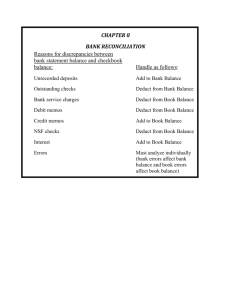

Part II – Bank Reconciliation Chapter 8 © 2009 The McGraw-Hill Companies, Inc. Bank Procedures and Reconciliation Banks help businesses control cash by offering services that: 1.Safeguard Cash – The bank provides a secure place to deposit cash. 2.Improved Efficiency and Effectiveness – The bank strengthens the processing of cash. 3.Independent Verification – The bank statement is used to help the company account for its cash transactions. McGraw-Hill/Irwin Slide 2 Bank Procedures and Reconciliation Cash receipts should be recorded immediately upon receipt and deposited intact daily. Up to date signature card should be maintained. A monthly bank reconciliation should be prepared by an independent party. Controlling Cash in the Bank A deposit ticket should be used for all deposits. Cash disbursements should be made by prenumbered check. McGraw-Hill/Irwin Slide 3 The Bank Statement The bank statement format varies from bank to bank, but the statement usually contains these common elements: 1.an overall summary of the activity in the account, 2.a list of specific transactions posted to the account, including checks cleared, deposits made, and other transactions, and 3.a running balance in the account. Because amounts that are removed from a bank account reduce the bank’s liability, they are reported as debits on the bank statement. Debit Card Slide 4 Need for Reconciliation Your Bank May Not Know About 1.Errors made by the bank 2.Time lags a. Deposits that you made recently b. Checks that you wrote recently You May Not Know About 1.Interest the bank has put into your account 2.Electronic funds transfers 3.Service charges taken out of your account 4.Customer checks you deposited but that bounced (NSF checks) 5.Errors made by you Slide 5 Bank Reconciliation The bank reconciliation reports on the differences between the balance on the bank statement and the balance in the general ledger cash account. The reconciliation results in the up-to-date ending cash balance that will appear on the balance sheet. Updates to Bank Statement Ending cash balance per bank + Deposits in transit Deduct - Outstanding checks Equals = Up-to-date ending cash balance Add Updates to Company's Books Ending cash balance per books Add Add Deduct Deduct Equals McGraw-Hill/Irwin + + = Interest earned Electronic funds transfers NSF checks Bank service charges Up-to-date ending cash balance Slide 6 Bank Reconciliation If an error is found on the bank statement, an adjustment for it is made to the bank balance to determine the up-to-date cash balance. An error made on our books requires an adjusting journal entry to correct. McGraw-Hill/Irwin Slide 7 Bank Reconciliation Jerry Company is preparing the bank reconciliation for the month of June. 1. The June 30th balance on the bank statement is $4,892.56, and the Cash general ledger balance on this date is $4,240.54. 2. There was a deposit in transit in the amount of $475. 3. The bank erroneously deducted a $200 check drawn on the books of Mary, Inc. from our account. 4. At June 30th there were three checks outstanding. Check 1078 dated 6/28, for $372.33; Check 1080 dated 6/29, for $402.41; and Check 1081 dated 6/30, for $66.89. More Information McGraw-Hill/Irwin Slide 8 Bank Reconciliation 5. During the month of June the bank collected an EFT in the amount of $875. 6. A check actually written for $146.88 for supplies was erroneously recorded in our records by the bookkeeper as $173.88. 7. Jerry Company earned interest of $9.25 on its checking account. 8. The bank assessed a service charge of $12.75 for June and we deposited a NSF check in the amount of $413.11. Let’s prepare the bank reconciliation McGraw-Hill/Irwin Slide 9 Bank Reconciliation McGraw-Hill/Irwin Slide 10 Bank Reconciliation McGraw-Hill/Irwin Slide 11 Bank Reconciliation McGraw-Hill/Irwin Slide 12 Bank Reconciliation McGraw-Hill/Irwin Slide 13 Bank Reconciliation McGraw-Hill/Irwin Slide 14 Bank Reconciliation McGraw-Hill/Irwin Slide 15 Bank Reconciliation Every reconciling item that appears on the unadjusted book balance section requires a journal entry to adjust the general ledger cash balance to the up-to-date cash balance. Cash (+A) Accounts Receivable (-A) Supplies Expense (-E, +OE) Interest Revenue (+R, +OE) Bank Service Charge Expense (+E, -OE) Accounts Receivable (+A) Cash (-A) McGraw-Hill/Irwin Debit 911.25 Credit 875.00 27.00 9.25 12.75 413.11 425.86 Slide 16