Cash and Cash Equivalents

advertisement

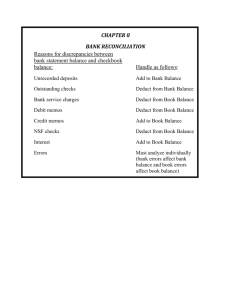

Cash and Cash Equivalents Cash This includes money and other negotiable instrument that is payable in money and acceptable by the bank for deposit and immediate credit. Examples are bills and coins, checks, bank drafts and money orders. To be included or considered as cash, it must be unrestricted as to use, meaning, it must be readily available for use or payment of current obligations, thus, not subject to contractual or legal restrictions. The following items are included in “cash”: Cash on Hand Cash in Bank Cash Fund Cash Equivalents According to PAS 7, cash equivalents are short-term highly liquid investments that are readily convertible into cash so near their maturity that they present insignificant risk of changes in value because of changes in interest rates. In addition, the standard also states that only highly liquid investments acquired three months before maturity can qualify as cash equivalents. Examples are: Three-month BSP Treasury Bill Three month time deposit Three-month money market instruments BSP Instruments purchased three months prior to maturity Redeemable preference shares purchased three months prior to maturity Valuation of Cash Face value Current exchange rate if foreign currency Net realizable value if cash is in bank that is under bankruptcy proceeding Investment of Excess Cash If invested with terms of 3 months or less, treated as “cash and cash equivalents” If invested with terms more than 3 months but not more than 1 year, treated as short term investments classified as other current assets If invested with terms of more than 1 year, treated as long term investment under non-current assets, however, reclassified as current asset if maturity is within 1 year. Cash Fund The classification of a certain cash fund follows the nature of the liability it is created for. Cash funds created for current obligations are treated as current assets. Examples of such are: o Petty cash fund o Payroll fund o Travel fund o Interest fund o Dividend fund o Tax fund Bank Overdraft If problem is silent, treated as current liability If two or more banks accounts exist in one bank and at least one has an overdraft, the overdraft may be offset with the other bank accounts in order to get “cash net of overdraft” or “bank overdraft, net of other bank accounts”. Page 1 of 4 Compensating balance If problem is silent, ignore the compensating balance and treat it as part of cash. If compensating balance is legally restricted, treat such as “cash held as compensating balance” reported as either current or non-current asset depending on the term of the loan or borrowing. Treatment of Entity Checks Undelivered or unreleased checks are treated as cash Postdated checks are treated as cash Stale checks are reverted back to cash and treated a miscellaneous income if immaterial and treated as reversal of previous entry if material. Window Dressing It pertains to any deliberate misstatement of financial statement elements or presenting false statements. It is often accomplished by: Recording as of the last day of an accounting period collections made subsequent to the close of the period Recording as of the last day of an accounting period payments of accounts made subsequent to the close of the period Lapping It is a practice used to conceal cash shortage. It consists of misappropriating a collection from one customer and concealing this defalcation by applying a subsequent collection made from another customer. It involves a series of postponements of the entries for the collection of receivables. This is possible when an entity has poor internal control and especially when the bookkeeper and cashier is one and the same person. Kiting This device used to conceal cash shortage may be utilized if an entity maintains current accounts in different banks. This is usually employed at the end of the month. This method is simple. The amount of cash shortage is drawn from one bank and subsequently deposited to the other bank. This can be discovered by the simultaneous preparation of bank reconciliation. Accounting for Cash Shortage It is initially recorded by debiting “cash short or over” and crediting cash The cash shortage is closed to “due from cashier” account if the shortage is the responsibility of the cashier The cash shortage is closed to “loss from cash shortage” account if reasonable efforts fail to disclose the cause of the shortage Accounting for Cash Overage It is initially recorded by debiting cash and crediting “cash short of over” The cash overage is closed to “miscellaneous income” account if there is no claim to such The cash overage is closed to “payable to cashier” account if the overage was the money of the cashier The Imprest System This is a system of controlling cash which requires all cash receipts to be deposited intact and all cash disbursements made through checks. This system suggests the use of petty cash fund since it is impractical to always use check in paying expenditures especially for small expenses. Page 2 of 4 Petty Cash Fund This cash fund is managed using two methods namely: Imprest Fund System Fluctuating Fund System The main difference between the two systems is the timing of the recognition of the expenses and the cash account that is credited when the petty cash fund is used or replenished. Bank Reconciliation It is a statement which brings into agreement the cash balance per book (general ledger) and the cash balance per bank (bank statement). It is usually prepared on a monthly basis. There are three methods of doing bank reconciliation, namely: Adjusted balance method Bank to book method Book to bank method In doing bank reconciliation, there are certain items that are considered. Reconciliation items for books balance are as follows: Credit memos Debit memos Errors As a rule, all credit memos will increase the cash balance per books while all debit memos will decrease cash balance per books. Effects of errors to the cash balance per books vary depending on the nature of the error committed. Reconciliation items for cash balance per bank statement are as follows: Deposit in Transit Outstanding Checks Errors As a rule, deposits in transit will increase the cash balance per books while outstanding checks will decrease cash balance per books. Effects of errors to the cash balance per books vary depending on the nature of the error committed. It is to be noted, however, that certain types of outstanding checks will not be a reconciling item such as certified checks. After all reconciling items are correctly reflected, the adjusted balance per book and the adjusted balance per bank should already be in agreement. However, there are instances when this does not happen. For cases like this, there is a logical reason to believe that a cash shortage or a cash overage exists. Treatment of such is the same as the previous discussion in this text. It should be noted that in doing bank reconciliations, adjusting entries for book reconciling items are necessary to reflect the correct cash balance in the book of the entity. Two-Date Bank Reconciliation It is basically a bank reconciliation that involves two dates, the first date represents the beginning cash balance and the second date represents the ending cash balance. In order to prepare this kind of reconciliation, a proof of cash is needed. Proof of Cash A proof of cash is a bank reconciliation tool that provides proof for receipts and disbursements. In using this tool, it must be emphasized that at the end of the reconciliation process, the balances of beginning and ending cash as well as the balances of receipts and disbursements in the books and in the bank should be the same. Page 3 of 4 There are three methods of doing this bank reconciliation, namely: Adjusted balance method Bank to book method Book to bank method However, the adjusted balance method is the method that is commonly used. Page 4 of 4